es

es de

de it

itContents

Click to go to key areas of report

- Executive Summary

- Introduction

- Ownership and Management

- Developers & Investors

- Opinions

- Skill shortages - threats to the industry

- Who’s in short supply?

- Skill shortages impact

- Supply chain

- Supply chain disruption impacting future data centre locations

- Power – The ongoing challenge

- Average Rack Power/cooling levels to rise?

- Power efficiency increasingly attractive driver

- Move to renewables

- Can the industry be trusted to self-regulate?

- Should the industry self-regulate?

- Use of waste energy

- Retro-fit solutions

Summer 2022: Change or be Changed – The Looming Threat of Regulation

To view a pdf version of the report click here

Executive Summary

With the backdrop of economic indicators that suggest that stagnation and recession are at the foremost in the thoughts of the markets, the world bank president David Malpass recently commented ‘The war in Ukraine, lockdowns in China, supply-chain disruptions, and the risk of stagflation are hammering growth. For many countries, recession will be hard to avoid’. This makes the optimism shown by our respondents on the current state and future growth prospects of our sector even more remarkable. Within this environment we’ve seen a 5% increase in respondents seeing a rising demand against a falling supply and is underlined by a near 100% response that demand will either rise or remain the same over the next 12 months. With this rising demand, the questions raised in previous reports around energy supply and emissions coupled with sharply increasing costs remain. We are also starting to see Governments around the world reactivating or increasing energy production from fossil fuels, placing climate targets under pressure. Will this lead to governments to legislate against softer targets, such as happened to the aviation industry, to appear to maintain commitments and what does this mean to the data centre sector?

In 2021, representatives from the data centre trade associations and companies signed the European Green Deal. The European Green Deal is the EU’s ambitious and comprehensive plan to become the first climate neutral continent and fundamentally transform the European Economy in which taxes and incentives are critical to its success. Whilst this initiative is currently self-regulatory, a recent survey undertaken by PWC suggested that fewer than half of organisations are prepared for the EU Green Deal. With ambitious targets to be achieved by 2025 and 2030, it begs the question that if our sector doesn’t get ahead of these targets will the self-regulatory initiative become legislative and regulated? We have already seen moves within the tier 1 cities of Europe to curb data centre developments and protect energy capacity using the planning and permitting process. We believe our sector is at a crossroads with one route being proactive, investing in new technologies, self-generation and looking at innovative storage solutions to reach climate neutral targets. The other route is having legislation and regulation imposed on us and having to react to the imposition of energy, water and emission targets that we have no influence over. Whilst we at BCS do not have all the answers yet, we are helping clients navigate the transformation that is necessary to prosper in the Green Deal environment. Our current services include informing clients of Green Deal levies, the financial modelling of impacts and supply-chain transformation that will form the map to reach our green destination.

Introduction

Welcome to the 24th data centre survey undertaken by independent research firm, iX Consulting and sponsored by BCS, offering integrated solutions through IT asset consultancy.

After two difficult years, much of Europe now appears to be emerging from the worst direct impacts of the pandemic, through a combination of intense vaccination programmes and daily management to live alongside the virus. However, the long-term effects of the global pandemic, coupled with new geopolitical issues mean that the world now faces some robust challenges. Whilst an economic slowdown across Europe may have its own consequences for growth in our industry, perhaps the most immediate and stark issue is the inflationary pressures on energy pricing that has already hit consumers and business.

The response by most world democracies to Russia’s invasion of Ukraine has led to gas and oil prices skyrocketing. This, allied to already prevalent rises in energy prices as the world addresses a move to more renewable and sustainable sources of energy, have added to power cost increases across Europe. This level of pressure on power costs is unprecedented.

In addition, ongoing supply chain difficulties continue across all sectors, compounded by China's ongoing strict COVID-19 restrictions which have reduced factory production and curbed domestic demand. The supply of electronics has been hit particularly hard with Asia-based chipmakers struggling against the rise in cost of raw materials and shortage of qualified staff for technical manufacturing jobs. None of this is likely to end soon as the shortage of semiconductors is predicted to continue this year, leading to project delays, postponement and potentially cancellations. With all these pressures, the European data centre industry faces perhaps one of its most difficult phases for over 20 years, with builders, owners and occupiers all being asked to address some tough issues.

Fig 1

What is your primary relationship with the data centre industry?

It is against this background that our latest survey on the current state and prospects for the European data centre industry was undertaken. It reflects responses from real estate developers and investors, corporate occupiers, colocation providers and IT and telecom service providers, as well as design and build specialists, consultants and other key market practitioners across Europe.

In total, we analysed the views of respondents who controlled data centre portfolios of around 5 million square metres of technical floor space across some 38 countries; a fivefold increase in survey coverage since we began in 2009.

Fig 2

Total Technical Floorspace

Fig 3

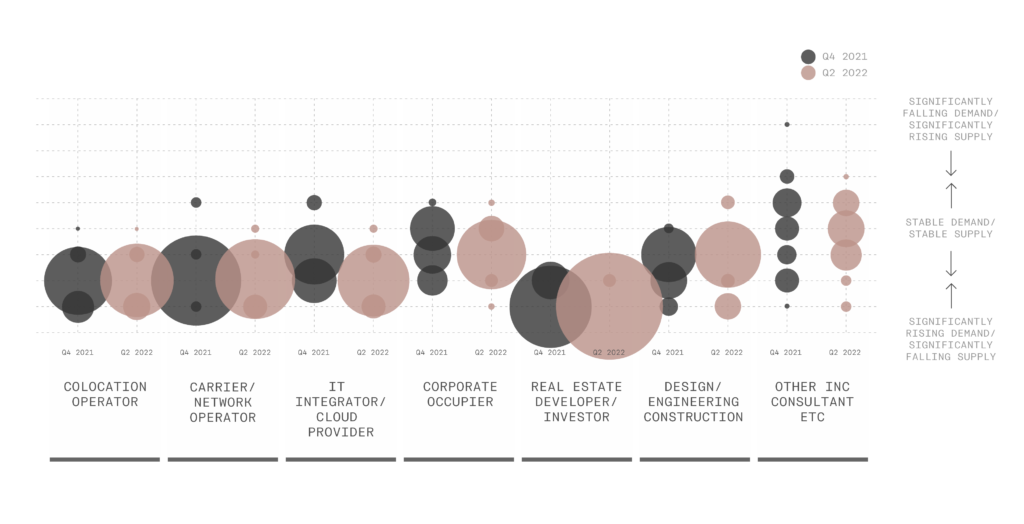

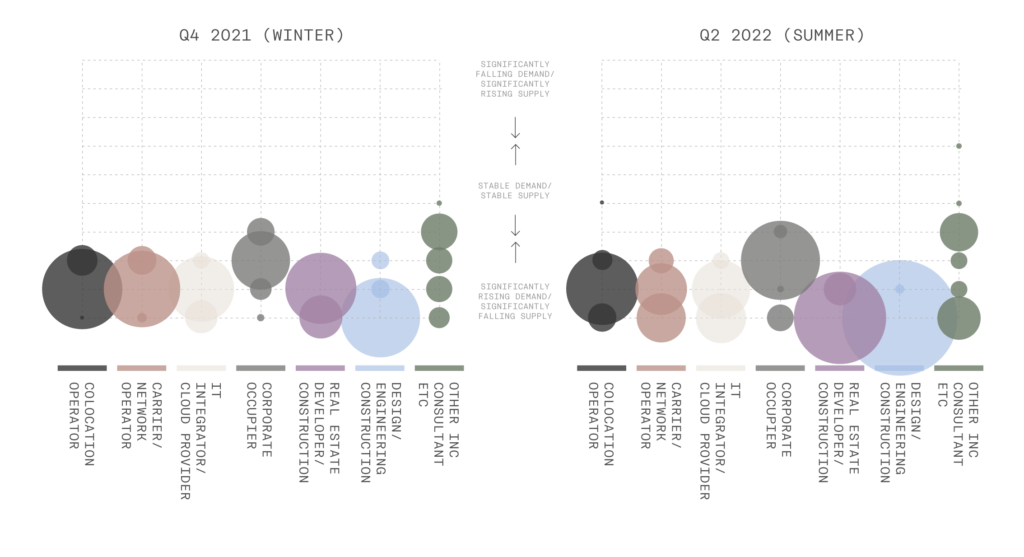

The Supply/Demand dynamic

Fig 4

- Despite the difficulties on the global landscape, our respondents suggest that the European data centre market continues to be characterised by falling supply and rising demand levels; a view held by 85% of our respondents, an increase on the 80% recorded in our previous survey six months ago.

- Our latest survey suggests that there is near-universal consent amongst respondents that demand will either increase or remain the same over the next 12 months.

- Once again developer and investor respondents remain the most confident in terms of market sentiment, with all expecting a continuation of rising demand over the next 12 months.

- Most suppliers of data centre services remain positive around the balance between supply and demand in the market, with 97% of colocation providers seeing rising demand, a similar proportion recorded six months ago.

- Carriers/network operators and IT integrators are confident, with just over 90% believing the coming year will be characterised by falling supply and rising demand.

- Corporate respondents continue to be the most cautious group. However, with 74% recording they expect to see rising demand and falling supply, this is still a notable increase on the 56% in our last survey. A further 26% indicate that they expect demand to remain stable over the coming year. For the third survey in a row, none of our corporates reported that there may be a fall in demand.

Ownership and Management

Colocation operators, managed services providers, IT integrators and cloud provider respondents continue to view the need to own or manage their facilities as fundamental to their business model as it allows them the degree of control and flexibility to respond promptly to changing demand requirements.

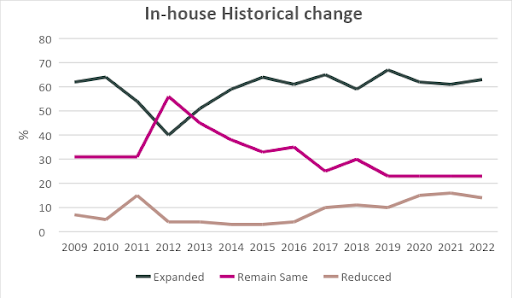

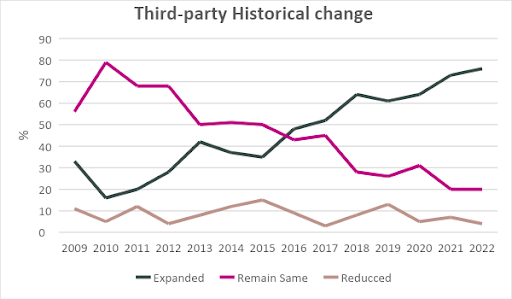

- over three-quarters reported that 80% or more of their data centre portfolio was internally managed, a proportion in line with our long-term average.

In contrast, over the years we have monitored the definitive move of our corporate respondents away from ownership and management, with a focus on the outsourcing of a data centre solution.

- 72% of end-users indicated that at least 80% or more of their portfolio is managed via a third- party, a proportion just above the 69% monitored in our last survey

With demand for cloud services witnessing substantial growth in the wake of corporates expanding their use of IT services, and consumers moving towards the Internet of Things, it is likely that externally managed space will continue to play an important part in the infrastructure to support the delivery of those services.

Utilisation

With both ownership and third-party structures, the pressure is high to maximise the use of the data centre asset whilst maintaining flexibility and vacancy for swift deployment in response to demand. Arguably, taking third-party space on contract can offer more flexibility to match your internal demand with your contracted space than the ownership route. Indeed, if we look at utilisation rates, the average utilisation ratio of third-party users continues to exceed those for internally managed solutions.

- Six months ago, our survey reported that 71% of respondents stated that they utilised over 80% of their outsourced technical footprint compared to 27% who utilised the same percentage of in-house managed facilities.

- Our latest survey indicates a continuation of this, with the proportion of those having utilisation rates of externally managed solutions of 80% or more remain constant at 70% whilst the rates of 80% plus of in-house utilisation has fallen marginally to 22%.

Amongst corporate occupiers, the requirement to maximise efficiencies in externally managed data centres – minimising expensive under-used space - has meant that this proportion is marginally higher at over 72%. Service providers, driven by a need to maximise value for money regarding their third-party space, maintain relatively high utilisation rates at about 76% in these facilities.

Fig 5

How much of your current data centre space is active and being used?

Expansion

The ongoing strength of demand for data centre services continues to be illustrated by both the pattern of recent expansion and expectations on short term change that our respondents have reported.

Fig 6

How has your total fitted technical floorspace altered over the past six months?

- The proportion of respondents who indicated that they have increased their in-house managed data centre capacity over the past six months remains at around 63%; a very small uplift on the 61% recorded in Q4 2021.

Fig 7

- Much of the impetus behind this expansion has come from our service providers, this proportion rises to some 87% in agreement; unchanged on the figure recorded six months ago.

- For many respondents utilising a third-party solution remains a popular choice; 76% of whom indicated that they had increased their third-party managed data centre capacity over the past six month, a rise on the 73% we recorded in the preceding survey.

- For end-user respondents, outsourced solutions remain even more attractive with the number of those stating that they had expanded their technical floorspace within such facilities rising from 80% in Q4 2021 to 89% today.

Fig 8

Fig 9

Corporate Sector – data centre proportion expansion

- Interestingly, the number of corporate respondents who have reported an expansion in their own facilities has more-than doubled from 7% six months ago to 16% this time around and reflects a return closer to the long-term average of 14% that has been monitored during the last ten years.

How was expansion achieved?

- The choice of routes for expansion of self-managed facilities in our latest survey has changed a little to those recorded in the latter half of 2021. Whilst the self-build route was again the most popular - with around half of respondents using it - this represents a marginal decline on the 58% recorded six months earlier.

- The option of purchasing or leasing through a development partner was followed by 33% of respondents; up from the 20% recorded six months ago.

- Some 17% reported that they have reduced their data centre space through the decommissioning of a legacy facility, similar to that reported in our Winter 2021 edition - the majority of these being corporate end-users.

Fig 10A

If change has occurred via expansion or contraction how have you achieved this? In house

- In terms of externally managed expansion, taking space from a colocation partner remains the most popular option with some 70% of respondents saying that they had chosen this route, followed by IT integrators, carriers and network providers.

- Once again, several respondents indicated that they have chosen a multi-supplier route, suggesting that the choice of route to market may depend on a number of local factors that decide the best suited approach rather than sticking to a single supplier model approach.

Fig 10b

If change has occurred via expansion or contraction how have you achieved this? Third party

No slowdown in expansion plans

The future levels of expected demand for technical real estate and services shows no signs of slowing.

Fig 11

What are your current expectations for changes to your ‘in-house’ technical data centre area?

- Looking forward well over half of respondents (56%) expect to expand the size of their internal data centre capacity portfolio over the coming 12-month period; a proportion unchanged since our last survey.

- Colocation/IT providers and carriers continue to be the most optimistic group amongst our respondents, with around 78% expecting to expand their in-house portfolio over the next 12 months.

- Third-party data centre solutions will remain popular over the next year with 58% of respondents stating that they will expand their technical floorspace within such facilities rising from 49% just six months ago.

- The proportion of respondents indicating they would reduce their in-house data centre space remains small, standing at just 9%, but un-changed on Q4 2021.

- Similarly, few expect to downsize their externally managed facilities over the next six months – just 3% –once again un-changed on Q4 2021.

- The number of respondents who are undecided on what they will do regarding their in-house estate totalled fell from 5% recorded in our preceding survey to 3% today. For those using third-party solutions, this proportion was higher at 10%, slightly down from 11% six months ago.

- There remains a significant proportion of respondents who believe that there will be “no change” in the amount of their in-house data centre space over the next year, sitting at around 33%, a slight increase on that recorded last time around.

- For those using external third-party providers, the proportion of those who report there will be “no change” of this metric has fallen significantly to 29%, from 38% six months ago.

Fig 12

What are your current expectations for changes to your ‘third party’ technical data centre area?

Drivers of change

- Corporate expansion or contraction has long been established as the most highly ranked factor driving change in both self-owned or managed and third-party data centres over the past decade. This continues in the first half of 2022, albeit the latest survey has seen the proportion identifying it as the top driver falling from two-fifths six months ago to around a third for both internally and externally manged facilities in our latest survey.

- For the second survey in succession, demand for power and the costs associated with it have seen an uplift in the number of respondents citing it as an important driver of changes for both internally and externally operated space – up from 17% previously to 20%. Given the highly publicised inflationary pressures on energy costs that have been experienced over the last year, it may be a little surprising this proportion was not even higher.

Fig 13

What factors are/will be driving these changes?

- Budgetary issues remain a constant for respondents; around 15% cited them as a significant reason for change, in line with that recorded previously.

- The influence of data sovereignty and fiscal structures on data centre footprints has also remained relatively constant at around 13%.

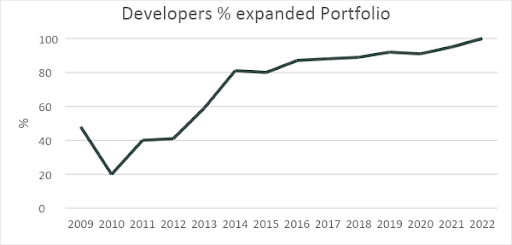

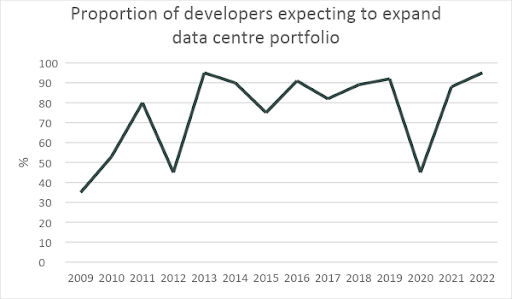

Developers & Investors

No easing in new stock plans

The latest survey suggests an on-going optimism from developers and investors operating in the European technical real estate market. Not only have we recorded a historical high in those reporting expansion over the last 12 months, but also significantly a rise in those expecting expansion over the next 12 months.

Fig 14

- Nearly every developer that responded has reported that they have expanded their data centre real estate over the course of the past 12 months. This is the first time that such near-universal agreement has been reached since we began the survey back in 2009.

- Some 95% of developers and investors also stated that their intention is to expand their portfolio over the coming year, up from around 90% six months ago and now at the highest proportion for at nearly 10 years

Fig 15

The proportion of risk that developer’s feel able to support by way of the amount of space they require to be pre-let before starting a development scheme is one measure that can be used to assess market sentiment. It can be viewed as an indication of the strength of belief in the fundamentals of supply and demand that underpins their decision-making process.

Fig 16

If it is your intention to develop more technical space during the next 12-18 months, on what basis will that be?

- Given this context, analysis of our latest data would suggest a slightly mixed picture. On one hand, we have seen a drop-off in the proportion of respondents that have indicated they would only be prepared to move forward with their scheme if they have the security of a 100% pre-let; from 13% in Q4 2021 to zero.

- On the other, the proportion of respondents requiring at least 50% secured letting has risen significantly over the past six months from around 75% to around 84%.

Another metric to gauge developer sentiment is the minimum lease length requirement for a wholesale transaction that a developer would like to achieve. Here we again see some mixed messages.

Fig 17

For Wholesale transcations, what is the minimum lease length that you would accept?

- Our latest survey indicates that 21% would require over five years term, a rise on the 18% noted six months ago.

- Meanwhile, 21% would accept a period shorter than three years, up from just 6% in Q4 2021,

- Whilst over half (58%) of respondents suggested a three-to-five-year period would be needed, little movement on the 56% who suggested the same six months ago.

Ranking of choice factors for new data centre

- Since we began this survey, the availability of power has consistently been ranked as the single most important factor in the choice for a new data centre. The results of our latest analysis suggest that this firmly remains the case, with over 70% of respondents choosing Availability of Power as their top influencing factor. Indeed, the proportion of those ranking it in either of the top two positions remains at a high of 90%, in line with that recorded in winter 2021.

- Location remains the second most highly rated factor with over two-fifths of all respondents ranking it in either of the top two positions. This degree of importance is unlikely to diminish soon given the background of the continuing global fallout from the pandemic and the ongoing issues with supply chain and the effect that this may have on the location of company’s data centres relative to the markets that they serve.

Fig 18

Drivers Ranking – data centre choice

- It is worth noting that political or social stability has become increasingly more important in recent surveys, a conclusion perhaps not surprising given ongoing concerns about the wider geopolitical environments and most importantly the Russian invasion of Ukraine.

- Access to fibre has risen as an increasingly important factor with around 10% citing it as their most important choice, and nearly half ranking it either of the top two positions. This is the second successive survey that has reported this promotion. As we noted in our last survey, the importance of China – especially Wuhan as a source of optical fibre production capacity - is potentially impacting respondent’s sentiment.

- Factors such as the total build-out cost, availability of specialist data centre construction skills and land price were ranked highly by developers, were consistently rated behind our top factors by the rest of our respondents.

Opinions

Skill shortages - threats to the industry

A threat to the delivery of new technical real estate to meet demand is a lack of sufficiently qualified professionals available to the industry, from design and build staff to operational personnel. How real this threat now, and what consequences might it have on the European market?

Fig 19 A and B

- In our latest survey, respondents continue to express their concerns around availability of skilled labour across the European data centre landscape. When asked about the skills supply/demand balance, 91% of our respondents believe it is characterised by falling supply of skills and rising demand, a significant uplift on the 80% recorded in Q4 2021.

- Overall, the number of those seeing demand either maintained or increasing was at the highest level recorded; some 97%, a marked increase on the 86% recorded six months ago.

- Notably, developer and investor respondents expressed the strongest concerning views, with all respondents from this group suggesting that demand for labour would rise over the next 12 months, allied with a decrease in availability of appropriately skilled staff.

- Most suppliers of data centre services also appear worried about this balance between supply and demand of labour, with the majority of colocation providers carriers/network operators and IT integrators believing the coming year will be characterised by falling supply and rising demand.

- The past six months have seen a significant rise in the level of concern held by corporate respondents - some 88% now expect to see rising demand for skilled professionals in the data centre fields, against a background of dwindling supply. This is a large leap from the 56% expressing the same view six months earlier.

Who’s in short supply?

Fig 20 A

With regard to the design/build/operations of data centres in Europe we believe it is increasingly difficult to source sufficiently skilled design professionals to deliver our current projects

- Over the last six months, we have noted that the number of respondents concerned about potential problems arising from shortages specifically amongst design professionals has remained relatively stable at around 80%, however there has been a pronounced rise in the number of respondents expressing their belief in the strongest terms – up from 31% to 41%.

- At the build stage, the problem appears to be just as acute; nearly 80% of the segmented supply specialists expressed their concerns that a shortage of sufficiently skilled build contractors existed, a proportion which has remained largely unchanged over the past year. Again, we also saw a pronounced shift in the proportion of these expressing their belief in the strongest terms compared to six months previously.

Fig 20 B

It is increasingly difficult to source sufficiently skilled build professionals to deliver our current projects

- Whilst according to our respondents, the difficulties in sourcing operational staff are slightly less pronounced than at the design and build stages, at 75% this still represents significant concern. We also see the proportion who strongly agree rising significantly to nearly 45%.

- The strength of agreement does vary amongst the groupings, albeit not as pronounced as in other categories. Our DEC respondents expressed their concern over skills shortages in the most robust terms, with universal agreement that shortages exist at both the design and build stages. In contrast just 72% of theses respondents see skill shortages amongst operational personnel.

- The strength of belief in design and build skill shortages amongst our service providers is slightly less pronounced, around 80% of these respondents agreed that shortages are problematic.

- A significant proportion of our corporate respondents (84%) agree that shortages of skilled operational staff pose the biggest problem, compared with 50% of our design professionals and 23% for build professionals.

Fig 20C

It is increasingly difficult to source skilled operations professionals to deliver our current projects

- Amongst our respondents, there appears to be consensus regarding job shortage concerns. Indeed, most respondents identified multiple roles as areas of concern rather than singling out just one discipline.

- In the construction sector over half of respondents stated that they had experienced shortages of quantity surveyors, site managers and site engineers within the past year.

- On the operational side, nearly 70% of respondents stated that they have had direct experience of shortages amongst operations and network engineers/technicians over the last 12 months, with a slightly lower proportion – around two-thirds - seeing a shortage of infrastructure specialists over that period.

- Also worthy of note, Mechanical & Electrical project managers were highlighted as an area of concern by 70% of respondents.

Skill shortages impact

- The wider debate over skill shortages is set within the context of its impact on the delivery of suitable stock for the end users. There appears to be little doubt that these shortages have already had real consequences and directly impacted on our respondents.

- Notably, when questioned about impacts experienced due to shortages in skilled professionals over the past year, most respondents cited multiple factors.

- The most cited impact is that a greater workload has been placed on existing staff, nearly nine-out-of-ten cited this as the case, an uplift from the eight-out-of-ten recorded six months ago.

- The shortage of staff has inevitably led to increasing operating/labour costs recorded by 83%, although it is noted this is a marginal decline from the 86% recorded six months earlier. These shortages can be seen as a contributory factor in the increasingly popularity of the use of outsourcing options, with around 51% citing this.

Fig 21

In the past year we have experienced the following as a direct result of skill shortages

- It appears that more respondents are finding it difficult to resource existing work this year than was the case in 2021, with just over half stating that they had experienced difficulties in meeting deadlines or client objectives. This is a rise on the 39% recorded six months ago, although notably lower than the 70% who cited it as factor at the beginning of the pandemic in 2020.

- In addition, just over two-fifths stated that shortages had led to delays to developing new products/innovations, up from the quarter recording this in our last survey, whilst the proportion that noted they had ceased offering certain products or services has also risen to 14% from 9%.

- However, lost orders is one of the more extreme consequence of skills shortages, and in our latest survey just 8% believed this had happened, a quite significant fall on the 20% identified six months ago.

Supply chain

- Disruptions to global supply chains continue to plague the data centre industry – 87% of our respondents stated that they had experienced such an eventuality in the past year, a marginal decline on the 91% recorded in our preceding survey, but a concerningly high proportion, nevertheless.

Fig 22

We have experienced considerable supply chain volatility over the past year

- Disruptions were felt the hardest amongst our build professional respondents who reported experiencing supply chain volatility over the period with some 93% of our design engineering and construction (DEC) group expressing their assent in the strongest terms whilst 63% of developer/investor respondents reported the same.

- Amongst our service providers, there is also near unanimity regarding this disruption – 98% experienced such supply chain problems.

Fig 23

Regarding the base construction of our data centre(s) in Europe, we have experienced the following:

The fallout from the global pandemic and related geopolitical issues continues to cause some robust challenges especially to the construction sector. However, we can note some indications of an easing in the degree of challenge being faced; the sourcing of construction raw materials for example.

- For our respondents, just over half in 2021 experienced sourcing difficulties for concrete/cement, steel, cladding materials, and dry lining materials – a proportion that has fallen to around 32% in 2022 for the concrete /cement and two-fifths for the other materials.

- However, there remains some physical shortages of materials which according to our respondents has led to a rise in associated costs – raw material unit and transportation costs as well as construction labour costs have all reportedly risen according to around three-quarters of respondents.

- On a sectoral basis, amongst our DEC respondents, over four-fifths have experienced raw material unit and transportation cost rises as well as construction labour costs in both 2021 and the early part of 2022. Even more telling is that the majority of developer’s/investors cited rising costs across the same metrics in both years.

Supply chain disruption impacting future data centre locations

Fig 24

Potential long term supply chain problems will impact significantly on our decision making regarding the future location(s) of our data centre(s)

- We have already noted earlier in the survey that location is second only to availability of power in a list of contributory drivers in identifying a new data centre for our respondents.

- Ongoing supply chain problems are likely to impact on the decision-making process according to our respondents, with just over 60% believing that long term disruption could have a major impact regarding the siting of future data centres.

- There is a broad range of opinions amongst different groups of respondents. Our DEC respondents were the most fervent in level of agreement with some 85% expressing their agreement (71% in the strongest possible terms) whilst 64% of service providers agreed.

- End user respondents expressed both the lowest level of agreement – just 44% and the highest level of disagreement – at 21%.

Power – The ongoing challenge

Whilst the growing global demand for IT services presents major opportunities for the data centre industry, it also presents a significant challenge – the need to source a sufficiency of power required to meet this ongoing expansion. This must be achieved against a background of environmental commitments to ensure clean and renewable energy use across data centre estates, driving down the carbon footprint of the industry.

- Our latest survey suggests that demand for power will continue to grow. Around 84% of respondents reported that they expect their power consumption levels to rise over the next three years, a rise from 76% recorded in Q4 2021 and 73% a year ago.

- Amongst our service providers this proportion is even higher at some 93%, whilst 73% of end users expect power consumption levels to rise over the next 3 years.

Fig 25

Over the next three years, we expect our power per sq meter consumption to:

Average Rack Power/cooling levels to rise?

- Over a quarter of respondents expect to see an average rack power/cooling level of 6kw-9kw over the coming 12 months - little change on the proportion recorded six months ago. A further 27% foresee a 9kw-12kw average power level over the period, up on the 22% who reported the same level six months ago.

- Once again only a relatively small proportion of our respondents (4%) indicated that they would see a level higher than 15 kw per rack – marginally above the 3% who reported the same in Q4 2021.

Fig 26

What is your expectations for your average rack power /cooling level by the end of the year

- Amongst our corporate respondents, around 30% are expecting to see an average rack power/cooling level of 3kw-6kw by the end of next year whilst a further 39% suggest their average levels will be in the 6kw-9kw range, up from the 31% who expected the same in our last survey.

Power efficiency increasingly attractive driver

- The rising costs of power are likely to benefit more energy efficient data centres moving forward according to over four-fifths of our respondents, with at least half of all respondents strongly agreeing with this view.

- Amongst our service providers this proportion is even higher at some 96%. In contrast just 44% of end users expect this to be the case.

Fig 27

We expect a rise in the cost of power in Europe to increase the demand for power efficient data centre space over the next three years

Move to renewables

- There is little doubt that many of our respondents have a commitment to ensure their data centre power is sourced from renewable resources. We have seen the proportion of respondents agreeing that this would be the case reaching 84% in our latest survey; a rise on the 79% six months earlier. Once again, amongst our service providers this portion jumps to some 93%.

Fig 28

We expect that the sourcing of power for our data centre in 2031 will be 90% or more sourced from renewable sources

As a European wide survey, our respondents operate across multiple countries with different infrastructures for sources of power delivered over their respective national grids. As is to be expected, European nations have a variety of diverse policies driven by numerous and complex geopolitical factors that have dictated the history of power resourcing and are changing the future landscape. For example, Germany, the sixth largest consumer of energy in the world and the largest national market of electricity in Europe, has reduced its reliance on coal power substantially in recent years. In 2013, coal made up about 45% of the country’s electricity production down to around 24% in 2020. In addition, the country has an ongoing plan to shut down its nuclear power plants. At time of writing three nuclear power plants remain active — down from 17 in 2011 — and the remaining three are scheduled for decommissioning at the end of this year. To replace these resources, Germany has had an active policy to promote various renewable energy generation initiatives and the government has set the goal of meeting 80% of the country's energy demands from alternative energy by 2050.

In contrast, in France the approach to nuclear power is very different to its neighbour, as it is responsible for some 70% of total electricity production. Meanwhile, in Spain wind power overtook nuclear power as the leading source of electricity, and in Denmark, bioenergy (energy stored in organic material or biomass) has recently overtaken wind energy as the most widely used renewable energy source.

The recent invasion of Ukraine and subsequent economic sanctions against Russia has undoubtedly helped to accelerate the focus on renewable sources across Europe. In 2021 Russia was the largest exporter of oil and natural gas to the European Union, accounting for about a quarter of the oil EU countries import and 40% of natural gas consumed.

The disparate nature of sources of power across Europe is an important factor in explaining why only around one-in-ten of our responders secured their energy from a single source. As we noted six months ago, those who source energy solely from finite resources such as gas and coal, total less than 5% of our respondents.

Fig 29

Current Power sources

Around 27% of our respondents’ data centre portfolio is powered only from a mix of renewable sources including solar, hydroelectric/tidal and wind farms/turbines, an encouraging increase from 21% recorded in our last survey. Nuclear power was used in a least part of their portfolio by around 25%, down from the 30% recorded last survey.

The direction of travel in terms of utilisation off gas or coal power in our respondents’ facilities is encouraging - around 45% of our respondents utilise some degree of gas or coal power in their facilities, down from 48% six months ago and 53% a year ago. This proportion declines to around 28% over the next five-year period. In addition, nuclear power is expected to remain as a source of power by around 29% of respondents on at least part of their portfolio in five years’ time.

There has been almost universal agreement amongst our survey participants that they expect to see a rise in the proportion of power used from renewable sources which will service their data centre facilities. In our last two surveys we noted that 7% of respondents indicated that their facilities will be sourced from a single type of renewable power, and in our latest analysis this proportion is approximately the same at 8%.

Fig 30

Future Power sources

Can the industry be trusted to self-regulate?

Climate change and the global response of Net Zero has dominated the political discourse in recent years. There appears to be widespread agreement within the data centre industry – as a major and growing consumer of power – that it has an important role to play in the debate and resulting actions to implement change to limit and ultimately reverse the damage caused by historical methods of power generation.

As our survey results have already noted, there is a firm commitment on behalf of our respondents to move towards a renewable-sourced future. Nevertheless, the direction of travel in the political realm suggests that regulation could be placed on the industry to push initiatives for the greater use of renewable sources of power at a more rapid rate. Certainly, our respondents hold a strong belief that that is the case, with around 90% indicating that increased levels of regulation could be introduced to ensure greater compliance. Amongst service providers, this proportion is slightly higher at 96% for colocation operators and 93% for carriers and real estate developers and investors. End-users are less certain with around two thirds agreeing and the other third remaining neutral.

Fig 31

Increasing socio-political pressures and Net Zero requirements are likely to lead to increased regulation on the European datacentre industry to ensure greater compliance

Should the industry self-regulate?

The issue of regulation is always difficult. There is of course a need for industries to operate within a regulatory framework to ensure standards on many aspects. However, the extent of that regulation lies at the very heart of the fundamental debate of state intervention in the private sector and its implications for how business operates. There is a real and practical debate to be had, and in the real world there are industry groups to influence policy makes and legislators to ensure positive outcomes without stifling industry growth. Sensible policy makers accept and welcome this knowledge as it provides – accepting a degree of self-interest – knowledge, experience, and expertise on an issue from those with the greatest exposure to it.

In turn those reputable business accepts the need to operate their business within a sensible regulatory framework as it provides a stable and secure environment and gives their customers confidence around industry standards. The argument around self-regulation is to what extent processes within the industry need to guide and frame within a legal process and how much can be voluntarily supported and provided.

For the data centre industry here is little doubt that the industry recognizes the need to move forward with power optimisation and sensible sourcing initiatives. There are several high-profile groups and initiatives already in operation including the voluntary European Code of Conduct for Energy Efficiency in Data Centres and the Climate Neutral Data Centre Pact for example. The argument here is that those within the industry - and whose bottom lines it will directly impact - are best placed to know how to innovate and produce solutions. Around three-quarters of all respondents believe that self-regulation offers the best course of action to aid the push to meet Net Zero targets. Around 94% of developers and investors, and 85% of service providers indicated this view.

Fig 32

Self-regulation by the European data centre industry is the best course of action moving forward to help reach Net Zero requirements.

Use of waste energy

One element that is increasingly debated is that of the use of waste heat energy generated by data centres. In Europe, Norway is perhaps the furthest down the line in terms of formal requirements for heat reuse by data centres. The requirements here still rather limited, however, with the measure introduced in 2021 still only being a requirement that all data centres must examine the possibility and report on it.

Despite this rather limited exposure it seems that our respondents expect the political landscape within the context of the climate change debate is likely to require further adoption of such initiatives. In our latest survey, 86% of respondents expect further regulation over the next 5 years to drive the adoption of waste energy programmes in data centres.

Fig 33

Over the next 5 years we expect to see increased regulatory requirement and government (local and national) intervention to drive the adoption of waste energy programmes in data centres

At present, question marks exist over the efficiencies of power generated in this way. This uncertainty over the economic viability of such programmes causes concern amongst respondents, with some 83% suggesting that the economic metrics of such programmes needs to improve greatly for them to consider such measures over the course of the next five years.

Fig 34

Over the next 5 years, the economic viability of waste energy programmes needs to improve greatly in order for us to consider

One of the major reservations around adoption of these systems is the belief that

waste heat utilisation is only an economically viable option for data centres that are already in close proximity to existing district heating systems, with 59% of respondents indicating this.

Fig 35

Waste heat utilisation is only an economically viable option for data centres that are close to existing district heating systems.

Further doubts emerge around the issue of the imitations that waste energy source has, given its maximum permitted uptime at around 98% and its suitability as a primary power source, with three-quarters indicating this. Almost four-fifths of service providers believe that to be the case – a proportion which rises to above 90% in the case of integrators. However, around 60% believe that waste to energy sources could be considered as a secondary power source.

Fig 36

Current limitations to maximum permitted uptimes – at around 98% – mean that waste to energy sources is not a current viable option for us as a primary power source

Fig 37

Current limitations to maximum permitted uptimes – at around 98% – mean that waste to energy sources could be considered as a secondary power source to add resilience

Retro-fit solutions

As the need to move towards Net Zero targets becomes more urgent, one option that may prove to be attractive is to adapt existing data centre facilities to enable them to adopt or enhance renewable energy power sources. Overall, two-thirds of our respondents agree that retrofitting exiting facilities is something that they would be prepared to consider. This is particularly supported by carriers and integrators (90%), managed service providers (86%) and DEC (82%) respondents.

Fig 38

We would actively look to retrofit energy production solutions (i.e. solar, turbines, waste-to-energy) at our data centres to accelerate the move towards our Net Zero requirements.