es

es de

de it

itContents

Click to go to key areas of report

- Executive Summary

- Introduction

- Ownership and Management

- Developers and Investors

- Skill shortages - the threat remains

- Power

- Consumption unlikely to decline?

- Average Rack Power/cooling levels rising

- Cost of power to push efficiencies

- Move to renewables

- Use of waste energy

- Retro-fit solutions

- Ongoing supply chain disruption

Waste Heat: The Data Centres’ Warm Embrace

To view a PDF of the report click here

Executive Summary

Welcome to our Summer Report 2023 which, once again, has record levels of optimism for the data centre sector going forward. Indeed, some 89% of our respondents believed in falling supply and rising demand levels would continue for the foreseeable future and 98% of our developers state they are planning to expand over next year

However, what of the challenges we face?

There is longstanding consistency in the belief that there is a shortage of professionals and skilled construction personnel from our respondents with marginal declines reported in this survey and 98% now believe there will be a further decline in skilled staff which will impact on delivery and raise costs. According to our respondents this will also have a huge impact on location of datacentres moving forward with access to skilled staff a key driver.

However, perhaps the most pressing concern is the enduring challenge of sourcing affordable and renewable power. Approximately 81% of our respondents reported their expectation of rising consumption levels over the next three years and 88% expect a rise in the cost of power to increase the demand for power efficient data centre space over the next three years – up from the 82% noted six months ago.

This is as the drive for Net Zero continues and there is no doubt that the data centre industry has invested significant resources and expenditure in its quest to transition away from non-sustainable energy sources. One topic that is increasingly being discussed is the utilisation of waste heat energy generated by data centres. Interestingly, our latest survey shows that the concerns around economic viability of the use of waste heat are diminishing with a 15% decrease of respondents claiming this was an issue. This is a positive start.

Planning and permitting processes are increasingly requiring that more is done to utilise waste heat from data centres to support sustainable development and foster community resilience. Typically, excess heat is expelled into the atmosphere, contributing to urban heat islands and overall energy inefficiency. By capturing and repurposing this waste heat, data centre operators can significantly reduce their environmental impact while providing tangible benefits to nearby communities.

One practical application of waste heat from data centres is to integrate it into district heating systems, which are common in northern Europe. In colder regions, where heating demands are high, data centres can become valuable heat sources, offsetting the need for fossil fuel-based heating systems. The waste heat can be channelled through insulated pipes to neighbouring buildings, providing a sustainable and cost-effective heating solution. This approach not only reduces energy consumption and greenhouse gas emissions but also contributes to the resilience of local communities during extreme weather events. However, if the district heating scheme does not exist, what other options are there?

Another innovative use of waste heat is in greenhouse cultivation and urban farming. Greenhouses require consistent temperatures for optimal plant growth, especially in colder climates. By utilising waste heat from data centres, these facilities can maintain the necessary warmth, creating opportunities for year-round production of fruits, vegetables, and herbs.

Urban farming initiatives can benefit greatly from the surplus heat generated by data centres. Vertical farms, indoor gardens, and aquaponics systems can thrive with the consistent supply of waste heat. These initiatives contribute to local food production, promote food security, and reduce the carbon footprint associated with long-distance transportation of produce.

Waste heat from data centres can also be utilised in various industrial applications. For instance, in manufacturing processes that require heat, such as drying or sterilization, the waste heat can serve as an alternative heat source. We have even seen mini data centres used as ‘digital boilers’ to heat swimming pools with the local authorities benefitting from the water being heated to 30oC for 60% of the time and a refund for the electricity used by the data centre. This helps reduce reliance on fossil fuel-based heating systems, leading to lower energy costs and decreased environmental impact.

Fundamentally, to effectively harness waste heat from data centres, collaboration between data centre operators, local governments, and community stakeholders is crucial. Engaging with local communities, conducting feasibility studies, and implementing appropriate infrastructure are necessary steps to ensure the successful integration of waste heat into community initiatives.

The waste heat generated by data centres represents a valuable resource that, if properly harnessed, can benefit local communities in numerous ways. By incorporating waste heat into district heating systems, supporting greenhouse cultivation and urban farming, and facilitating industrial applications, data centres can contribute to sustainable development, reduce carbon emissions, and enhance community resilience. Embracing these innovative approaches not only helps address environmental challenges but also strengthens the symbiotic relationship between data centres and the communities they operate in. We at BCS have successfully integrated a range of waste heat schemes into many of our projects and have built up leading expertise in this area, an expertise that we are keen that our clients and potential clients benefit from.

Introduction

Welcome to the 26th data centre survey conducted by iX Consulting, an independent research firm specializing in data centre economic analysis, and sponsored by BCS, a leading provider of integrated IT asset consultancy solutions.

The survey work took place in the late spring, a time of the year typically associated with renewal and optimism. Despite some ongoing concerns over geopolitical issues – particularly the Ukrainian conflict - recent economic data shows some promising signs of growth in the European region. According to recent data, the Eurozone's GDP growth rate for the past year reached 3.2%, outperforming initial expectations. This positive trend indicates a potential promising economic outlook for the region.

However, it is important to acknowledge that global inflationary pressures persist, causing some apprehension among policymakers. In response to rising costs, central banks in the US and UK have implemented interest rate hikes this year. Similarly, in the Eurozone, inflation levels have remained stubbornly high, prompting speculation that the European Central Bank may need to take decisive actions to address the issue.

Against this economic backdrop, our latest survey aims to assess the current state and prospects of the European data centre industry. While the industry may face challenges associated with broader global factors, such as supply chain disruptions, the strong growth rates witnessed across the Eurozone indicate a sustained demand for technology-driven services. This survey seeks to explore the industry's response to these conditions and identify any emerging trends or opportunities that arise as a result.

Fig 1

What is your primary relationship with the data centre industry?

We continue to survey a diverse group of individuals and organizations involved in real estate, investment, colocation, IT, and telecom industries throughout Europe. Our respondents include real estate developers, investors, corporate occupiers, colocation providers, and IT and telecom service providers. Together, these stakeholders manage data centre portfolios comprising approximately 5.6 million square meters of technical floorspace based across 39 countries.

Fig 2

Total Technical Floorspace

Fig 3

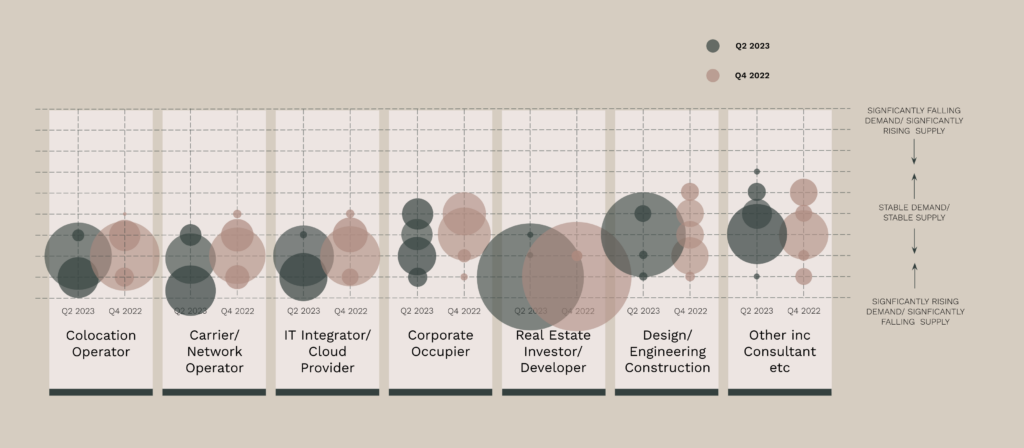

The Supply/Demand dynamic

Fig 4

- Whilst economic challenges continue to confront Europe as a whole, the underlying robustness of the European data centre market is illustrated by the continued belief in falling supply and rising demand levels; a view held by some 89% – a rise on the 85% recorded in winter 2022.

- Indeed, there is almost universal agreement amongst respondents that demand will either increase or remain the same over the coming year; the third survey in a row this has been the case.

- Our developer and investor stakeholders retain their position as the most confident group in terms of market sentiment. For the sixth successive survey all this group expect a continuation of rising demand over the next 12 months.

- Most suppliers of data centre services remain positive around the balance between supply and demand in the market, with all our colocation providers seeing rising demand; unchanged on that recorded six months ago.

- In addition, carriers/network operators and IT integrators are even more confident than reported in winter 2022, with close to universal agreement that the coming year will continue to be characterised by falling supply and rising demand; a rise on just over 90% recorded previously.

- Furthermore, there has been a marked uplift in the proportion of corporate respondents that expect demand to rise over the coming year – up from around 60% six months ago to 74% this time around.

Ownership and Management

For suppliers of data centre services – colocation operators and IT integrators/web hosting providers – the desire to manage their own facilities remains uppermost with over three-quarters disclosing that 80% or more of their data centre portfolio is internally managed. This degree of control gives them the flexibility to be more agile whilst responding to changing client demands, without the potential limitations in a commercial and physical sense that third-party management may present.

In contrast, our corporate stakeholder respondents continue to trust outsourcing a larger proportion of their data centre management to third parties, with some four-fifths indicating that they manage at least 80% or more of their portfolio externally, a similar proportion to that recorded six months ago, and a notable increase over the last decade from around half.

Over the course of our survey work, there has been a significant shift in the perception of end-users towards third-party solutions. For instance, let's consider a question we asked respondents in 2010 about their belief in the future adoption of cloud computing being limited due to ongoing security concerns. At that time, 57% of respondents expressed their agreement with this statement. However, as shown in our latest survey, the widespread adoption of third-party solutions indicates that these fears have been effectively overcome. Advancements in technology, enhanced security protocols, and the added benefits of service flexibility and cost savings on expensive data centre constructions have made these solutions highly appealing to many users.

However, it is important to note that there is evidence supporting the appeal of a blended approach by certain individuals. This approach combines the advantages of both external and in-house solutions, enabling enterprises to retain a higher level of control over specific aspects of their infrastructure that they prefer to keep internally managed. At the same time, they can still benefit from outsourcing other parts of their data centre environments.

Utilisation

Both service providers and users share a crucial objective: to optimize the utilization of their data centres while retaining the ability to accommodate growth. This need, which we have consistently highlighted since the start of our survey over a decade ago, has become even more critical in the current global economy characterized by relatively high inflation. As these pressures impact profit margins, there is an increased drive to enhance efficiencies across all areas of enterprise operations.

The ongoing analysis reveals a continual trend in favour of third-party utilisation ratios surpassing those of internally managed solutions. According to our winter 2022 survey, 82% of respondents disclosed that they leveraged over 80% of their outsourced technical footprint, while only 36% achieved the same level of utilisation for in-house managed facilities. In the most recent survey, this trend has continued, with approximately 83% of participants maintaining utilisation rates of externally managed solutions at 80% or above, while in-house utilisation rates have increased to 40%.

Indeed, among corporate occupiers, the drive to optimise efficiencies in third-party data centres has resulted in an even higher proportion (84%) reporting high utilisation, whilst 31% reported this for in-house managed facilities.

Fig 5

How much of your current data centre space is active and being used?

Average utilisation rates of their own facilities for the colocation operators, carriers, integrators and cloud providers tend to be slightly lower at around 65%. This most likely continues to reflect the need to have space close to completeness to allow for fast deployment to meet demand needs. In contrast, service providers are driven by a need to maximise value for money regarding their third-party space, maintaining relatively high utilisation rates at about 85% in these facilities.

Expansion

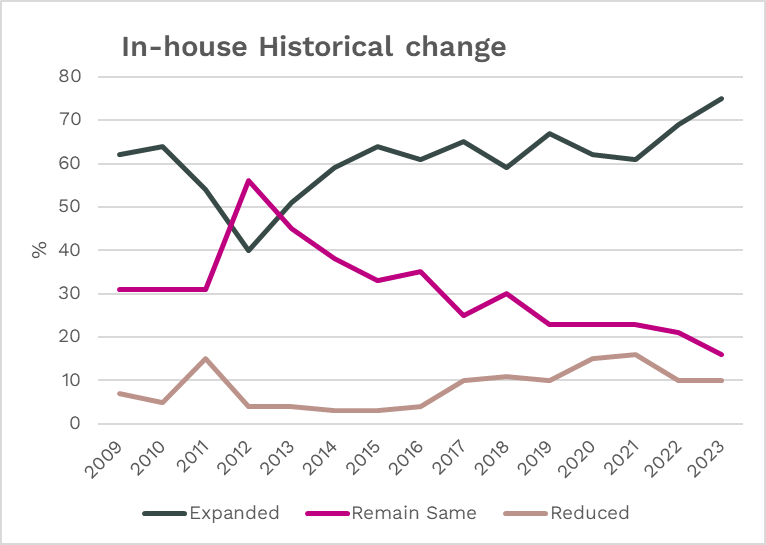

In the six months to the end of April 2023, around three-quarters of respondents indicated that they had increased their in-house managed data centre capacity, a rise from the 69% reporting this in our last survey. In addition, around 16% reported no change whilst some 10% indicated a reduction in their in-house floorspace, the latter a proportion unchanged from the preceding survey.

In the face of economic turbulence and persistent geopolitical uncertainties, the increase in capacity among a substantial proportion of survey participants continues to be encouraging for the European data centre industry. It is evident that our respondents remain confident around the enduring demand and growth in the IT services industry in the foreseeable future.

Fig 6

How has your total fitted technical floorspace altered over the past six months?

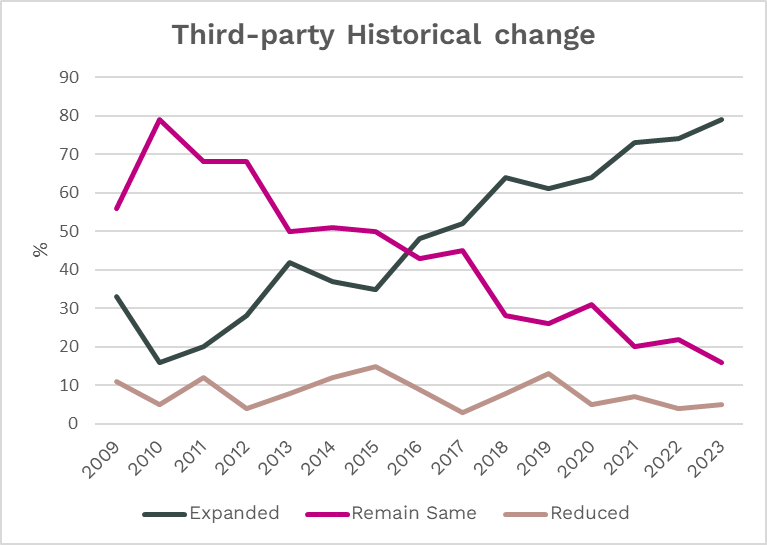

Indeed, this conviction on future IT services growth is further evidenced when we look at third-party expansion patterns over the past six months, with some 79% of survey participants indicating an increase in technical floorspace over the period compared to 74% recorded in winter 2022. It is worth noting that this sits considerably higher than the long-term average of some 53%. As with internally managed space, around one-in-six reported no change in their third-party portfolio whilst only 4% reported a floorspace reduction.

Fig 7

Amongst our services providers, we can see a level of expansion which provides evidence that these providers are continuing to respond to healthy levels of demand from their end-user clients. Nearly all our telecom and carrier respondents reported an expansion of their own stock over the last six months, whilst two-thirds of colocation suppliers indicated the same.

Interestingly - and perhaps slightly against the trend - the number of end-users who indicated an increase in their in-house technical floorspace over the past six months has risen, from 6% recorded previously to 12% this time. At the same time, we see a rise in the number of end-users who have disclosed that they had reduced their on-premises stock; from 53% to around 59%.

Fig 8

Fig 9

Corporate Sector – data centre proportion expansion

With regards to third-party change, end user participants dominate the story. Some 84% of whom reported an increase in their externally manged data centres over the past six months, albeit a marginal reduction on the 88% reported in our preceding survey. Despite a slight contraction, these levels continue to provide strong evidence that outsourced models regarding data centre requirements remain in vogue with end users.

Amongst our service providers some 76% reported a climb in the number of third-party managed data centre expansions over the period – a marginal dip from 79% reported in our last survey.

How was expansion achieved?

In terms of expansion within self-managed facilities over the past six months, the most favoured chosen route remains via a self-build option, 49% of respondents outlined this approach, a slight decrease from the 53% in our last survey. The option of purchasing or leasing through a development partner was pursued by just over a third of respondents, similar levels to that recorded six months ago.

In addition, around 14% reported that they have reduced their technical floorspace by decommissioning one or more legacy facilities, similar levels to those recorded in the preceding survey with the vast majority of these being end-user participants.

Utilising a colocation provider remains the most popular option for our survey stakeholders in terms of externally managed expansion; some two-thirds saying that they had chosen this route, followed by IT integrators, carriers and network providers.

Fig 10A

If change has occurred via expansion or contraction how have you achieved this? In house

Once again it is important to bear in mind that several respondents suggested that they chose a multi-supplier route to meet their externally manged requirements. These generally reflect those with a multi facility expansion programme which individually require their own distinct solution, a best-fit approach which sees different solutions purchased to suit needs of geography, cost, availability etc.

Fig 10B

If change has occurred via expansion or contraction how have you achieved this? Third party

No slowdown in expansion plans

The latest results suggest that 63% of respondents see their self-managed technical floorspace expanding over the coming year, up from the 60% reporting the same six months ago, with our service provider respondents being the most assured at 85%, an increase on the 82% recorded last winter. The proportion of participants indicating they would reduce their in-house data centre space remains small, standing at just 8% and unchanged for the third successive survey.

Fig 11

What are your current expectations for changes to your ‘in-house’ technical data centre area?

The proportion of those participants who believe that there will be “no change” in the amount of their in-house data centre space over the next year has risen slightly from 24% to 26% whilst those respondents who are undecided has now halved from 8% to 4%. Amongst end-users the appetite for continued expansion of in-house data centres continues at relatively low levels. Only 13% are intending to expand on-premises facilities over the next 12 months, contrasted to the 79% indicating they would expand operations with an external infrastructure partner over the coming period.

In addition, nearly two-fifths of end-users said they expected to downsize their in-house facilities during the period whilst almost half stated that would choose to retain the same level.

Prospects for externally controlled data centre facilities also appear positive over the next year. Some 61% of respondents reporting their intention to expand over that period, a proportion unchanged since the preceding survey. Indeed, across the whole metric, survey participants share a similar profile to that recorded six months ago. Those who reported there will be no change of third-party estate has remained static at 31%, whilst the number of respondents who are undecided on this issue is also unmoved at 4%. In addition, few expect to downsize their externally managed facilities over the period – just 3% of all respondents – a fall on the 4% recorded last winter.

Fig 12

What are your current expectations for changes to your ‘third party’ technical data centre area?

Despite the overall consistency of responses regarding third-party expansions over the past six months, there are variations when different sectors are assessed. For instance, among service providers, there has been a slight increase from 52% to 54% in the proportion expecting to expand their externally owned facilities. Conversely, among end-users, the intention to expand in third-party data centres has seen a modest decrease from 83% to 79% over the same period.

Drivers of change

Corporate expansion or contraction has been long established as the most highly ranked factor driving change in both internally controlled and third-party data centres. This has certainly been the case since we undertook the first of these surveys in 2009. Our latest survey confirms the continuation of this trend, with around a third citing it as the top priority for both internal and external solutions; a proportion largely un-changed over the past three surveys.

Interestingly although demand for power and the costs associated with it remains ranked second by our respondents as an important driver of change for both internally and externally operated space, our latest survey has recorded a marginal decline to 18% from the 24% reported last winter. It may be that the highly publicised inflationary pressures on energy costs that we have seen over the past year, have now been “priced in” to respondents thinking and as such its impact is already acknowledged. That is not to say that the impact of power is under-played by our stakeholders, given that once again as we report later in this survey that the availability of power is by some distance ranked the single most important driver regarding data centre choice.

Fig 13

What factors are/will be driving these changes?

There has been a small decline in those who cited budgetary issues as higher on the scale of importance, down from around 17% six months ago to around 15% this time around. This marginal fall in importance is noted across both in-house facilities and third-party managed floorspace. The ranking of availability of appropriate data centre product by around 14% of respondents represents a marginal uplift on the 11% reported previously, and unsurprisingly the proportion of those citing this regarding third-party space is higher at some 16%.

It is also worth noting that we have seen a marginal rise in those citing changes in fiscal structures; up from 8% to around 10% overall and 12% in respect of drivers for in-house solutions. Whilst data sovereignty continues to be ranked near the bottom of the list, identified by around 9% of participants, although a slight rise on the 8% recorded in our winter survey.

Developers and Investors

Supply plans continue apace

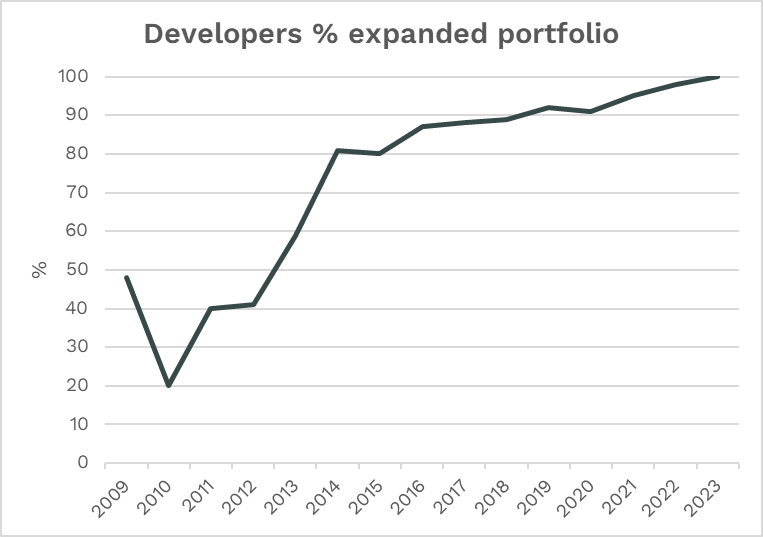

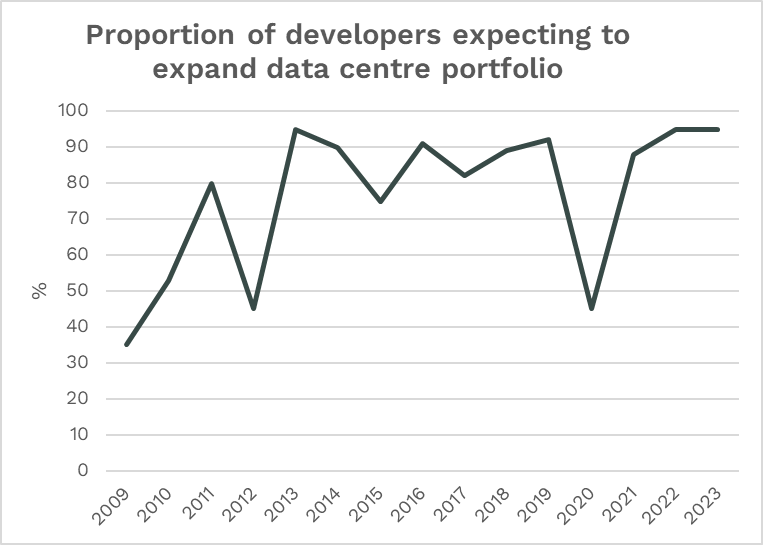

The enduring strength of the European data centre market highlights the industry's ability to thrive despite multiple obstacles, including macroeconomic challenges and geopolitical difficulties. This robustness is illustrated by the continuing confidence shown by those charged with delivering new technical real estate stock to the market. All our developer and investor stakeholders have stated in our latest survey that they expanded their data centre stock during the past 12-month period.

This marks the third consecutive survey in which we have observed such widespread and near-universal levels of expansion amongst this group of players. It is important to note that this progress occurs against a backdrop of some of the most challenging economic circumstances that we have experienced for quite a while, and only a few years after the global problems caused by the Coronavirus.

Fig 14

Looking forward, there is ongoing evidence that the delivery of new stock is likely to continue with little sign of a slowing in its pace. For the third successive survey some 95% of developers and investors revealed that they are anticipating expanding their portfolio over the coming year, levels last experienced a decade ago, and some of the highest levels we have recorded ever in the survey.

Fig 15

One way of assessing the market's prospects in the short to medium term involves evaluating the risk appetite of developers and investors. For the past 14 years, one benchmark we have consistently monitored is the proportion of secured letting area necessary before construction can commence on a project. By tracking the minimum level of pre-secured occupancy required, we are able to see the industry's willingness to invest and undertake new developments.

Fig 16

If it is your intention to develop more technical space during the next 12-18 months, on what basis will that be?

Once again analysis of responses suggests that there is a rising degree of positive sentiment amongst developer participants over the past six months with, on average, a lower degree of pre-letting required. The number of respondents requiring at least 75% or more of their scheme to be pre-committed has fallen from 27% to some 18% this time around, the second successive survey we have noted a fall.

In addition, further evidence of this increased positivity is illustrated by the proportion of those who are prepared to green-light the build-out having secured a pre-lease on 25% or less. This quantity has risen from zero a year ago to around 14% six months later and now stands at some 22%.

Fig 17

For Wholesale transactions, what is the minimum lease length that you would accept?

Another measure of sentiment amongst these participants is the minimum lease length requirement for a wholesale transaction that a developer would like to achieve. As with pre-leasing commitments, analysis of responses provides more evidence of increased positivity amongst developers and investors with, on average, a lowering in the length of time that they are happy to secure on this type of transaction.

Our latest survey indicates that 13% would require a term of five years or more, a marginal fall on the 14% noted six months ago. In addition, around two-thirds suggested a three-to-five-year period would be needed, an increase on the 59% who suggested the same six months ago. The residual 22% would accept a period of below three years.

Ranking of choice factors for new data centre

Since we began this survey in 2009, the availability of power has been identified as the single most important factor driving data centre choice amongst our respondents. Our latest survey once again reiterates this as the case with nearly three-quarters citing it as their number one driving choice, unchanged on that proportion recorded last winter. In addition, amongst our developer and investor respondents, the proportion that ranked this first stood significantly higher than the average, at some 91%.

Location retains its position as the second most popular factor, with two-fifths of all respondents ranking it at least in their top two choices, the same proportion registered in our winter survey and in line with the long-term tracking average. Six months ago, we noted that moving forward the importance of location is unlikely to diminish given current global political and economic uncertainty; the latest findings endorse this conclusion.

Further evidence of the increased importance to our respondents of location is provided by the uplift in those who place political or social stability as one of their top two ranked factors; 40% this time around compared to 30% recorded six months ago.

This survey has also seen a continuation of the trend that access to fibre is now viewed as an increasingly important factor, whilst not in the first position for many (8% down on the 14% six months ago) a further two-fifths cited it as the second most important factor which is a significant uplift on 25% seen last year.

One factor which appears to have become more popular is the availability of specialist data centre construction skills which is cited by around 20% of our respondents as one of the top two ranked factors, up on the 16% seen six months previously, and underpinning the ongoing uncertainty around a skills gap growing in the industry. Amongst our developer, investor, and DEC (Design, Engineering, and Construction) respondents, this is rated more highly – some 59% ranking it in their top two factors. Meanwhile, Land Price and Total Build out costs similarly score more highly amongst these latter groups.

Fig 18

Drivers Ranking – data centre choice

Skill shortages - the threat remains

Any industry faced with a shortage of qualified professionals to service the labour requirements of its component enterprises and those that service it, will face difficulties. The shortage of qualified professionals in the data centre industry can reduce its ability to meet the growing demands of enterprise, and could lead to increased operational costs, decreased efficiency and potential security vulnerabilities.

There are several reasons contributing to the shortage of skilled staff in the data centre industry. The exponential growth of data and the increasing reliance on digital infrastructure have outpaced the availability of trained professionals, particularly those that can evolve to adopt new technologies and operations. At the same time, a lack of specialised training programs means there may be a gap in the multidisciplinary skills education required for data centre operations. In addition, skilled professionals in the data centre industry are in high demand, and often have multiple opportunities available to them, making it a challenge for data centre companies to attract and retain top talent.

It should be noted that these threats are relatively longstanding, rising from the dislocation of the pace of growth of the industry allied to time lags associated with attracting and training skilled labour resource. In recent years, the impact of the Covid pandemic has exacerbated these problems via the imposition of lockdown restrictions on freedom of movement and environments for learning.

Fig 19 A and B

- Real – and ongoing - concerns over a skills shortage in the data centre industry exist amongst our respondents with 98% believing that the coming year will see a decline in supply of staff, a slight rise on the 96% reporting this in winter 2022, and above the 93% who reported the same in winter 2020.

- Further adding to the problem, some 92% believe that this will be accompanied by a rise in demand for staff with these skillsets.

- There is universal agreement amongst our developer respondents that the coming year will be characterised by significantly falling supply of staff whilst the demand for those skill sets rises – the fourth successive survey this has been the case and represents the joint highest degree of assent amongst all our respondent’s groupings.

- Design, Engineering and Construction (DEC) respondents share a similar response profile, with universal belief that the next year will be characterised by a fall in supply of staff whilst the demand for those skill sets increases.

- Whilst these two groups of respondents could be said to be the at the apex of these shortages, an increasing level of concern is being expressed by the majority of our survey participants. Many suppliers of data centre services appear increasingly worried about this balance between supply and demand of labour; the majority of colocation providers carriers/network operators and IT integrators believing the coming year will be characterised by falling supply and rising demand, 46% of whom expressed their concern in the strongest possible terms contrasted to just over one-third of six months ago.

- Whilst amongst end-users, the level of concern has remained constant: some 84% believe that a rising supply of skilled staff would be met with falling demand, more believe that this is most significant in terms of both supply and demand has risen to some 16% from zero last time around.

Who’s in short supply?

Fig 20 A

It is increasingly difficult to source sufficiently skilled design professionals to deliver our current projects

Concerns amongst our respondents about shortages of suitably qualified design professionals remain. In our latest survey some four-fifths of all replies stated this view, a quantity largely unchanged over the past six months.

Construction of new data centres is severely impacted by shortages of build professionals. Some 81% of surveyed stakeholders in the European data centre industry expressed their concerns that a shortage of sufficiently skilled build contractors existed – a marginal decline on the 83% reported last winter but continuing to be a problem.

Fig 20 B

It is increasingly difficult to source sufficiently skilled build professionals to deliver our current projects

In addition, there are rising worries amongst our respondents that the sourcing of operational staff for their data centres is becoming more difficult. These problems are marginally less acute than at the design and build stages but appear to be becoming more of a concern. Some 76% expressed their agreement, an increase on the 68% recorded in Q4 2022.

Fig 20 C

It is increasingly difficult to source skilled operations professionals to deliver our current projects

Our latest survey indicates a consensus among the DEC respondents regarding shortages in both the design and build stages. This agreement has persisted for three consecutive surveys, suggesting that the issue is a recurring concern for this group. Furthermore, our developers also universally agreed that they are encountering challenges in finding skilled professionals for design and build consistent with our findings from the previous winter survey.

Amongst our service providers the strength of belief in design and build skill shortages remains less pronounced, nevertheless, 82% (81% in Q4 2022) agreed that shortages are problematic. For end users, shortages of skilled operational staff pose the biggest problem – 94% compared to 88% six months ago. In contrast amongst these corporate occupiers, just 41% and 40% share the same degree of concern for design professionals for build professionals respectively.

There is a high degree of acknowledgment amongst our responders that these shortages are common across the sector impacting a raft of different roles, with all participants identifying a minimum of two specific roles of concern, and over 90% of the respondents citing at least three different roles that they considered to be of concern.

Within the build sector, approximately 59% of the survey participants reported experiencing shortages of quantity surveyors, site managers, and site engineers in the past year. This proportion aligns with the findings reported in our previous winter survey.

On the operational side, approximately 68% of the respondents have directly experienced shortages among operations and network engineers/technicians over the past year. This figure has increased from the 55% reported six months ago, indicating a growing concern regarding the availability of skilled professionals in these roles. Similarly, around 62% of the participants specified a shortage of infrastructure specialists over the same period. Although this percentage has increased marginally from the previous survey's result of 60%, it still reflects a significant proportion of respondents expressing concerns about the availability of skilled infrastructure specialists.

Once again around two-thirds of our respondents identified a shortage of Mechanical & Electrical project managers as an area of concern around the availability of skilled workforce – marginally up on the 60% reporting the same last winter.

Impact of skill shortages

Lying at the heart of the debate around shortages of skilled professionals is the potential impact on the delivery of new stock and subsequent consequences for the end user. The survey findings unequivocally support the notion that these shortages have already resulted in tangible consequences and have directly affected our respondents. When asked about the impacts they had experienced in the past year due to these shortages, the majority of respondents cited multiple factors.

For the last four surveys the most reported impact has been that these skills shortages have led to a greater workload on existing staff. In this survey we have seen a slight decline in the proportion of respondents, with some 85% citing it, down from almost 90% six months ago and pushing it back to second place. Just taking its place at the top, though by a very slim margin, is increased operating and labour costs, which is now reported by 86% of participants, roughly the same proportion as reported last winter.

These shortages have also contributed to the growing popularity of outsourcing options, with approximately 45% of respondents acknowledging it as a factor. However, it's worth noting that this percentage has decreased from the 52% recorded in our previous survey, and the more extreme consequence of skills shortages - lost orders – remains at just 9%, in line with the proportion identified six months ago.

The number of respondents who found it problematic to resource existing work this year has remained un-changed, with 43% stating that they had experienced difficulties in meeting deadlines or client objectives. It should be noted that this remains well below the 70% who cited it as factor in Summer 2020, when the effects of the COVID pandemic and subsequent lockdowns were being felt across the world.

Fig 21

In the past year we have experienced the following as a direct result of skill shortages

In addition, just less than a third stated that shortages had led to delays to developing new products/innovations, down on the 48% recording this in our last survey, whilst the proportion that noted they had ceased offering certain products or services has risen slightly to 22% from 17%.

Power

Consumption unlikely to decline?

The data centre industry and its participants continue to face the enduring challenge of sourcing affordable and renewable power. Therefore, having a comprehensive understanding of power usage is crucial in improving the alignment between demand and supply within the industry.

Once again, there is substantial evidence indicating that power consumption in the data centre industry is projected to increase, at least in the near future. Approximately 81% of our respondents reported their expectation of rising consumption levels over the next three years. Although this represents a slight decrease from the 84% recorded six months ago, it is important to note that the number of participants anticipating a more significant increase in consumption has risen from 40% to 49% in the current survey.

These findings underscore the ongoing upward trend in power consumption within the data centre industry. They also highlight the growing awareness among respondents of the potential magnitude of this increase, as the industry grapples with the challenge of sourcing affordable and sustainable power, understanding and effectively managing power consumption will remain crucial in the coming years.

Fig 22

Over the next three years, we expect our power per sq meter consumption to:

Once again amongst our service providers this proportion is even higher at some 96%, approximately the same as reported just six months ago, whilst 68% of end-users expect power consumption levels to rise over the period; an increase on the 62% recorded in our last survey.

Average Rack Power/cooling levels rising

An analysis of the expectations of our latest respondents regarding their average rack power/cooling levels in the upcoming year reveals only minimal differences compared to the data recorded in Q4 2022.

Approximately 28% of survey participants anticipate an average rack power/cooling level of 9kw-12kw in the coming year, representing a slight increase from the figure reported in our previous survey. Additionally, nearly a quarter of respondents expect the average rack power/cooling level to reach 12kw-15kw within the next 12 months, marking a notable increase compared to the 17% recorded in the same survey. The proportion of respondents indicating a level higher than 15kw per rack remains small at 7%, consistent with the metric reported last winter.

Amongst our corporate respondents, there were some changes since our last survey. Most recently, some 47% are expecting to see average rack power/cooling level of 6kw-9kw, up from 40% last winter, whilst just 21% are expecting to see average rack power/cooling level of 3kw-6kw, a drop on the 33% citing the same in Q4 2022.

Fig 23

What is your expectations for your average rack power /cooling level iby the end of the year

Cost of power to push efficiencies

Fig 24

We expect a rise in the cost of power in Europe to increase the demand for power efficient data centre space over the next three years

Over the past year, global inflation rates have surpassed even the levels witnessed during the peak of the banking crisis in 2007-08. In the case of the UK, inflation has reached its highest point in 40 years. One significant factor contributing to this situation is the swift escalation in energy costs, particularly influenced by the Russian invasion of Ukraine. Against this background - and given that the desire for efficiency is one of the core tenets for most organisations - it is perhaps not surprising that enterprises will look for solutions to limit their exposure to rising energy costs.

Some 88% of our respondents expect a rise in the cost of power to increase the demand for power efficient data centre space over the next three years – up from the 82% noted six months ago. For the third survey in a row some 95% of service providers expressed their agreement with this outcome, and notably some 58% of end-users cited the same, down from the 67% recorded earlier in the year.

Move to renewables

The data centre industry continues to prioritize enhancing energy efficiency and embracing renewable energy sources. Apart from the financial benefits that power efficiencies bring to operators, there is a global political and social push for stronger environmental protection. The move to renewable energy in the data centre industry represents a pivotal step towards creating a more sustainable and environmentally conscious digital infrastructure and once again our latest survey clearly shows that the industry remains deeply engaged in providing appropriate power solutions.

As we reported in our winter 2022 survey some 82% agreed that they expect the sourcing of power for data centres to be at least 90% from renewable sources over a 10-year horizon and six months later this proportion remains the same. In addition, only a very small minority - just 3% - believe that this will not be the case.

Fig 25

We expect that the sourcing of power for our data centre in 2033 will be 90% or more sourced from renewable sources

Amongst our service providers the proportion in agreement jumps to some 90%; marginally up on the 88% reported six months ago. For the third survey in a row our developer and investor respondents were near universal in their agreement on this issue.

The ongoing geopolitical situation, particularly the continued occupation of Ukraine by Russia, is likely to continue to incentivise a shift towards renewable energy sources which are more likely to have been generated locally and thus making it less susceptible to global factors and potentially improving energy security and pricing. The latest survey offers additional evidence supporting this notion, with approximately 68% of survey participants agreed that recent events would prompt them to expedite their transition towards renewable energy; a slight decrease from the 70% reported last winter, although remaining a significant proportion.

Amongst end-users this proportion was even higher at some 85%, marginally up on 83% reporting the same six months ago. In addition, amongst service providers some 70% shared this belief, a similar proportion to that seen last winter. For developers and investors, the level of agreement is slightly lower at around two-thirds, a notable decline on the 80% who expressed this preference in Q2 2022. This metric will be one to watch as developers and investors have a significant influence on the move to renewable energy sources and are key to Europe’s move towards its promises of Net Zero.

Fig 26

In the light of recent geopolitical events, we will pursue an accelerated move towards renewable energy sources for our data centre(s).

Use of waste energy

There is no doubt that the data centre industry has invested significant resources and expenditure in its quest to transition away from non-sustainable energy sources. It consistently strives to enhance its efficiency by exploring new methods and improving existing ones. One topic that is increasingly being discussed is the utilisation of waste heat energy generated by data centres.

However, it seems that a significant number of our survey respondents remain sceptical about the current economic viability of such programs, despite some indications that these concerns may be diminishing. While 63% of participants expressed concerns about the efficiency of power generated using waste energy, this does indicate a decrease compared to the 73% who held the same view in winter 2022.

Among our developers and investors, four out of five individuals expressed the highest level of concern regarding the cost viability of utilisation of waste heat energy. Interestingly, among our end-user respondents, there seems to be less concern, with just over two-fifths expressing reservations, and none of them doing so in the strongest terms possible.

Fig 27

Over the next 5 years, the economic viability of waste energy programmes needs to improve greatly in order for us to consider

Retro-fit solutions

Fig 28

We would actively look to retrofit energy production solutions (i.e. solar, turbines, waste-to-energy) at our data centres to accelerate the move towards our Net Zero requirements.

For the third survey in a row, around two-thirds of our respondents agree that retrofitting exiting facilities is something that they would consider. Amongst our differing respondent groups, the highest degree of agreement came from our DEC respondents, 93%, up from 85% recorded in our winter 2022 survey. In addition, our service providers/carriers (81%) and colocation operators (78%) remain largely supportive of this option, although both groups have seen a slight fall in positive proportions compared to our last survey.

Ongoing supply chain disruption

Disruption is arguably the technology sector’s key tool, as it utilises such disruption to cause significant change in an industry by means of innovation. However, even the technology sector has been unable to shield itself from the ravages of the worst disruptor of recent years; the Covid pandemic. It should of course be noted that the industry was also able to take advantage of this disruption by enabling and servicing the rise in home working, resulting in the soaring demand for on-line communications and collaborative software such as Teams and Zoom housed in data centres.

The downside impacts that have been felt however, are largely related to raw material cost inflation, and disruption amongst global supply chains. Indeed, there is little doubt that these supply chains are continuing to suffer ongoing impacts in the post pandemic world, exacerbated by geopolitical factors such as the Russian invasion of Ukraine which has led in turn to further economic consequences, not least the rise in energy prices and consequent calculative inflationary effects.

Fig 29

We have experienced considerable supply chain volatility over the past year

It is within this context that we have sought the views of our European data centre participants on a variety of supply chain topics. Firstly, there appears to have been little sign of easing on some supply chains, with 86% respondents stating that they had experienced supply chain volatility over the past year, slightly down on the same level who reported the same in winter 2022 but similar to the levels who reported the same one year ago.

Once again, the professionals responsible for delivering new data centre facilities to the market have been significantly impacted by the volatility in the supply chain. Our survey of developer/investor respondents revealed that some 91% of them confirmed being affected, expressing their strong agreement. This figure represents an increase from the 82% reported six months ago and 83% recorded a year ago. Notably, among our DEC stakeholders the impact was more pronounced, with 93% expressing their strong agreement, compared to 70% in Q4 2022. Amongst our service providers, there is still a high level of agreement regarding this disruption albeit with some marginal easing – 92% stated that they had experienced such supply chain problems, down from 97% reported six months ago.

Fig 30

Regarding the base construction of our data centre(s) in Europe, we have experienced the following:

In this survey, there is some welcome evidence that our build stakeholders are seeing alleviation in problems around their ability to source raw materials used for construction, although not across all items. Issues in the sourcing of dry lining materials has remained relatively static, reported by around a third of respondents whilst the sourcing of cladding has evidently become slightly more problematic, rising from 31% to 34% of respondents reporting issues.

However, over the past six months, our respondents have reported an easing of the difficulties in getting hold of other key materials such as steel, where the proportion reporting problems has fallen to 33% from 42%, and for cement and concrete, down to 27% from 38%. Despite this there is evidence of an inflationary impact on our build professionals, with a rise in associated costs most notable amongst transportation costs as well as construction labour costs. In the case of both, some 80% of respondents reported a rise on that cited six months ago. Amongst our developer stakeholders – around 95% have reported experiencing rising costs across all three of these metrics, a rise on the 90% specifying the same six months ago.

Among our participants, the acquisition of cooling units and UPS (Uninterruptible Power Supply) hardware has proven to be the most challenging. Regarding the former, approximately 57% of participants acknowledged experiencing difficulties in securing such equipment over the past year, while 50% stated the same challenges with UPS acquisitions.

Fig 31

Regarding data centre equipment, over the past year we have experienced difficulties sourcing the following

Furthermore, two-fifths of the participants encountered similar issues with sourcing power distribution units/components, and an additional third cited difficulties in obtaining switchgear. Just over a quarter of the respondents found it difficult to source lithium-ion batteries and generators.

Supply chain disruption will impact future data centre locations decisions

In our survey, we have consistently highlighted the importance of location for our stakeholders when evaluating new data centre credentials. Indeed, earlier in this report, our latest data shows that it ranks second only to power availability among the contributing factors for data centre choice.

However, our respondents are increasingly concerned that ongoing disruptions in the supply chain will significantly impact their decision-making process regarding future data centre locations. Nearly two-thirds of our participants reveal that this factor will heavily influence their choices for future data centre locations. This represents an increase from the 54% recorded in our winter 2022 survey.

Our DEC respondents remain one of the most fervent in agreement, with some 85% expressing their agreement albeit a decline from 92% recorded six months ago. In contrast service providers appear more concerned than previously with 65% in agreement, up from the 54% previously recorded. Indeed, our integrator participants are now the most heavily in agreement – some 88% agreed.

Fig 32

Potential long term supply chain problems will impact significantly on our decision making regarding the future location(s) of our data centre(s).

In contrast, for the third survey in a row end-user respondents expressed the lowest level of agreement – just 43%, albeit this represents an uplift on the 39% recorded in the winter survey. End-users also recorded the highest levels of disagreement with 22%, a small decline on the 28% recorded six months ago.

A change of supplier(s)

Fig 33

In the past year we have undertaken the following actions in response to supply chain disruption

The challenges faced in the supply chain have undoubtedly pushed data centre designers and builders to carefully examine existing supply routes, identifying potential weak points and implementing measures to mitigate associated risks. According to our latest survey, in general most companies have embraced the post-pandemic world by prioritizing the agility and resilience of their supply chains.

Amongst respondents, around 60% have now looked to source from local or national suppliers, potentially avoiding inflated global transport costs as well as shortening lead-in times. Around 45% have expanded their list of suppliers to give greater breadth of options, and a similar number have increased order sizes allowing them to carry stock or gain efficiencies from bulk buying. Around one quarter of participants have actively changed their supplier or suppliers over the past year in response to disruption.

Amongst our professional groups, just over half of our DEC respondents increased their size of orders to ensure they have access to materials they require, whilst 47% of end users and 66% of colocation providers looked to increasingly source from local or national suppliers. Whatever the chosen route, the desired conclusion is the creation of a stronger, more diversified supply chain with greater potential for risk mitigation.

Inflationary impact

There has been significant concern regarding the potential threat to economic prospects due to the prevailing high inflationary environment experienced by a substantial portion of the global economy. Earlier we reported on the inflationary impact that our survey respondents have experienced around materials, labour and transportation costs linked to expenditure on new build data centres.

Fig 34

Labour and materials’ inflation has led to a re-evaluation of our new data centre project and its subsequent postponement for….

In our winter 2022 survey, there was little evidence that such rising costs were going to impact the number of data centre projects proposed by our respondents moving forward. Reassuringly, the latest survey data suggests that this remains the case.

Over the short term (the next two years) just 6% stated that such a re-evaluation had taken place, the same proportion reported in winter 2022. Over the medium term (two years plus) this proportion stood at only 5%, although this is an increase from the 2% previously reported and 4% stated that such a review had led to a postponement of a project for the foreseeable future – unchanged over the past six months.

Indeed, four-fifths of respondents detailed no impact on their plans in the short term – again in line with what was stated in winter 2022; two-thirds stated the same over medium term and 68% over the longer term. In both the latter cases, these represent a decline over the past six months from 79% and 74% respectively. As was the case in our preceding survey none of our developer respondents suggested any planned postponements of their projects.

Amongst our service providers, the proportion who reported postponements remained low at 7% (short term) – albeit this represents an uplift on the 3% reported in winter 2022 - 3% (medium term – up from 2%) and 3% (long term) which is down from 4%.

Amongst our end-users, for the second survey in succession there were no reported postponements over the medium term or longer. However, we have noted a rise in the number that reported that they re-evaluated projects over the next 12-24 months and had subsequently delayed them – up to 16% from 6%.

Will the clients pay?

Fig 35

Over the past year, inflation in the operational costs of our data centre have forced us to pass on some or all these increases to our clients

Our recent survey highlights the pressing issue that enterprises face in an inflationary environment, where rising costs directly impact their business operations. The fundamental question arises: are these enterprises prepared to absorb the cost increases or will they opt to pass them, either fully or partially, onto their client base?

A significant majority (66%) have already chosen to pass on the higher costs to their clients within the past 12 months. This figure represents an increase from the previous survey conducted during winter, where only 52% of respondents reported the same action. Amongst our service providers (colocation operators, carriers, and integrators) this rises to 78% - a marked increase on the 59% recording the agreement six months ago. Similarly, among developers, the proportion has risen from 40% to 64%.

Moving forward there may be a degree of optimism regarding an easing of inflationary pressures, albeit relatively small at present. Some 79% of our respondents still expect to have to raise prices to cover increasing costs, although this is a slight fall on the 85% reporting the same in winter 2022. Amongst our service providers this proportion is higher (86%) although still a marginal decline from the 89% recorded six months ago. In contrast – and as expected - 91% of developers intend to pass on increased costs to clients, a rise on the 85% reporting the same six months ago.

Fig 36

Over the next year, we expect inflation in the operational costs of our data centre will force us to pass some or all these increases to our clients