es

es de

de it

itContents

Click to go to key areas of report

- Summary

- Introduction

- Ownership and Management

- Developers & Investors

- Opinions

- Skill shortages - threats to the industry

- Who’s in short supply?

- Skill shortages impact

- Supply chain

- Supply chain disruption impacting future data centre locations

- Inflationary Impact

- Will the clients pay?

- Power – The Ongoing challenge

The Liability of Legacy

To view a PDF of the report click here

Summary

The European economic outlook remains surrounded by an exceptional degree of uncertainty as Russia's war of aggression against Ukraine continues and the potential for further economic disruptions is far from exhausted. The largest threat comes from adverse developments on the gas market, the risk of shortages and the impact on energy costs, especially in the winter of 2023-24. Beyond gas supply, Europe remains directly and indirectly exposed to further shocks to other commodity markets reverberating from geopolitical tensions which will impact on bond markets and the availability of funds. Longer-lasting inflation and potential disorderly adjustments on global financial markets to the new high interest rate environment also remain important risk factors. Both are amplified by the potential for inconsistency between fiscal and monetary policy objectives. Yet against this backdrop the data centre sector remains buoyant with near 100% agreement that demand will either grow or remain the same in the coming 12 months. This sentiment is further underlined by indications that the degree of pre-letting required has fallen with the proportion of those who are prepared to green light developments having secured 25% or less pre-lease has risen from 0% to 14%. However, with further rising inflationary pressures forecast, 85% of our respondents expect to have to raise prices to cover costs. Will this accelerate the uptake of alternative power sources and ever more efficient design solutions?

82% of our respondents agreed that the current pressures will increase the demand for power efficient data space over the next three years. This represents a significant uplift on the two thirds that expressed this same opinion 12 months ago, but will it translate into action? Our survey suggests that this is the case and is underpinned by approaches taken in our new developments. We have seen that rising fuel costs have accelerated a move away from diesel to using HVO which is supported by our survey showing that 69% of respondents are looking at these alternative fuel sources. We are seeing increased investment in hydrogen fuel cell technology, notably by the likes of Microsoft, to replace diesel generators. Indeed, in February this year, Dutch data centre company NorthC became the first European data centre to install hydrogen fuel cells for emergency power. The pursuit of green, renewable energy continues with various targets committed to; this needs to be accelerated in conjunction with governments as power grids by and large remain unfit for purpose. Another leap forward is the use of AI-assisted automatic cooling control by using sensors to identify energy waste and deploying software management platforms to maximise efficiency is much more efficient than manually monitoring power. Equinix estimates automated power monitoring could improve energy efficiency in data centres by as much as 30-50%. However, this is looking forward, legacy data centres still consume huge amounts of energy at far greater PUE’s than their modern and future counterparts, when does legacy become liability? At BCS we are addressing these legacy challenges through cost effective and sustainable solutions to pave the way for a net zero future.

James Hart

CEO

Introduction

Welcome to the 25th data centre survey undertaken by independent research firm, iX Consulting and sponsored by BCS, offering integrated solutions through IT asset consultancy.

The phrase “May you live in interesting times” – attributed as an ancient Chinese curse - is thought to assign a hidden degree of malevolence; wishing the recipient uncertainty and disorder rather than a tranquil existence suggested by a more superficial interpretation. There is little doubt that we are now living in interesting times. The global political, economic and social realms are all characterised by degrees of uncertainty and disorder at present, with consequences reverberating across all regions and nations in varying measure.

Whilst Europe now appears to have moved past the worst health consequences of the pandemic – largely due to the successful application of vaccination programmes, global supply chains are still being affected. The ongoing adoption in China of widespread lockdowns across impacted areas continues to disrupt both demand and production levels in that country. Allied to this the ongoing Russian war on Ukraine continues to cause economic upheaval with major consequences for the availability and cost of gas, oil and related industries.

The inflationary fallout of this is being felt across Europe with economic growth facing a heavy toll. Indeed, a recent IMF projection suggested that more than half the countries in the Euro zone will face recessions this winter. In the UK, the Bank of England has warned that the country could potentially face a recessionary period for the next two years.

Fig 1

What is your primary relationship with the data centre industry?

So interesting times indeed, illustrating why those suppliers and consumers across the European data centre industry are now facing some of the most serious challenges of the last 20 years. This provides the context against which our latest survey on the current state and prospects for the European data centre industry was undertaken.

The report captures the views of a wide variety of professionals working in the industry, including owners, operators, developers, and investors of facilities, consultants involved in the building, selling, and renting and end-users who either own and run their own buildings, or occupy a third-party’s space.

In all, the research now includes the views of participants who either occupy or control around 5.4 million square metres of technical real estate across 39 countries of Europe.

Fig 2

Total Technical Floorspace

Fig 3

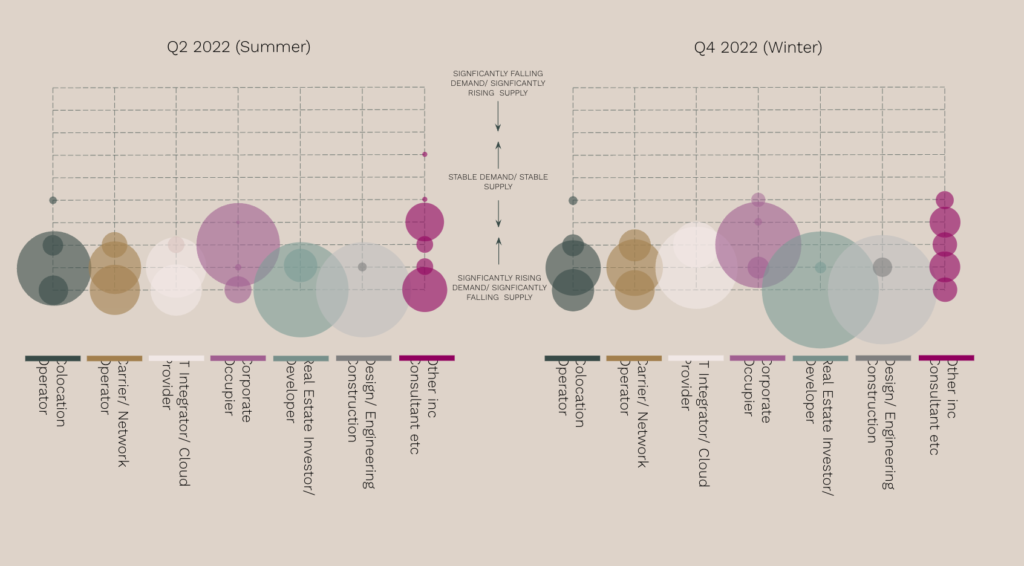

The Supply/Demand dynamic

Fig 4

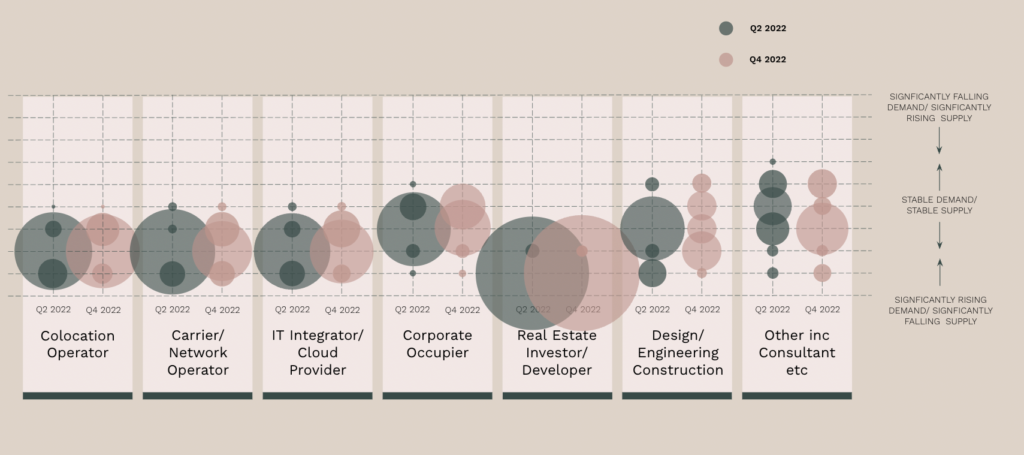

- Despite the wider economic challenges, the European data centre market continues to be characterised by falling supply and rising demand levels; a view held by 85% of our respondents unchanged on that recorded in our previous survey six months ago.

- Again, for the second survey in succession there is near-universal consent amongst respondents that demand will either increase or remain the same over the next 12 months.

- Developer and investor respondents remain the most confident in terms of market sentiment, with all expecting a continuation of rising demand over the next 12 months, a trend identified for the fifth successive survey.

- Most suppliers of data centre services also remain positive around the balance between supply and demand in the market, with all colocation providers seeing rising demand; marginally up on the 97% recorded six months ago.

- Similarly, carriers/network operators and IT integrators are confident, with well over 90% believing the coming year will be characterised by falling supply and rising demand, a similar proportion to that recorded six months ago.

- Corporate respondents remain cautious compared to the suppliers and owners, with just over 60% indicating that they expect demand to rise over the coming year, a decline on the 74% who indicated the same in our summer survey. For the fourth survey in a row, no end-user reported that there may be a fall in demand.

Ownership and Management

Maintaining control of their own facilities remains a major requirement for our colocation operators, managed services providers, IT integrators and cloud provider respondents; some four-fifths of whom reported that 80% or more of their data centre portfolio was internally managed, a proportion in line with the long-term average.

This level of operational control allows service providers to be both flexible and speedy in their decision-making enabling them to satisfy changing client demands, whilst continuing to drive efficiencies through their environments without constraints a third-party provider may present.

In contrast with the popularity of this self-managed approach as the business model for service providers, the requirements of most corporate respondents continue to be very different. Amongst end-user respondents, a large proportion find the outsourcing solution an attractive option; nearly four-fifths of whom indicated that at least 80% or more of their portfolio is managed via a third- party, up from the 72% reported in our summer survey.

Whilst the benefits of third-party solutions are attractive to many – offering service flexibility and CAPEX savings on expensive data centre build-outs – for some there is evidence that a blended approach also appeals. This combines the benefits of both external and on-premise solutions allowing the user a greater degree of control over those elements of their infrastructure that they wish to keep internal for whatever reasons.

Utilisation

The ability to optimise their data centre footprints in the most efficient manner is a natural economic requirement for all our respondents – whatever the ownership model. This has been a constant feature identified in our survey work in over the past 12 years or so and will likely increase in importance as global inflationary pressures continue to erode profit margins across services.

All respondents want to ensure that a healthy balance is maintained between the need for sufficient flexibility for future business demands whilst out-goings on flex-space are minimised and wasteful costs capped.

There are marked differences when utilisation rates between on-premises and externally owned facilities are analysed. Once again, we see that the average utilisation ratio of third-party users continues to exceed those for internally managed solutions. Six months ago, we recorded that some 70% of respondents stated that they utilised over 80% of their outsourced technical footprint compared to 22% who utilised the same percentage of in-house managed facilities. Our latest survey shows these proportions have increased to 82% (third-party) and 36% (in-house).

Fig 5

How much of your current data centre space is active and being used?

Amongst corporates, the requirement to maximise the efficient use of any IT environment, and thus minimising costly under-used space, has meant that proportions are in-line with averages for third-party managed space (82%) but above average (44%) when reporting this high utilisation for their in-house managed facilities.

As with other users, service providers are driven by a need to maximise value regarding their third-party space, maintaining relatively high utilisation rates at about 80% in these facilities. In contrast, average utilisation rates amongst service/infrastructure providers of their own facilities tend to be lower (64%) allowing flexibility to respond quickly to new demand levels.

Expansion

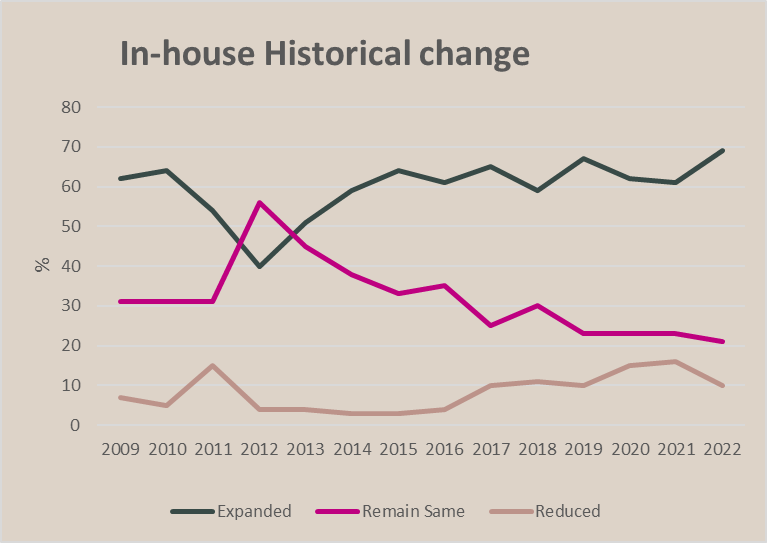

Despite the well-documented global turmoil, analysis of the views of our respondents suggests that the strength of demand for data centre services remains relatively buoyant across the European landscape, illustrated by the pattern of recent expansion projects of respondents and expectations on future short-term change. Over the past seven years, the proportion of our respondents who reported having expanded their on-premises facilities in the preceding six-month period has remained relatively consistent within a range of around 60-65%. In our most recent survey that proportion has increased to some 69% - up from the 63% reported in our summer survey. Around one-in-five reported no change whist some 10% reported a reduction in their in-house floorspace.

Fig 6

How has your total fitted technical floorspace altered over the past six months?

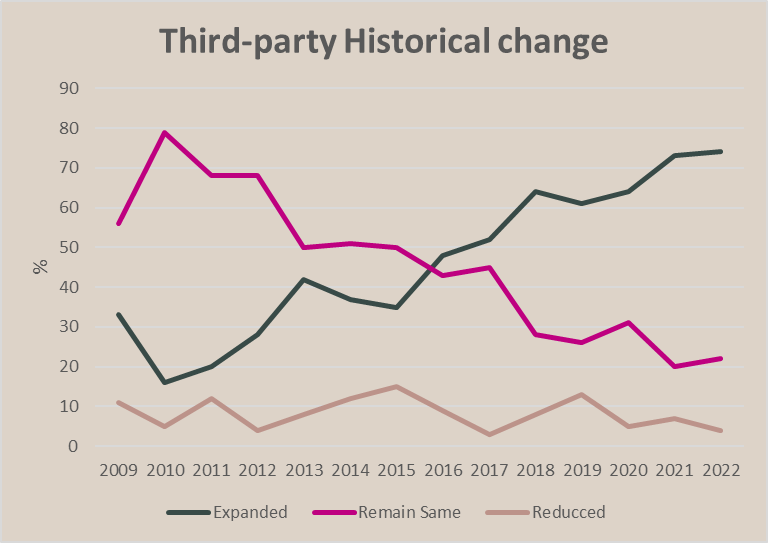

The number of third-party managed data centre expansions since our summer 2022 publication has remained fairly consistent; some 74% of our respondents indicated an increase in the previous six months compared to 76% recorded six months earlier. This is noticeably higher than the long-term average of some 53%. As with internally managed space around one-in-five reported no change in their third-party portfolio whist around one-in-twenty reported a floorspace reduction.

Fig 7

Amongst our service providers, colocation operators continue to lead the way in terms of expansion, with some 94% indicating increases of their own stock during the previous six months; up from the 87% recorded in the summer. This increasing level of expansion provides clear evidence that these service providers expect strong demand from end-users in the near term and are ensuring that they are positioned to respond quickly to meet this demand.

Amongst our corporate respondents, just 6% indicated an increase in their in-house technical floor space over the past six months; down from 16% in our last survey. At the same time, we have seen a decrease in the proportion who reported that they had reduced self-managed stock; 53% reported that this was the case compared to 63% six months earlier. We have seen a rise in the numbers of end-users reporting no change in their internal data centre portfolio

Fig 8

Fig 9

Corporate Sector – data centre proportion expansion

Despite this, the longer-term trend remains clear; end-users continue to favour an outsourced model for occupying data centre space where possible. Some 88% of these respondents reporting an increase in their externally manged data centres over the past six months, in line with that reported in our summer survey. Amongst our service providers some 79% reported an increase the number of third-party managed data centre expansions over the period – up from 74% reported in our last survey.

How was expansion achieved?

The choice of routes for expansion of self-managed facilities in our latest survey are similar to those recorded in the first half of 2022. The self-build route was again the most popular, with around 53% of respondents using it, a marginal uplift on the 49% recorded earlier this year. The option of purchasing or leasing through a development partner was pursued by around a third of respondents, the same levels recorded six months ago.

Around 14% reported that they have reduced their tech space through the decommissioning of a legacy facility, a small decline on the 17% reported in our summer 2022 edition with the vast majority of these being corporate end-users.

In terms of externally managed expansion, taking space from a colocation partner remains the most popular option with some 71% of respondents saying that they had chosen this route followed by IT integrators, carriers and network providers.

Fig 10A

If change has occurred via expansion or contraction how have you achieved this? In house

It is noted that several respondents indicated that they chose a multi-supplier route - expanding across several facilities over the period and adopting different strategies in individual cases i.e. what best suited at the time, in a certain geography; a decision generally driven by availability, suitability and/or cost.

Fig 10B

If change has occurred via expansion or contraction how have you achieved this? Third party

Expansion plans continue apace

The predicted expansion of internally managed data centre space, over the coming year has risen from 56% to 60% over the past six months across all our respondent groups. This represents a continuation in the recovery we have noted since the first half of 2020 in the immediate aftermath of the COVID outbreak when this proportion stood at just 21%.

Fig 11

What are your current expectations for changes to your ‘in-house’ technical data centre area?

Our service providers - Colocation/IT providers and carriers – are the most optimistic group amongst our respondents, with around 82% expecting to expand their in-house portfolio over the next 12 months, up from the 78% recorded last summer. The proportion of respondents indicating they would reduce their in-house data centre space remains small, standing at just 8% and unchanged on Q2 2022.

Whilst there remains a significant proportion (24%) of respondents who believe that there will be “no change” in the amount of their in-house data centre space over the next year, this represents a decline on the 32% recorded in our last survey. The number of respondents who are undecided on what they will do regarding their in-house estate rose from 3% recorded in our preceding survey to 8% today, a reflection of the uncertainty in the wider economies.

Fig 12

What are your current expectations for changes to your ‘third party’ technical data centre area?

Similarly, respondents’ attitudes toward third-party managed space fairs considerably better than was the case in early 2020; 61% of responders reporting their intention to expand over the coming year, a major increase on the 24% stating expansion intentions in the summer of 2020.

Some 52% of service providers expect to expand their externally owned facilities. For end-users, some 83% expressed their intention to expand in third-party data centres over the coming year. In addition, few expect to downsize their externally managed facilities over the next six months – just 4% of all respondents – although an increase on the 3% in Q2 2022.

The proportion of those who report there will be “no change” of third-party estate has risen marginally to 31%, from 29% six months ago, whilst the number of respondents who are undecided on what they will do regarding this metric fell from 10% last time around to 4%.

Drivers of Change

Over the past decade the most highly ranked factor driving changes in both internal and third-party controlled data centres identified by our respondents has been business expansion or contraction. Our latest survey confirms the extension of this trend, with around a third citing it as the top priority for both internal and external solutions; a similar proportion recorded six months ago.

For the third successive survey, demand for power and the costs associated with it has ranked second by our respondents as an important driver of change for both internally and externally operated space; 24% citing it as such, a rise on 20% reported in the summer. We noted in our summer survey that given the highly publicised inflationary pressures on energy costs that have been experienced, it may be a little surprising this proportion was not even higher; an observation worth repeating this time around, despite the rise that has been recorded.

We have seen a small uplift in those who cited budgetary issues as increasingly important; up from around 15% six months ago to around 17% this time around. This marginal increase in importance as a driver is noted in both in-house facilities and third-party managed floorspace.

Fig 13

What factors are/will be driving these changes?

The ranking of availability of appropriate data centre product by around 11% of respondents represents a marginal decline on the 10% in our last survey. Whilst changes in fiscal structures are cited by around 8% of respondents, largely un-changed overall from six months ago and data sovereignty continuing to be ranked near the bottom of the list, identified by around 8% of respondents, a decline on the 12% from our preceding survey.

Developers & Investors

No slowdown in supply plans

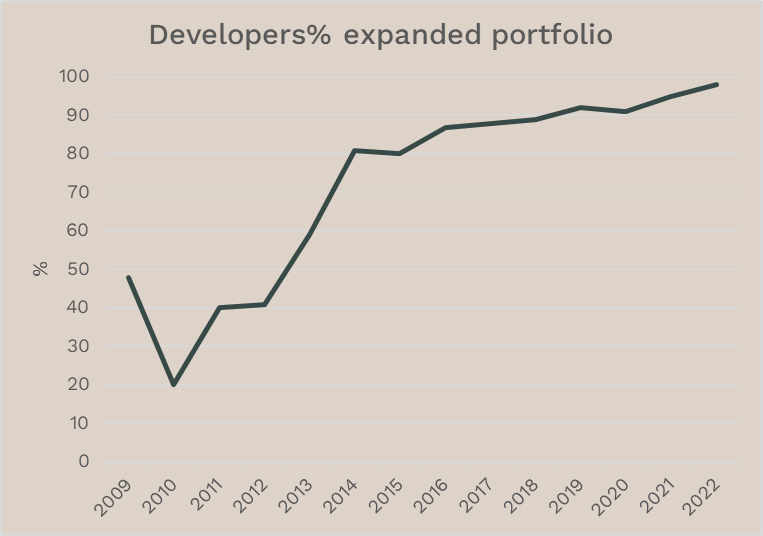

Despite the background of slowing global economic growth, the fallout of the Russian invasion of Ukraine and the residual impact of the pandemic on global supply chains, developer sentiment has proven generally robust over the past year or so. Indeed, even against that background almost all (98%) of our developer and investor respondents reported that they grew their data centre stock in the past 12-month period, the second successive survey that we have noted this high level.

Fig 14

Fig 15

Moving forward, there is little evidence of any potential slowdown in the delivery of new stock. Some 95% of developers and investors also stated that their intention is to expand their portfolio over the coming year, unchanged on that seen six months ago, matching the highest proportion recorded since 2013.

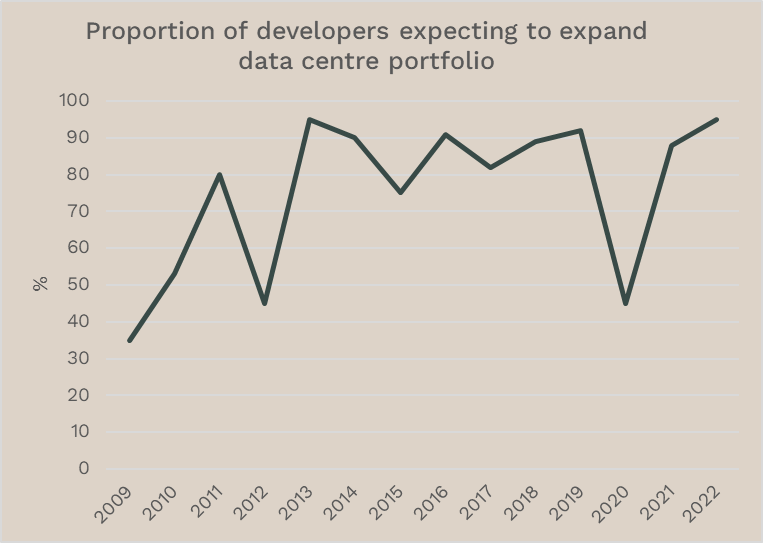

Developers and investors attitude to risk provides a useful barometer to gauge prospects for the market in the short to medium term. We have utilised the proportion of secured letting area that a scheme requires before construction can commence as a benchmark to measure this risk since we started this survey in 2009.

Fig 16

If it is your intention to develop more technical space during the next 12-18 months, on what basis will that be?

The results of our latest survey suggest that there has been in fact a greater degree of positive sentiment amongst developer respondents over the past six months with, on average, a lower degree of pre-letting required. The number of respondents requiring at least 75% or more of their scheme to be pre-committed has fallen from around two-fifths to around a quarter this time around. In addition, further evidence of this increased positivity is illustrated by the proportion of those who are prepared to green-light the build-out having secured a pre-lease on 25% or less has risen form 0% six months ago to around 14% this time.

Fig 17

For Wholesale transcations, what is the minimum lease length that you would accept?

One other measure of sentiment is the minimum lease length requirement for a wholesale transaction that a developer would like to achieve. Analysis of this metric provides further evidence of an increased positive attitude amongst these respondents with, on average, a lowering in the length of time that a developer is happy to secure on this type of transaction.

Our latest survey indicates that 14% would require a term of five years or more, a fall on the 21% noted six months ago. In addition, a further 27% would accept a period shorter than three years, up from 21% in Q2 2022 whilst over half (59%) of respondents suggested a three-to-five-year period would be needed, little movement on the 58% who suggested the same six months ago.

Ranking of choice factors for new data centre

The availability of power remains the single most important factor driving data centre choice amongst our respondents, with nearly three-quarters citing this as their number one driving choice in our latest survey. This represents a marginal increase on those who did so last summer. Indeed, amongst our developer and investor respondents the ability to have access to a secure and economic power source is rated even more highly, with around 95% placing it first.

Location remains as the second most popular factor, with just over two-fifths of all respondents ranking it in their top two choices, a proportion un-changed on six months ago and in line with to the long-term average. Moving forward the importance of location is unlikely to dimmish given current global political and economic uncertainty.

Linked to this is It is political or social stability which has become increasingly more important in recent surveys; 30% of our respondents in our latest survey rank it as one of their top two ranked factors. This survey has also seen a continuation of the trend that access to fibre is now viewed as an increasingly important factor with around 14% citing it as their most important choice – up from 10% six months ago.

Again, it should be noted that whilst factors such as the total build-out cost, availability of specialist data centre construction skills and land price were consistently rated behind our top factors by most respondents, both our developer and DEC (Design, engineering, and construction) respondents rated them more highly. For example, whilst total build cost was ranked in top two places by 23% of all respondents, this proportion jumps to a third amongst those professionals charged with the delivery of new supply.

Fig 18

Drivers Ranking – data centre choice

Opinions

Skill shortages - threats to the industry

For some years, the industry has been mindful of a potential threat to the delivery of enough new data centre stock; a shortage of sufficiently qualified professionals to deliver that stock. Initially concerns appeared around the design and build of new facilities but has also emerged in the fields of operations of data centres. Whilst these threats have been given more prominence in the last few years in the wake of international lockdowns and the imposition of restrictions on the movement of skilled labour to areas of demand, they are long-standing having emerged from the dislocation of the pace of growth of the industry and the pace of growth of attracting and training skilled labour resource.

Fig 19 A and B

- Across our respondent groupings there remains real concern over a skills shortage in the data centre industry. 96% of respondents believe that the coming year will see a decline in supply of staff, an uplift on the 91% reporting this in summer 2022, and slightly above the 93% who reported the same in Winter 2020 arguably at the nadir of the COVID-19 crisis across Europe.

- To further exacerbate the problem, some 90% believe that this will be accompanied by a rise in demand for such staff.

- For the third survey in a row there is near universal agreement amongst our developer respondents that the coming year will be characterised by significantly falling supply of staff whilst the demand for those skill sets rises; the highest degree of assent amongst all our respondent’s groupings.

- Design, Engineering and Construction (DEC) respondents share an almost identical response profile, universal belief that the next year will be characterised by a fall in supply of staff whilst the demand for those skill sets increases. This reflects a notable strengthening of belief contrasted with the 72% recorded in Winter 2020.

- Most suppliers of data centre services appear worried about this balance between supply and demand of labour; the majority of colocation providers carriers/network operators and IT integrators believing the coming year will be characterised by falling supply and rising demand. Where they differ from our developer and DEC respondents is in the degree of concern; just one-third of service providers couching their agreement in the strongest possible terms compared to 90% or more in the other groups.

- Amongst end-users, 84% believe that a rising supply of skilled staff would be met with falling demand – a marginal decline on the 88% who shared this view six months ago but represents a considerable uplift on the 44% who shared the same view just two years ago in Winter 2020.

Who’s in short supply?

Fig 20A

It is increasingly difficult to source sufficiently skilled design professionals to deliver our current projects

Our survey suggests that respondents have increasing concerns around shortages amongst design professionals; we have noted an increase in the number of respondents raising concerns from 72% six months ago to over 81% recently and back in line with the levels expressed toward the end of 2021.

Fig 20B

It is increasingly difficult to source sufficiently skilled build professionals to deliver our current projects

Concern amongst stakeholders in the European data centre industry around the issue of skill shortages is also evident around build professionals. Indeed, some 83% of respondents expressed their concerns that a shortage of sufficiently skilled build contractors existed, an increase on the 78% who suggested the same in the first half of the year.

The perception amongst our respondents is that although there are difficulties in sourcing operational staff for their data centres, these problems are less acute than at the design and build stages. Some 68% expressed their agreement when asked about the shortages of sufficiently skilled operations staff, a decrease on the 75% recorded previously.

Fig 20C

It is increasingly difficult to source skilled operations professionals to deliver our current projects

The strength of agreement does vary amongst our respondent groupings. Perhaps not surprisingly our DEC respondents expressed their concern over skills shortages in the most robust terms, with universal agreement that shortages exist at both the design and build stages – the second successive survey that this level has been recorded. Similarly on both design and build metrics, our developers also express universal agreement that they are facing increasing difficulties in sourcing skilled professionals.

Amongst our service providers the strength of belief in design and build skill shortages is slightly less pronounced, nevertheless, 81% and 88% respectively of these respondents agreed that shortages are problematic.

For end-user respondents, a belief in shortages of skilled operational staff pose the biggest problem – 88% compared to 84% six months ago. In contrast just 61% for design professionals and 50% for build professionals. Nevertheless, in both cases of design and build, this represents a significant uplift on the proportions recoded six months ago – 50% and 23% respectively. Whilst these end-users have been increasingly using outsourcing solutions meaning many of these are not exposed to the early stages of data centre delivery and thus limited direct experience of any problems associated with it, this perceived awareness amongst this group may indicate the increasing acuteness of these problems and serve as a more substantial warning.

Once again, we have noted widespread agreement amongst our respondents that job shortage concerns, are spread across a variety of specific job roles. Indeed, most identified multiple roles as areas of concern. In the construction sector for example around 60% of respondents stated that they had experienced shortages of quantity surveyors, site managers and site engineers within the past year.

Within the operational sphere, around 65% of respondents stated that they have had direct experience of shortages amongst operations and network engineers/technicians over the past year, with a slightly lower proportion – around 60% - seeing a shortage of infrastructure specialists over that period.

In addition, Mechanical & Electrical project managers were also highlighted as an area of concern around the availability of skilled workforce – just over 60% cited shortages amongst this skill set as problematic.

Skill shortages impact

Certainly, in the case of build and design professionals, the debate around potential shortages of skilled labour is centred on the potential impact for the delivery of new data centre space and subsequent consequences for the end-user. When questioned on this, our respondents are unequivocal in their assertions that these impacts are real and are being keenly felt. Indeed, most respondents noted a multitude of factors when quizzed on these impacts.

Fig 21

In the past year we have experienced the following as a direct result of skill shortages

The most cited impact is that these skills shortages have placed a greater workload on existing staff, nearly nine-out-of-ten noted this as the case, the same proportion recorded six months ago.

The shortage of staff has inevitably led to increasing operating/labour costs recorded by 87%, a rise from the 83% reported last summer. Such shortages also can be seen as a contributory factor in the increasingly popularity of the use of outsourcing options, with around 52% citing it as such, marginally up on the previous survey – 51%,

Encouragingly, it appears that fewer respondents are finding it difficult to resource existing work this year than was the case earlier in the year with just over 43% stating that they had experienced difficulties in meeting deadlines or client objectives, down from 52% six months ago and well down on the 70% who cited it as factor at the beginning of the pandemic in Summer 2020.

In addition, around 48% stated that shortages had led to delays to developing new products/innovations, marginally up on the 44% reported in our last survey, whilst the proportion that noted they had ceased offering certain products or services has also risen to 14% to 17%.

However, the more extreme consequence of skills shortages is lost orders, with 8% of respondents still believing that this happened, this is in line with the levels identified six months ago, but well down on the 20% who recorded the same a year ago.

Supply chain

Fig 22

We have experienced considerable supply chain volatility over the past year

The ongoing fall out of the pandemic – the Chinese government’s continued use of lockdowns in response to further outbreaks of COVID and the Russian invasion of Ukraine, has led to ongoing problems with global supply chains. The data centre industry is not immune to these disruptions and our survey results continue to reflect this. Some 88% of our respondents stated that they had experienced such an eventuality in the past year, a proportion in line with the 87% recorded in our preceding survey.

These disruptions continue to be felt the hardest amongst our build professional respondents who reported experiencing supply chain volatility over the period - some 82% of our developer/investor respondents group expressing their assent in the strongest terms, up from 63% recorded six months ago. In addition, some 70% of our design engineering and construction group expressed the same degree of agreement in the strongest terms.

For the second survey in a row amongst our service providers, there is also near unanimity regarding this disruption – 97% stated that they had experienced such supply chain problems.

Fig 23

Regarding the base construction of our data centre(s) in Europe, we have experienced the following:

Supply chain disruption is a major contributory factor alongside related geopolitical issues – in impacting economic growth. It continues to pose some serious channellings to the wider construction sector and of course within that, those tasked with providing new technical real estate.

Whilst in our summer survey we noted some easing in the degree of challenge being faced in the sourcing of construction raw materials for example. To some extent we have seen a reversal of this in the past six months. Our respondents have reported increased difficulties in getting hold of these materials rising from 42% to 44% in the case of steel and 38% for cement and concrete up from 32% six months ago. In contrast our respondents report that there has been some minor easing in the sourcing of cladding and dry lining materials.

Supply and demand tenets dictate that shortages of a particular material will inevitably lead to a rise in price for that product. According to our respondents the associated costs with data centre builds – raw material unit and transportation costs as well as construction labour costs have all reportedly risen over the past six months. In the case of raw material unit and transportation costs, the number of respondents reporting that trend has risen from around 75% to around 80%. In the case of labour costs this proportion has jumped from 62% last summer to around three-quarters.

Unsurprisingly amongst our developer respondents - over 90% - reported experiencing rising costs across all three of these metrics with universal agreement of higher raw material costs. Amongst our DEC respondents, around 88% have reported experience of rising raw material unit and transportation cost rises as well as construction labour costs – up from 80% six months ago.

Supply chain disruption impacting future data centre locations

As we have noted geography remains a strong determinant for our respondents when identifying new data centre credentials. Indeed, over a long period, it has ranked second only to the availability of power in a top list of contributory drivers.

Fig 24

Potential long term supply chain problems will impact significantly on our decision making regarding the future location(s) of our data centre(s)

Some 54% of our respondents report that if current supply chain difficulties remain then it will significantly impact their decision-making regarding future locations for their data centres. This does represent a fall form the 60% recording the same in our preceding survey but continues to be significant.

For the second survey in succession, it is our DEC respondents who were the most fervent in agreement, with some 92% expressing their agreement up from 85% six months ago. Service providers appear less concerned than others, with 54% in agreement, trending down from the 64% previously recorded.

Once again end-user respondents expressed both the lowest level of agreement – just 39% which is down on the 44% recorded in the summer survey – whilst also recording one of the highest levels of disagreement with 28%. Colocation operators were the most polar in their views, providing the highest levels of disagreement (34%), as well as a similar level of disagreement (33%), and just under a third adopting a neutral opinion.

Inflationary Impact

With inflation across the UK and much of mainland Europe at or near double digit levels we sought the views of respondents on how they believe this is impacting the operation of their businesses and the potential impact on their data centre strategies.

Fig 25

Labour and materials’ inflation has led to a re-evaluation of our new data centre project and its subsequent postponement for….

We have already seen our respondent’s strong acknowledgment that they have experienced rising costs for both materials and labour costs as well associated transportation expenditure. Given that, we wanted to ascertain whether these rises have forced our participants to review their timing on their data centre projects.

In general, there is little evidence that such rising costs are going to impact the number of data centre projects proposed by our respondents moving forward. Over the short term around 6% stated that such a re-evaluation had taken place, 2% over the medium term and some 4% stated that such a review had led to a postponement of a project for the foreseeable future.

Indeed, the majority of respondents reported no impact in the short (79%), medium (79%) or long term (74%), whilst over the same time frames – some 21%, 19% and 16% expressed a neutral opinion. This may indicate a degree of uncertainty remains amongst respondents as they continue to assess the market indicators.

Amongst our service providers, the proportion who reported postponements remained low at 3% (short term), 2% (medium term) and 4% (long term). Amongst our developer respondents none suggested any postponements of their projects.

With end-users, there were no also reported postponements over the medium term or longer, but some 6% reported that they re-evaluated projects over the next 12-24 months and had subsequently postponed them. It should be noted that it is not clear whether these relate to in-house projects and the expense associated with them but if so, some could choose to follow a less capital expensive alternative via a third-party provider.

Will the clients pay?

Rising costs in an industry pose a dilemma for any business. A decision needs to be made as to the extent which that business is prepared to absorb such rises or pass them – either wholly or partially - onto their client base. There is strong evidence that our respondents have already felt the need to pass higher costs on to their clients, with an average of 52% reporting having done this in the last 12 months. Amongst our service providers this rises to 59% and amongst developers just 40%. Notably, around 30% have expressly refrained from doing so.

Fig 26

Over the past year, inflation in the operational costs of our data centre have forced us to pass on some or all these increases to our clients

Inflationary prospects for the coming year are not positive. Looking forward over the period some 85% of our respondents expect to have to raise prices to cover increasing costs. Amongst our service providers this proportion rises to some 89% with 85% of developers also intend to pass on increased costs to clients.

Fig 27

Over the next year, we expect inflation in the operational costs of our data centre will force us to pass some or all these increases to our clients

Power – The Ongoing challenge

The sourcing of affordable and renewable power is an enduring challenge facing all businesses and is magnified in the data centre industry as power plays such a large part of the core service. Given recent global events and the subsequent inflationary pressure on power costs, this challenge has undoubtedly risen to the top of respondent’s concerns. With growth for digital services forecasted to remain strong, the industry needs to respond to the increasing power demands created as a result, with the question of sustainability arguably never so important as it is today.

Consumption unlikely to diminish

There is little sign amongst our respondents that power consumption is likely to fall in the foreseeable future. For the second survey in succession, some 84% of respondents reported that they expect their power consumption levels to rise over the next three years, an increase from 76% recorded this time last year.

Amongst our service providers this proportion is even higher at some 95%, up slightly from the 93% we reported just six months ago, whilst 62% of end-users expect power consumption levels to rise over the period.

Fig 28

Over the next three years, we expect our power per sq meter consumption to:

Average Rack Power/cooling levels to rise?

In terms of our respondents’ expectations on their average rack power/cooling levels over the coming year, results for the current survey indicate a very similar profile to our those recorded in the summer. Just over a quarter of respondents expect to see an average rack power/cooling level of 9kw-12kw. In addition, a further 17% expect to see this level move to 12kw-15kw within the next 12 months. Whilst still only representing a small proportion of respondents, the near doubling from 4% to 7% who indicated that they would see a level higher than 15 kw per rack over the next 12 months is a notable increase.

Fig 29

What is your expectations for your average rack power /cooling level iby the end of the year

Amongst our corporate respondents, around 33% are expecting to see average rack power/cooling level of 3kw-6kw whilst 40% suggest their average levels will be in the 6kw-9kw range.

Cost of power – an efficiency driver

The recent considerable rise in energy costs and the impact on global economies that it has had – double digit inflation across much of Europe for example - will only encourage enterprises to look for more efficient solutions to limit their exposure to such cost increases. Some 82% of our respondents expect a rise in the cost of power to increase the demand for power efficient data centre space over the next three years. This reflects a marginal increase since Q2 this year but a significant uplift from the two-thirds who expressed the same opinion a year ago.

Amongst our service providers, there continues to be almost universal agreement that this outcome will be the case; 96% believed this, unchanged from six months ago. In addition, some 67% of end-users agree, substantially up from the 44% recorded earlier in the year.

Fig 30

We expect a rise in the cost of power in Europe to increase the demand for power efficient data centre space over the next three years

Move to renewables

There is little doubt that the industry is committed to moving away from non-renewable sources of power. Our survey participants continue to illustrate that commitment with over four-fifths once again agreeing that they expect the sourcing of power for data centres to be at least 90% from renewable sources by 2032.

Amongst our service providers this portion jumps to some 88%., albeit marginally down the 93% reported six months ago. Once again, our developer and investor respondents were almost universal in their agreement that 90% or more of their power will stem from renewable sources in the next 10 years.

Fig 31

We expect that the sourcing of power for our data centre in 2032 will be 90% or more sourced from renewable sources

The current geopolitical situation is also likely to encourage a move towards power sourced from renewable energy as the nature of this source is more likely to be locally generated and therefore less likely to be affected by other global factors, and therefore potentially enhancing stability of provision and pricing. Around 70% of respondents agreed that current events would encourage them to move more rapidly down this route. Amongst end-users this proportion was even higher at some 83%. Amongst service providers whilst 70% shared this belief, around a quarter remained neutral, possibly an indication that they are already quite far down the route of renewable sourced power already.

Fig 32

In the light of recent geopolitical events, we will pursue an accelerated move towards renewable energy sources for our data centre(s).

Notably, only around 10% of our responders presently reported that they secured their energy from a single source, a proportion which has remained un-changed over the past two years. This low level of single source of power reflects to some degree the global nature of some of our respondents. These participants have a multitude of facilities across their portfolio meaning that they are likely to source power as and when, looking to secure the best-in-class power solution for individual facilities.

Across Europe for historical and political reasons, sourcing respective national grids vary greatly which impacts on the potential sources available. For example, to source wind power may be easier in Denmark where according to Statista, almost half of electricity generated in the country is derived from. In contrast wind power contributed around 26% of the UK’s total electricity generation in Q4 2021 (Source: National Grid).

Around a quarter of our respondents’ data centre portfolio is powered only from a mix of renewable sources including solar, hydroelectric/tidal and wind farms/turbines, in line with the proportion recorded earlier this year - 27%. However, it should be noted that around half of our respondents utilise some degree of gas or coal power in their facilities - up from the 45% reported in the summer – and around 5% source energy solely from finite natural resources such as gas and coal. Nuclear power is noted as a source of power by around 20% or respondents in at least part of their portfolio, down from the 25% recorded six months ago.

Fig 33

Current Power sources

Looking forward we asked our respondents to try to assess their expected average share of sources of power across their data centre real estate in the next five years. Whilst fewer than 10% suggest that their facilities will be sourced from a single type of renewable power, most respondents expect to see a rise in the proportion of power from renewable sources to service their data centre facilities.

Fig 34

Future Power sources

Moving forward gas or coal power in our respondents’ facilities is encouraging – expected to decline from around 50% now to around 29% over the next five-year period. In addition, nuclear power is expected to remain as a source of power by around 25% of respondents on at least part of their portfolio, a small fall from the 29% recorded six months ago

Use of waste energy

The desire - and regulatory imperative - to move to more sustainable sources of energy across society underpins the data centre industry’s drive to find solutions to its own needs regarding the power issue. One potential element increasingly under discussion is that of the use of waste heat energy generated by data centres.

Fig 35

Over the next 5 years, the economic viability of waste energy programmes needs to improve greatly in order for us to consider

However, question marks exist over the efficiencies of power generated in this way. This uncertainty over the economic viability of such programmes causes concern amongst respondents, with some 73% suggesting that the economic metrics of such programmes needs to improve greatly for them to consider such measures over the course of the next five years.

In our summer 2022 report we noted that a potential limitation around adoption of these systems is the belief that waste heat utilisation is only an economically viable option for data centres that are already near existing district heating systems, with 59% of respondents indicating this. Our latest survey has shown a firming of this attitude with around two-thirds of our respondents now reporting the same. Amongst our service providers the degree of agreement with these jumps to 75%.

Fig 36

Waste heat utilisation is only an economically viable option for data centres that are close to existing district heating systems

In addition, when questioned on the issue of the utilisation of waste to energy – the burning of waste to produce electricity excluding biomass - as a primary power source, our respondents expressed further doubts regarding its viability as such. Some 72% stated their belief that current limitations to maximum permitted uptimes – at around 98% led to this, albeit this represented a marginal decline on the 75% recorded in our last survey.

Once again, some four-fifths of service providers believe that to be the case – a proportion which rises to above 90% in the case of integrators. However, some 59% believe that waste to energy sources could be considered as a secondary power source, a similar proportion to what was reported six months ago.

Fig 37

Current limitations to maximum permitted uptimes – at around 98% – mean that waste to energy sources is not a current viable option for us as a primary power source

Fig 38

Current limitations to maximum permitted uptimes – at around 98% – mean that waste to energy sources could be considered as a secondary power source to add resilience

Retro-fit solutions

As our respondents look for greater efficiencies and enhanced renewable energy solutions to meet regulatory requirements around net zero targets, they are prepared to consider a variety of solutions. One of which is to retrofit existing technical facilities – adapting existing data centre facilities to enable them to adopt or enhance renewable energy power sources.

Almost two-thirds of our respondents agree that retrofitting of existing facilities is something that they would be prepared to consider, a similar proportion to that seen in our summer survey. This is particularly supported by our service providers - carriers (87%), colocation operators (86%) and integrators (79%).

Fig 39

We would actively look to retrofit energy production solutions (i.e. solar, turbines, waste-to-energy) at our data centres to accelerate the move towards our Net Zero requirements.

One notable bi-product of the cost-of-living crisis and rising fuel costs for the data centre industry has seen further consideration given by our respondents to replacing diesel as the primary source of fuel for back-up generators. Of course, the social and regulatory push for net zero targets to be achieved have long under-pinned the industry’s search for cleaner and more efficient sources of power. It is therefore not surprising that some 69% of respondents acknowledge that the latest fuel prices increases have led them to look for alternatives to diesel for their back-up power generators. Our service providers were the clearest, with 84% acknowledging their agreement.

Fig 40

Increasing fuel prices have forced us to look at alternatives to diesel for our back-up power generators