es

es de

de it

itContents

Click to go to key areas of report

- Executive Summary

- Introduction

- Ownership and Management

- Utilisation

- Developers and Investors

- Skill shortages - the threat remains

- Power

- Consumption on the rise

- Average Rack Power/cooling levels slowly rising

- Rising power cost to drive efficiencies

- Move to renewables

- Supply chain disruption continuing

- Supply chain disruption impacting future data centre locations

- Inflationary impact - will clients pay?

- Legacy data centres

Opportunity or Liability – Legacy Data Centres

To view a PDF of the report click here

Executive Summary

In the rapidly evolving landscape of information technology, legacy data centres are increasingly facing a plethora of challenges that hinder their ability to meet modern demands. This report highlights the multifaceted issues confronting these traditional data centres, illuminating the complexities that organisations must navigate to remain competitive and efficient in today's digital era.

According to the IDC, the average data centre is 9 years old. However, Gartner states that any site more than 7 years old is obsolete. Legacy data centres, typically characterised by their aging infrastructure and outdated technologies, were designed during a period when current technological advancements were not anticipated. These facilities now struggle to cope with the escalating requirements of modern computing, such as higher data volumes, faster processing speeds, and the need for robust cybersecurity measures. One of the primary challenges is the perception of limited scalability of legacy data centres. Initially built for a different era of computing, they often lack the physical and architectural flexibility to adapt to the rapid pace of technological change. This perception results in difficulties in integrating new technologies, leading to operational inefficiencies and increased costs. As businesses grow and their data needs expand, these data centres often struggle to scale up effectively, leading to performance bottlenecks and reduced competitiveness. However, in some cases we are seeing capacity expansion opportunities which are being missed. Another significant challenge is energy inefficiency. Older data centres were not designed with energy conservation in mind, leading to excessive power consumption and higher operational costs. This is not only financially burdensome but also environmentally unsustainable. With the growing emphasis on green computing and corporate responsibility, organisations are under pressure to upgrade their facilities to be more energy-efficient.

Furthermore, legacy data centres are grappling with inadequate disaster recovery and data backup systems. In an age where data is a critical asset, the inability to ensure data integrity and continuity in the face of disruptions poses a significant risk. These centres often lack the advanced infrastructure and protocols necessary to protect against data loss or breaches, which can have catastrophic consequences for businesses. Addressing the challenges of embedded carbon in legacy data centres is critical in the context of global efforts to reduce greenhouse gas emissions and combat climate change. Legacy data centres were built at a time when less attention was paid to the environmental impact of construction materials and methods. The embedded carbon in these structures includes the emissions from the extraction, manufacturing, and transportation of building materials. The issue on embedded carbon is to the carbon that has already been emitted during initial construction when contemplating modernisation such that it isn’t in a sense wasted. Modernising or replacing these facilities to reduce their carbon footprint can be complex and costly. Moreover, the maintenance of legacy data centres presents a considerable challenge. The aging hardware and software require frequent and costly upgrades and repairs. This not only strains financial resources but also demands specialised skills that ar becoming scarce in the IT workforce.

Finally, compliance and regulatory challenges add another layer of complexity. As governments and industries impose stricter regulations on data privacy and security, legacy data centres often struggle to meet these evolving standards, leading to potential legal and financial penalties.

In conclusion, legacy data centres are at a critical juncture where they must overcome a myriad of challenges to stay relevant in the digital age. At BCS we have helped many clients navigate potential pathways for transformation and innovation to deliver the best possible outcomes to modernise their digital built assets. We have helped clients figure out whether a given site warrants a closer look for investment by undertaking high level modelling, saving time and money in studies that may prove a site unsuitable for expansion / de-carbonisation / continued maintenance and operation.

Introduction

Welcome to our latest data centre survey – the 27th edition conducted by iX Consulting, an independent research firm specializing in data centre economic analysis, and sponsored by BCS, a leading provider of integrated IT asset consultancy solutions.

The survey work was undertaken in late September and early October, a period that was characterised by cautious yet optimistic economic growth forecasts across Europe albeit set against a background of geopolitical difficulties including the continuing war in Ukraine and then the start of the armed conflict between Israel and Hamas-led Palestinian militant groups which now sees Israel mounting a full-scale military assault in Gaza.

Against this background, our survey aims to gauge both the current and ongoing prospects for the data centre industry across Europe. As we noted in the summer, the industry may face challenges associated with broader global factors, such as supply chain disruptions and raw material inflation, however it also continues to see growth through sustained demand for technology-driven services. Evidence suggests that the past six months has seen little change in this characterisation and our most recent survey will explore the continued response of the industry to such conditions and identify any emerging trends or opportunities that arise as a result.

Fig 1

What is your primary relationship with the data centre industry?

Our respondents represent a comprehensive and varied group of organizations involved in real estate, investment, colocation, telecom, IT and managed service industries throughout Europe. These stakeholders include service providers, developers, financiers and corporate occupiers who own or manage data centre portfolios comprising approximately six million square meters of technical floorspace based in 40 countries across Europe.

Fig 2

Total Technical Floorspace

Fig 3

The Supply/Demand dynamic

- The European data centre market continues to demonstrate its robustness, with our latest survey indicating a confidence in the trend of decreasing supply and increasing demand. This sentiment is shared by 91% of survey participants, representing a slight increase from the 89% recorded in the summer of 2023.

- For the fourth survey in a row there is universal agreement amongst respondents that demand will either increase or remain the same over the coming year.

- For the seventh successive survey, all developer and investor respondents expect a continuation of rising demand over the next year, again cementing this group’s position as showing the most bullish group market sentiment.

- Most suppliers of data centre services continue to hold generally buoyant views regarding the balance between supply and demand in the market. For the second survey in succession all our colocation providers indicate rising demand.

- In addition, carriers/network operators and IT integrators illustrate their ongoing confidence, with some 97% expressing an opinion that the coming year will continue to see falling supply and rising demand; albeit a small decline on the universal agreement we recorded in the summer.

- For the second survey in a row, we have seen a marked uplift in the proportion of corporate respondents that expect demand to rise over the coming year. At 90%, this is a rise from the 74% recorded six months ago, and up from the 60% seen in our Winter 2022 report.

Fig 4

Ownership and Management

Since our survey work began some 14 years ago, we have noted an on-going preference for our colocation operators and IT integrators/web hosting participants to manage most of their own facilities, with over three-quarters now recording that 80% or more of their data centre portfolio was internally managed. This proportion has remained almost constant over the course of our survey work reflecting an emphasis for control of their own space, allowing them to respond quickly to client demand, as well as providing their clients with an added-value proposition.

In contrast, we have seen end-user respondents become increasingly drawn away from reliance on self-managed IT infrastructure towards relying on third-party solutions. For the third survey in a row, four-fifths of corporate participants have indicated that they rely on a third-party to manage at least 80% or more of their data centre portfolio, reflecting an up-tick from around 50% who recorded this a decade ago.

This increased popularity in the use of third-party solutions amongst end-users has been driven by several factors. Data centre construction can be expensive requiring a large initial expenditure which has proven to be a barrier to end-users. For those market participants whose business is the provision of new technical space and solutions, the ability to benefit from the latest technology and economics of scale associated with such builds mean that they are likely to be able to deliver new stock in a more cost-efficient manner than available to an end-user.

It is also seen that many respondents favour a mixed approach to their data centre requirements. By adopting this hybrid strategy, end-users benefit from a combination of the advantages of both solutions; a higher level of control over specific aspects of their infrastructure, with the flexibility and scalability of an out-sourced solution.

Utilisation

Value for money and cost-efficiency drives have become the focus of most industries across the globe. The effects of severe supply chain difficulties that started during the pandemic and have been further exacerbated by other geopolitical issues such as Russia’s invasion of Ukraine, have been felt throughout Europe leading to inflationary environments experienced across the board. The global supply chains that are involved in all aspects of the development and occupation of the European data centre market mean that the industry has been particularly exposed to these inflationary effects.

Therefore, whilst the occupational side of the data centre market has always been characterised by a desire to maximise utilisation of infrastructure whilst maintaining flexibility for growth, it has become even more into focus over recent surveys, for both service providers and corporate users.

The average utilisation rates of third-party managed space continue to exceed those for internally managed solutions. In our summer edition, 83% of respondents reported that they utilised over 80% of their outsourced technical footprint, compared to 36% who utilised the same percentage of in-house managed facilities. Our latest research suggests a continuation of this, with the outsourced managed space proportion remaining high at 81%, whilst in-house utilisation rates now rising to 52%.

This requirement to maximise efficiencies in third-party data centres is mirrored by our end-users, with 83% reporting 80% or more utilisation of their third-party space, and 50% utilisation rates for their in-house managed facilities.

Fig 5

How much of your current data centre space is active and being used?

In contrast, average utilisation rates for service providers tend to be marginally lower with just over half of their own facilities reaching utilisation rates of 80% or more, reflecting the need to balance the commissioning of space to meet expected demand and having near-finished space to allow quick deployment when needed. As with other users, service providers are driven by a need to maximise value for money regarding their third-party controlled space, maintaining relatively high utilisation rates with four-fifths utilising at least 80% in these facilities.

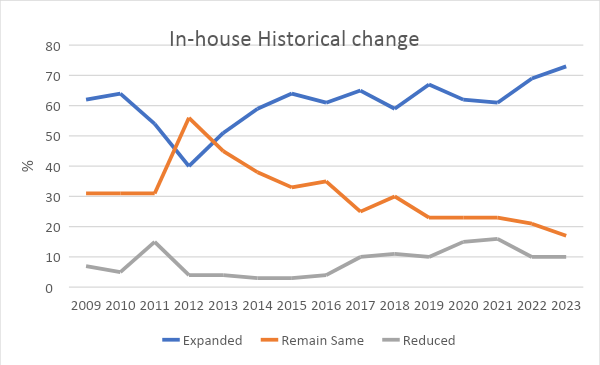

Expansion on-going

The ongoing expectation amongst respondents therefore appears to be positive that demand for IT services is set to continue. The profile of reported changes to in-house managed data centre capacity has altered little over the 12 months. In our last summer survey, we saw around three-quarters of respondents suggesting that they had increased their in-house managed data centre capacity in the preceding six-month period; a proportion un-changed in our winter survey. Those participants indicating no change remained at 10%, whilst those having reduced their in-house floorspace has also stayed at around 17%.

An examination of third-party expansion patterns over the past six months also points to continued healthy expectations of demand for data centre services, with some 83% of respondents suggesting an expectation to increase in their externally managed solutions over that period. This represents a rise on the 79% recorded earlier in the summer and considerably above the long-term average of 55%. In addition, around 12% reported no change in their third-party portfolio and only 6% reported a floorspace reduction.

Fig 6

How has your total fitted technical floorspace altered over the past six months?

Fig 7

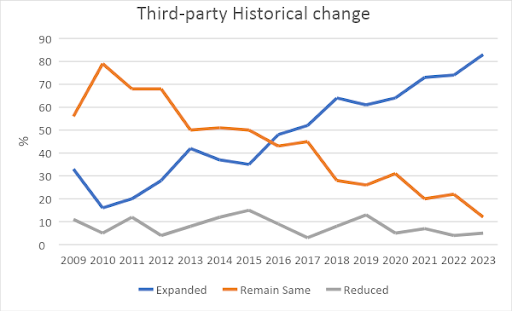

For service providers the aim is to be able to provide the supply that their clients require in a timely manner. The latest survey provides further evidence of continued healthy rates of demand for this supply and these services. A familiar profile can be seen amongst the different respondent professions. Around 95% of service providers recorded an expansion in their own stock over the period, with similar levels amongst managed service providers, telecom specialist and colocation suppliers. Notably, the proportion of colocation suppliers indicating an increase has risen significantly from the two-thirds who reported the same measure back in the summer.

In our summer 2023 survey we found that the number of corporates who indicated that they had increased their in-house technical floorspace over the previous six months had doubled since the previous survey: a jump from 6% to 12%. Our latest research shows that this proportion has risen again to 14%. At the same time, we have seen a small fall in the number of end users reporting that they had reduced their in-house stock; from 59% to around 52%. This seems to suggest a slight reversal of the trend for end-users to continue to expand their portfolios with third parties at a cost to their in-house managed space and may reflect the more challenging economic period that has been experienced since the start of Covid, perhaps persuading end-users to bring IT environments under their own immediate cost control.

Whether this will continue is yet to be seen, however it is apparent that a blended approach is becoming more popular, allowing users to keep some infrastructure under in-house management whilst gaining the benefits from outsourcing other elements of their IT estate to trusted third parties. Indeed, some 83% of end users also reported an increase in their third-party managed data centres over the past six months, still a very healthy majority, albeit a marginal reduction on the 84% reported in the summer.

Fig 8

Amongst our service providers some 86% indicated a rise in the number of third-party managed data centre expansions over the period, up from the three-quarters reported in our last survey.

Fig 9

Corporate Sector – data centre proportion expansion

How was expansion achieved?

The self-build option remains the most approved choice amongst our respondents in terms of expansion within self-managed facilities over the past six months, some 47% of respondents outlined this approach, similar to the 49% reporting the same in our last survey. The option of purchasing or leasing through a development partner was highlighted by around two-fifths of respondents, an increase on the one-third recorded six months ago.

Fig 10A

If change has occurred via expansion or contraction how have you achieved this? In house

In addition, 13% reported that they have reduced their technical floorspace by decommissioning one or more legacy facilities, little change on the number seen in the preceding two surveys, and once again the vast majority of these being corporate end-users. The choice to utilise a colocation provider remains a firm favourite amongst our respondents; some 74% saying that they had chosen this route, a rise on the two-thirds recorded in summer.

Also of note is the fact that some 14% of respondents selected more than one route to meet their externally managed solution needs. In such cases, this may be due to the availability of product, pricing, and geography. Moreover, it most likely also reflects the changes in demand requirements for contracting space with an outsourced facility tailored to meet the diverse needs of each enterprise in terms of access to power, certain IT eco-systems or networks, or simply down to geographic necessities.

Fig 10B

If change has occurred via expansion or contraction how have you achieved this? Third party

No slowdown in expansion plans

When questioned on anticipated changes to their self-managed technical floor space, 64% of respondents expect to see an expansion in the coming year, a proportion unchanged since our last survey. As we have recorded previously, service-provider respondents have been the most confident – some 84% broadly in line with the 85% who reported the same six months ago. The proportion of participants indicating they would reduce their in-house data centre space remains small – at just 10%, although this is marginally up on the 8% noted in the summer.

The share of those participants who believe that there will be “no change” in the amount of their in-house data centre space over the next year has remained static since our last research at 24%, whilst those respondents who are undecided has remained low at 3%.

Fig 11

What are your current expectations for changes to your ‘in-house’ technical data centre area?

The contrast in views on the issue of in-house data centre change amongst corporates compared to our other groups of participants remains marked. The desire to expand facilities remains low with just 16% of end users intending to expand self-managed facilities over the next year contrasted to the 84% of service providers. In addition, around 46% of corporate participants said they expected to downsize their in-house facilities during the period, an increase from 40% reported in the summer, whilst nearly a third indicated that they would choose to retain floorspace at the same level, a fall from around half in the summer.

Expectations for third-party data centre facilities appear positive over the coming 12 months, with two-thirds of respondents reporting their intention to expand over that period, up from the 61% recorded in the preceding survey. Those who reported there will be no change in their third-party estate has fallen from 31% to 24% in the six months between surveys, whilst the number of respondents who are undecided has risen from 4% to 8%. In contrast, the proportion of those who expect to downsize their externally managed facilities over the period remains unchanged at just 3%.

On a sectoral basis, our latest research has also seen a marked increase in the proportion of service providers who expressed intentions to expand their third-party managed data centre space over the period, up from 54% to 68%. In addition, 83% of end users indicated they would expand operations with a third-party provider, up from 79%.

Fig 12

What are your current expectations for changes to your ‘third party’ technical data centre area?

Drivers of change

Since our first survey in 2009, corporate expansion or contraction has been established as the most highly ranked factor driving change in both in-house and third-party data centres. This continues in our latest survey with approximately a third of participants citing it as the top driver for changes in both in-house and third-party floorspace.

Fig 13

What factors are/will be driving these changes?

Demand for power and the costs associated with it has remined firmly in second place; the number of respondents citing it as an important driver of change to both in-house and third-party operated space holding at 18%. Budgetary issues are once again ranked in third place, although we have seen a slight rise in those citing it, from 15% last summer to around 17% this time around.

The ranking of availability of appropriate data centre product by around 13% of respondents remains similar to the 14% reported previously, however there is significantly greater importance attached to this factor in regards of third-party data centres – some 19% contrasted to just 7% who cited it in respect of in-house solutions. Data sovereignty and fiscal structures remain relatively unchanged in respondents’ views compared to our summer research. Data sovereignty identified by 10% of participants and fiscal structures cited by 9%.

Developers and Investors

No easing in new supply plans

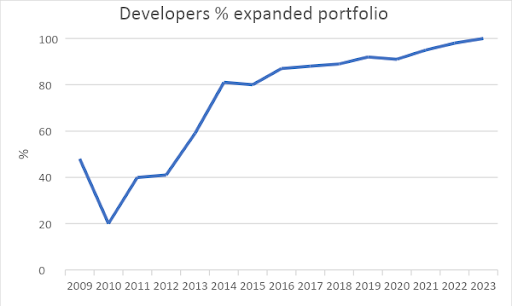

The provision of new data centre supply to satisfy future levels of demand is a key component to ensure a well-balanced market across Europe. Our latest survey continues to provide evidence of the on-going confidence in the European market, with all developer and investor respondents reporting an expansion in their portfolio of technical real estate in the past six months. This is the fourth consecutive survey in which we have recorded this near-universal level of sentiment amongst this group.

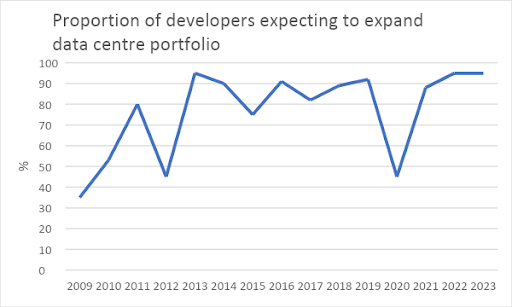

In addition, there appears to be little sign of any potential slowdown in the supply pipeline soon. For the fourth successive survey some 95% of developers and investors revealed that they are anticipating expanding their portfolio over the coming year.

Fig 14

It is worth noting again that this progress occurs against a backdrop of some very challenging economic circumstances that show little evidence of subsiding soon. The inflationary environment that engulfs one of the key components of data centre charges – electricity – appears now to be clearly baked into occupational costs and can only be met by end-user price increases. Despite previous assumptions that these inflationary pressures may relax as supply side pressures are resolved, developing geopolitical issues may well keep these prices higher than anticipated for the foreseeable future.

Fig 15

One measure that can be used to assess developer’s market sentiment is through the proportion of risk that they feel able to support by way of the amount of space they require to be pre-let before starting a development scheme. Whilst there are several factors that feed into these criteria (for example, company finance structures) this helps provide an indication of the levels of sentiment that underpins their decision-making process.

Fig 16

If it is your intention to develop more technical space during the next 12-18 months, on what basis will that be?

Analysis of our latest data suggests a slight lowering in the level of caution exhibited by developers bringing new schemes to market, as we have seen a slight fall in the degree of pre-letting required. The number of respondents requiring at least 75% or more of their scheme to be pre-committed has fallen from 18% to some 10% in our latest research, the third successive survey we have noted a decline.

Counter to this, however, it should be acknowledged that we see indications in a slight decline in the proportion of those who are prepared to start a build-out having secured a pre-lease on just 25% or less. This quantity has fallen from 22% six months ago and now stands at 19%.

Fig 17

For Wholesale transactions, what is the minimum lease length that you would accept?

One other area of interest is the minimum lease length for a wholesale transaction that the developer would prefer to achieve. Our latest survey indicates that almost half (48%) of respondents suggested a three-to-five-year period would be needed, a fall on the two-thirds indicating the same six months ago. In addition, 29% would require over five years (13% in the summer) and just 23% would accept a period shorter than three years; no change in the last six months.

Ranking of choice factors for new data centre

Once again latest analysis illustrates that the availability of power has been ranked as the single most important factor in the choice for a new data centre, a continuance of sentiment that stretches back to our first data centre survey in 2009. Most recently, 74% of respondents choose it as their top influencing factor, and indeed, the proportion of those ranking it in either of the top two positions remains high at 95%, a rise from 80% recorded in our preceding survey.

Location remains the second most highly rated factor with almost two-thirds of all respondents ranking it in either of the top two positions, up from two-fifths recorded previously. Since the pandemic we have noted a marked uptick in the importance attributed to location by our respondents and likely to remain so given current global geopolitical incertitude continues to remain at the forefront of economic uncertainty.

In our last survey we found that the availability of specialist data centre construction skills has become a more popular factor cited by around 20% of our respondents as one of the top two ranked factors. That portion is largely maintained in the latest research. Amongst those supply-side providers - developer, investor, and Design, Engineering, and Construction (DEC) businesses - this is rated more highly, with around one-third ranking it in their top two factors. Land price and total build out costs similarly score more highly amongst these groups.

Fig 18

Drivers Ranking – data centre choice

Whilst the last couple of surveys has seen access to fibre rise as an increasingly important factor, the latest survey provides evidence of a reversal in this trend. Just 22% cite it as one of their top two factors, almost half that recorded in the summer. As we noted in earlier surveys, the importance of China – especially Wuhan as a source of optical fibre production capacity - potentially drove concerns around access to fibre. These issues remain, and therefore it may be surprising to see a drop-off in respondent’s concerns, perhaps explained more easily by their rising concerns in other issues pushing fibre down the list.

Skill shortages - the threat remains

An ongoing area of concern within the data centre industry is the lack of sufficiently qualified professionals to meet demand, particularly across the design, build and operations disciplines. Our research during the past eight years has tracked this area closely and sought to gauge market practitioners concerns and the resulting effects on delivery of space to the market.

Fig 19 A and B

- Shortages of skilled labour across the data centre industry are marked according to our respondents, and our latest survey provides no evidence in any decline in the level of anxiety felt. Six months ago, we reported that some 98% believed that the coming year will see a decline in supply of staff, and this proportion remains unchanged.

- Some 93% also believe that this will be accompanied by a rise in demand for staff with these skill sets, again remaining unchanged since our last survey in the summer.

- Our developer respondents continue to show strong concerns that the coming year will be characterised by the double issue of significantly falling supply of staff AND demand for those skill sets rising - at 96% this represents the highest degree of assent amongst all our respondent’s groupings.

- Whilst amongst our DEC respondents’ concerns remain high, there has been a slight decline in the number whose level of concern is ranked at the highest level; from 93% in the summer to 84% most recently.

- In our last survey we noted that data centre suppliers appeared increasingly worried about this balance between supply and demand of labour; most colocation providers carriers/network operators and IT integrators believing the coming year will be characterised by falling supply and rising demand. At that time 46% expressed their concern in the strongest possible terms, a proportion that has most recently risen to 53%.

- Amongst corporates, the level of concern has also increased: some 90% believe that a rising demand of skilled staff would be met with falling supply, a rise from 84% recorded previously.

Who’s in short supply?

Fig 20 A

It is increasingly difficult to source sufficiently skilled design professionals to deliver our current projects

The past six months have seen little easing in the level of concern expressed by our respondents regarding shortages of suitably qualified design professionals. As was the case in the summer, some four-fifths of respondents expressed their agreement that sourcing such labour was becoming increasingly difficult. Indeed, this portion has remained consistently at or near these levels for the last four years.

Fig 20 B

It is increasingly difficult to source sufficiently skilled build professionals to deliver our current projects

A similar level of concern is expressed by our survey respondents about skilled professionals across the build sector. Some 79% indicated their concerns that a shortage of sufficiently skilled build contractors existed - a marginal fall from the 81% reporting on the same metric six months ago, and the second successive survey we have noted a fractional decline, as a year ago the proportion stood at 83%.

The third element of the process – the supply of sufficiently qualified staff to service the operational side of data centres – also faces difficulties. Whilst our latest research suggests this may have seen a slight reduction in concern compared to the design and build stage as we noted in our last survey, there remains 76% who expressed their agreement, unchanged on that recorded in the summer.

Fig 20 C

It is increasingly difficult to source skilled operations professionals to deliver our current projects

Unsurprising amongst our respondents’ groups it is those whose role is to deliver new supply to the market that have expressed the highest levels of concern regarding the supply of skilled professionals in the design and build process. Amongst our developers, there is universal agreement that they are encountering challenges in finding skilled professionals, remaining at the high levels recorded a year ago. 93% of DEC respondents acknowledge concern over design professional shortages and, as with developers, there was universal agreement on build professional shortages.

As we noted in our summer survey, for service providers the strength of belief in design and build skill shortages remains less pronounced than for DEC and developer stakeholders, although still high with 83% agreeing that shortages are problematic. Amongst these respondents, shortages of skilled operational staff are more problematic – some 89% share this belief. Similarly, amongst end users, the availability of operational staff remains the area of biggest concern with 85% agreeing, albeit this represents a decline on the 94% we recorded six months ago.

Impact of skill shortages

Any successful industry relies on its ability to deliver its goods or services to its clients in a timely and cost-effective manner. The challenge for the European data centre industry is to ensure that the core building block of its offering can be achieved in this manner. Evidence suggests that these skills shortages have already had real consequences and directly impacted our respondents and indications are that the negative effects have been experienced in multiple ways.

We have previously seen that increased operating and labour costs and greater workload on existing staff equally topped the chart as the most cited impact by our respondents; 86% and 85% respectively six months ago. In our latest survey, that remains the case with the former referenced by 81% and the latter 80%, both totals reflecting a small decline on the summer.

We have noted a small increase in what could be acknowledged as the most extreme consequence of skills shortages; lost orders. At 11% this is a rise on the 9% indicated six months ago. In addition, the dearth in skilled professional has also contributed to the growing popularity of outsourcing options, with approximately 44% of respondents acknowledging it as a factor.

The number of respondents who found it problematic to satisfy existing work this year has also risen in the last six months, with 49% stating that they had experienced difficulties in meeting deadlines or client objectives. As we have seen, this is considerably below the heights of 70% who cited it as factor in our summer 2020 research, when the effects of the COVID pandemic and subsequent lockdowns were at their most influential.

Fig 21

In the past year we have experienced the following as a direct result of skill shortages

In addition, some 44% stated that shortages had led to delays in developing new products/innovations, up on the one-third who recorded this six months ago. In contrast, the proportion that noted they had ceased offering certain products or services has fallen to 12% from 22%.

Power

Consumption on the rise

The growth in demand for data centre services that we have witnessed in the wake of the ongoing digital transformation has posed a major challenge in terms of the resourcing and use of power. The industry continues to try to ensure an adequate supply of power is available to meet the increasingly power-hungry IT needs whilst satisfying social and environment needs to ensure it promotes renewable and sustainable power generation.

The results of our latest survey underpin that demand for power will continue moving forward, with some 83% of respondents reporting that they expect their power consumption levels to rise over the next three years, a slight increase on the 81% recorded six months ago. As was the case previously, almost all our developer respondents expect to see an increase in power usage; indeed, three quarters of these expect to see this rise to be considerable.

Amongst our services providers, the proportion expecting to see some increase stands at 90%, a slight drop on the 96% recorded in the summer, whilst amongst our corporate respondents this proportion drops to around 75%. With demand for data centre services forecast to continue to grow at substantial rates into the future, the challenge for the industry in dealing with the issue of both sourcing and consumption of power will remain.

Fig 22

Over the next three years, we expect our power per sq meter consumption to:

Once again amongst our service providers this proportion is even higher at some 96%, approximately the same as reported just six months ago, whilst 68% of end-users expect power consumption levels to rise over the period; an increase on the 62% recorded in our last survey.

Average Rack Power/cooling levels slowly rising

Over a quarter of respondents expect to see an average rack power/cooling level of 6kw-9kw over the coming year, unchanged on the levels who reported this previously. However, for the second survey in succession, we have recorded an increase in respondents anticipating average rack power/cooling level of 9kw-12kw; 36% up from the 28% monitored in the summer survey. A further 20% expect to see an average rack power/cooling level of 12kw-15kw over the next 12 months – a slight decrease on 23% who indicated this in the summer – and just 6% who suggested that they would see a level higher than 15kw per rack – a slight fall on the previous 7%.

Fig 23

What is your expectations for your average rack power /cooling level by the end of the year

Rising power cost to drive efficiencies

The rising cost of power that has been witnessed across the European landscape has been concerning, however this focus has likely benefitted the more energy efficient data centres and certainly highlighted a differentiator that has been marketed over the years. It is within this context that enterprises will continue to look for solutions to ease any negative impact rising energy costs may have on their occupation of data centre space.

Some 87% of our respondents indicate that they believe this rise in the cost of power will increase the demand for power efficient data centre space over the next three years, similar to levels recorded in the summer. Significantly, whilst agreement remained high amongst our service providers – 97% expressed their agreement with this outcome - just 45% of corporate stakeholders agreed, and this is a significant fall from the 58% recorded just six months ago.

Fig 24

We expect a rise in the cost of power in Europe to increase the demand for power efficient data centre space over the next three years

Move to renewables

As with all global industries, the current pressures favour an absolute move towards embracing renewable energy sources and reducing the reliance on the use of non-renewable energy sources where possible. Environmental and political factors are shaping the agenda, and the data centre industry has been playing its part in the conversation and signs indicate that it is increasingly proving its desire to continue creating the backbone to a more sustainable digital infrastructure.

The commitment to a move to source sustainable energy amongst the industry is clear; 88% of our response base expect to source at least 80% of their data centre power from renewable formats over the next decade, an increase on the 82% who expressed the same sentiment in our summer survey. In addition, the level of disagreement with this remains minimal with just 2% disagreeing, and this is a fall from 3% recorded in the summer.

Fig 25

We expect that the sourcing of power for our data centre in 2033 will be 90% or more sourced from renewable sources

For the fourth survey in a row our developer and investor respondents were near universal in their agreement on this issue whilst amongst our service providers the likeminded proportion sits at 92%, a slight increase on the 90% reported previously.

Given the current global difficulties, not least the continued occupation of Ukraine by Russia and the recent escalation of conflict in the Middle East, the benefits of a move towards renewable locally generated energy sources that are less susceptible to global disruption makes a lot of sense for all industries.

Once again, a significant majority of our respondents suggest that this is a preferred course of action for many in the industry. Some 71% of survey participants agreed that recent events would prompt them to expedite their transition towards renewable energy – up from the 68% recorded in our preceding survey. Only 6% disagreed whilst the balance - just under a quarter - adopted a neutral position.

Fig 26

In the light of recent geopolitical events, we will pursue an accelerated move towards renewable energy sources for our data centre(s).

For the second survey in a row, amongst end users this proportion stood at some 85%, whilst amongst service providers some 64% shared this belief, a fall on the 70% reported six months ago. For developers and investors, the level of agreement is slightly lower at around two-thirds, broadly in line with the proportion who expressed this preference in the summer.

Supply chain disruption continuing

There is little doubt that the impact of the global pandemic allied to more recent geopolitical issues has led to supply chain disruption for all global supply routes. The most recent events in Ukraine have led to significant inflationary pressures across economies driven both by notable rises in energy prices as well as raw materials. This supply chain volatility is still impacting the data centre industry – some 91% of our respondents stated that they had experienced such in the past year, a slight uplift on the 86% recorded in our preceding survey and this remains concerningly high.

We have already noted how the shortages of skilled professionals has been most keenly felt by those teams responsible for delivering new data centre facilities to the market. The same holds true for our supply chain volatility impacts. This is more apparent in our latest survey where there has been universal agreement amongst our developer/investor respondents and DEC stakeholders of the considerable impact they have faced over the past year.

Fig 27

We have experienced considerable supply chain volatility over the past year

Although there is comprehensive agreement of an impact, the level of assent is less strongly expressed. In our summer survey 91% of developer/investor respondents confirmed their agreement in the strongest terms, this proportion has reduced to some 76% this time around. Similarly, among our DEC stakeholders the impact recorded has fallen slightly with 86% expressing their strong agreement, down from 93% in the summer.

Despite this slight fall, these overall levels are worryingly high, highlighted by concerns amongst our service providers which show that 97% have stated that they had experienced such supply chain problems, up from 92% reported six months ago.

Supply chain disruption impacting future data centre locations

The physical location of a data centre is an important feature for our respondents. Earlier in our survey we indicated that, for our respondents, location is second only to availability of power in a list of contributory drivers in identifying a new data centre location. There is real concern amongst participants that ongoing supply chain problems are likely to impact on the decision-making process regarding the location of future facilities. Some 64% state that this factor will heavily influence their choices for future locations for new facilities, remaining unchanged on that reported six months ago.

However, there are a broad range of opinions amongst the different groups of respondents. For example, our DEC participants were the most fervent in level of agreement with some 93% expressing such, up from 85% six months ago, and of these 79% did so in the strongest possible terms. In addition, our service providers appear to be becoming more concerned on this issue. A year ago, some 54% of this group cited their agreement, six months later this portion had risen to some 65%, now it stands at some 73%.

In contrast, for the fourth survey in a row corporate respondents expressed the lowest level of agreement, with just 40% agreeing that supply chain factors will heavily influence their future locations for new facilities, and this group also recorded the highest levels of disagreement with the statement - 35%, an uplift on the 22% recorded in the summer.

Fig 28

Potential long term supply chain problems will impact significantly on our decision making regarding the future location(s) of our data centre(s).

Inflationary impact - will clients pay?

Whilst the worst excesses of inflationary pressures driven in the recent past by higher energy prices appear to be easing- albeit slowly across many European economies - there is little doubt that our survey respondents have felt the impact of these price increases. Given this inflationary environment we sought the views of respondents on how these inflationary pressures have been dealt with - absorbed or passed either wholly or partially through to their clients.

Over the past six months we have monitored a reduction in the number of clients who have reported that they have already chosen to pass on the higher costs to their clients within the last 12 months of trading. In our summer survey some 66% reported that they had done so, reducing to 55% most recently. Importantly, amongst our service providers (colocation operators, carriers, and integrators) this proportion stands at around 60%, a fall from the 78% recorded in the summer, whilst among developers, the proportion has fallen from 64% to 52%.

Fig 29

Over the next year, we expect inflation in the operational costs of our data centre will force us to pass some or all these increases to our clients

Twelve months ago, the proportion of survey participants expecting to have to pass on future price rises to clients stood at some 85% which we see as still significant but fallen to 79% during the summer and now sits at 77%. Whilst albeit a small decline this may be viewed as a step in the right direction reflecting an increasing optimism on inflationary prospects in to 2024. For the second successive survey this proportion is higher (85%) for our service providers, unchanged in the last six months, whilst we see a similarly unchanged 90% of developers intending to pass on increased costs to clients.

Legacy data centres

There is little doubt that we are in a period of unprecedented change in terms of technological advances and processes. Digital transformation, mobile computing, generative artificial intelligence (AI) and Big Data are all helping to drive demand for data centre services and the digital infrastructure to support the sheer size and computing depth of those services.

One challenge that emerges with this rapid rate of growth is the ability of existing infrastructure to not only cope with the types of demand, but positively encourage and help it thrive. The need to deal with the greater workloads created and the more power density required places particular challenges for older legacy centres which were developed in a time when power draws were much less, and cooling infrastructure designed accordingly. Allied to this is the demand that our IT infrastructure is constantly measured and replaced to ensure compliance with the sustainable and increasing regulatory requirements focused on reducing consumption of power and water, as well as limiting carbon emissions. Sustainable business practice is no longer just a choice for well-meaning participants, it’s a must for all.

Age profile

Although it cannot be considered a comprehensive definition of what constitutes a legacy data centre, the age of such facilities can be used as a simple gauge to help provide a signal of the potential relative size of the problem facing the industry. To that end we have investigated the approximate proportions of stock by age range, using the approximate start date of when M&E infrastructure was established in the data centre.

Fig 30

Within your own physical data centre environment what is the approximate proportions of stock by age range, using the approximate start date of when M&E infrastructure has been established in the facility

At least 17% of our respondents have their entire data centre portfolio made up of facilities which are less than five years old, whilst around a third have at least half of their technical floorspace in this age bracket and 50% have at least some proportion of their data centre facilities less than 5 years old.

In contrast, one-third have at least some proportion of their facilities which are between six and ten years old and around 17% operate stock which is ten years old or more. In our initial research there appears to be no noticeable difference between the various groups of data centre professionals and occupiers.

What are the main problems?

There are several challenges that our respondents reported when dealing with legacy data centre space, and it is noted that most respondents cited multiple challenges affecting them, giving insight into the complexity of dealing with legacy stock. The most cited factor by some 56% of participants was cost; specifically, that the operational costs per sqm was too high to be competitive. Unsurprising perhaps given that the impact on the bottom line is generally the best measure for whether a solution is working for an enterprise.

The lack of sustainable and renewable power closely followed in second place, illustrating the difficulty in meeting CSR and ESG targets when there is a lack of available renewable power to meet modern IT environment demands. We have earlier seen the importance of power identified by our respondent base, and it is of no surprise to see it ranked highly given the social environmental platform that now underpins all business practices across the world not just in the high power-usage categories.

Fig 31

Which of the following problems have you experienced arising amongst Legacy stock (10+ years old)

The two lowest ranked factors - PUE greater than 2.0 and Unacceptable PUE to meet modern demand are both cited by around two-fifths of respondents. It should be noted that amongst our colocation operators, carriers and IT integrators, the proportion who cited a challenge with their PUE greater than 2.0 rises to 56%.

What would you consider as solution?

Aging infrastructure inherent in legacy data centres undermines its overall operational efficiency leading to ingrained limitations and high costs associated with operations and impedes an organisation’s capacity to meet the expanding IT demands of the occupier. So how does the industry address these issues in order for a data centre asset to operate competitively?

Again, almost all respondents cited multiple potential routes that they would choose to address legacy issues. The most cited solution by 47% or respondents was to retrofit key M&E areas to address the ESG & CSR issues. This was closely followed by the total decommissioning of a data centre asset after moving IT environments to new facility as well as the choice to upgrade M&E environment to address PUE issues to give a minimum 5-year extension - both of which were referenced by around 44% of survey participants.

Fig 32

Which of the following options would your enterprise consider when addressing Legacy stock (10+ years old)

In addition, and perhaps the most surprising, was that two-fifths of respondents admitted that they would manage a maintenance regime (notably in a reactionary manner) to extend the life of the data centre whilst a similar proportion would choose to upgrade key areas such as the mains power to the facility to improve power density. Just over two thirds agreed that they would upgrade the M&E environment to address PUE issues to give up to 10-year extension if that was an option. Amongst our end-users there is some divergence from the average. The choice to retrofit key M&E areas to address ESG & CSR issues and the total decommissioning of the data centre after moving IT environments to new facility were highly favoured, cited top by 57% of respondents.

Each option has its own challenges, all of which are influenced by both cost implications and the sustainability agenda. It should be noted that throughout this section respondents were offered the choice of picking more than one solution or option and there was almost universal opt-in amongst respondents to do this reflecting different approaches for different legacy facilities, unsurprisingly each treated on its own merits.

Arguably the most extreme option to take is the full decommissioning of a legacy data centre. This can be a complicated and potentially expensive option as the process covers a multitude of actions including removal of IT hardware through to stripping out the building management system and mechanical and electrical installations and the recycling or disposal of these. The recycling of e-waste to try to recover hardware parts for manufacturing IT equipment is important and can contribute to offsetting the impact of using new materials to produce new data centre equipment.

The choice to move to an existing facility or a new facility will depend on other business and economic drivers. We have already noted the attraction that the outsourced route has for many especially with the potential substantial CAPEX costs savings involved. Decommissioning a company’s legacy data centre should see savings on energy consumption, staffing expenses, and maintenance costs whatever other option a company takes.

What have you done?

Over the past two years just under half of all respondents have addressed legacy issues within one or more of their facilities. Of these respondents, almost half had opted for the retrofitting of key M&E areas such as diesel generators and solar generation to address ESG & CSR issues, whilst the same proportion stated that they had upgraded the mains power to their facility to improve power density. Amongst our colocation operators, carriers/network operators and IT integrators/cloud over 60% have addressed legacy issues within one or more of their facilities whilst a slightly higher proportion (62%) of corporate users said they had done the same.

Upgrading the M&E environment to give up to a ten-year extension for the facility is favoured by just over two-fifths of survey participants. Interestingly, the least favoured approach was an upgrade of the M&E environment to give a minimum five-year extension suggesting that this these data centre respondents value a long-term solution for the data centre, potentially to satisfy their business commitments or ensure that user contracts can be supported by the facility.

Fig 33

If you have you addressed a data centre with legacy issues in the past 24 months what option did you follow to address the issues?

Around one-third of respondents who acted on their legacy data centre in the last two years chose to decommission those facilities. Amongst these, those who chose to move to a newly built facility (34%) slightly outnumbered those who moved to an existing data centre (31%). Amongst our service providers, the retrofitting of key M&E areas or upgrading mains power are the most cited choices, with around half stating these to be the case. In contrast, for our end users the most favoured approaches are the decommissioning of the legacy data centre and move to an existing facility/new facility.

What would you consider doing?

Looking forward some 56% of survey respondents agreed that they were likely to have to address a data centre with legacy issues at some point in the next three years. Amongst our service providers and end users this portion jumps to over two-thirds. When asked about how they would deal with legacy facilities in the future however, there is no clear consensus on which would be the most favoured route, although amongst the top options chosen were retrofitting key M&E areas to address ESG / CSR issues (39%), upgrading the M&E environment to give up to 10-year extension (38%) and the total decommissioning of the data centre after moving IT environment to an existing facility (37%).

The total decommissioning of a data centre after moving IT environments to new facility was cited around one-third or respondents, whilst the upgrading of mains power to the facility to improve power density and the minimum five-year extension of an upgrade M&E environment were chosen by 29% and 28% or respondents respectively.

Fig 34

If you likely to address a data centre with legacy issues in the next 36 months what option would you follow to address the issues?

Amongst our service providers there appears to be a leaning towards an active response to address the shortcomings of a legacy data centre with retrofitting key M&E areas, or upgrading M&E environment to give up to a ten-year extension, or upgrading the mains power to the facility to improve power density all supported by around 44% of respondents.

The ESR/CSR challenge

The practical problems that can be created by adhering to both ESG and CSR commitments within the legacy data centre is illustrated by the fact that some 60% of our respondents believe that the requirements for achieving these standards represents one of the biggest challenges they face in retrofitting a data centre.

Fig 35

The biggest challenge with retrofitting a data centre is in achieving required ESG / CSR standards in an economically viable manner.

Amongst service provider and end-user stakeholders, this level rises to 70%, with the highest level of agreement seen from our DEC participants at some 83%.

In recent years we have seen an increasingly level of societal, and legislative pressures that have led enterprises being asked to conduct their business in and more ethical manner. Moving forward this is unlikely to diminish. The analysis above indicates, our respondents are fully aware of the challenges meeting these requirements regarding their legacy facilities, but there is no doubt these factors will impact on their business across a wider sphere.

Monitoring & Maintenance only not enough

Perhaps the least expensive option is to undertake a reactionary monitoring and maintenance programme in the data centre, responding to faults and upgrades when demanded. Whilst this route will undoubtedly save both upfront cost, resource and disruption in the short term, this approach is not considered a sufficiently robust avenue to dealing with issues in legacy facilities by most of our respondent base, with only a third supporting it.

Of course, the monitoring of systems is an integral tool to safeguard the data centre environment and ensure insight into the performance and health of critical systems. It may be that our respondents view a reactionary version simply as a short-term option, but over the longer term a more proactive approach is likely.

Fig 36

A reactionary Monitoring & Maintenance program is an acceptable policy to address Legacy (10+ years) data centre space

Legacy operational costs impacting ability to meet IT requirements.

We have already noted the importance of the bottom line to our respondents. This is more keenly illustrated when our stakeholders were questioned about the impact of rising operational costs associated with older data centres on their IT strategy moving forward. Some 55% agreed that rising operational costs in respect of their legacy facilities are likely to prove problematic moving forward. Whilst 23% disagreed a further 22% adopted a neutral position.

Amongst our service providers this proportion rises to two-thirds whilst a quarter expressed their disagreement whilst amongst end users a slightly higher proportion some 69% share this concern.

By their very nature the costs associated with maintaining legacy facilities limit the ability of enterprises to raise expenditure for new systems especially in times of economic uncertainty when pressures on budgets tend to be enhanced. These pressures especially in a higher inflationary environment set real challenges to CIOs and IT managers to ensure that technology spend is deployed in the most efficient manner. Limiting costs associated with legacy data centres will have real appeal.

Fig 37

Rising operational costs associated with legacy data centres are likely to adversely impact our ability to meet other IT requirements in the coming three years.