es

es de

de it

itContents

Click to go to key areas of report

Thought Leadership Post

The Supply/Demand Dynamic

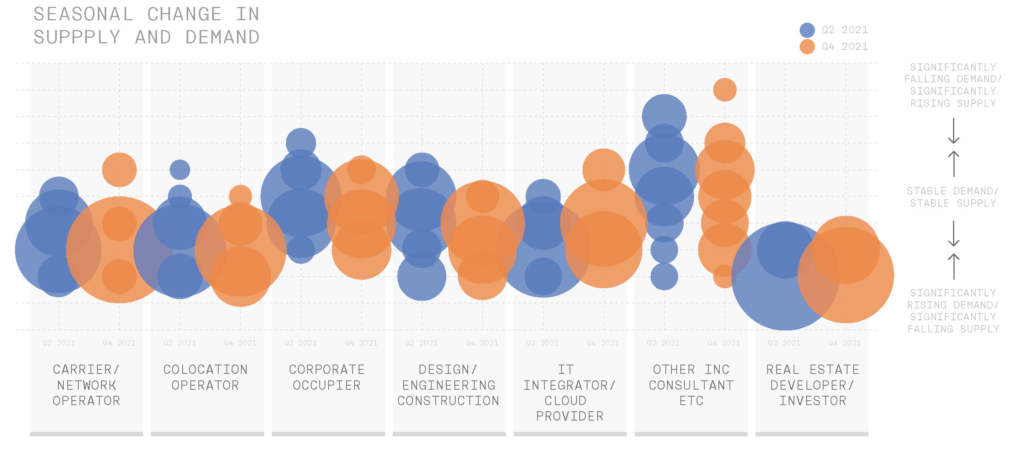

In our latest survey, the European data centre market is characterised by falling supply and rising demand levels; a view held by around four-fifths of our respondents, an increase on the 71% recorded in our Q2 survey.

The number of those seeing demand either maintained or increasing is almost universal (98%), with few respondents forecasting a fall in demand over the next 12 months. These results are the highest recorded since our survey began over 12 years ago.

Developer and investor respondents remain the most confident in terms of market sentiment; the vast majority suggesting that demand will be rising over the next 12 months.

Most suppliers of data centre services are positive around the balance between supply and demand in the market, with colocation providers being the most optimistic, some 97% seeing rising demand.

Carriers/network operators and IT integrators are almost as confident, with around 90% believing the coming year will be characterised by rising demand and falling supply.

Corporate respondents continue to be the most cautious of our respondents, with around 45% indicating that they expect demand to remain stable over the coming year. Encouragingly for the second survey in a row no corporate reported that there may be a fall in demand.

Ownership & Management

Our colocation operators and IT integrators/web hosting respondents continue to prefer to manage most of their own facilities, with over three-quarters recording that 80% or more of their data centre portfolio was internally managed. This proportion has remained constant over the course of our survey reflecting an emphasis for control of their own space, allowing them to respond more quickly to client demand, as well as providing their clients with an added-value proposition.

In contrast, end-user respondents have become increasingly drawn away from reliance on self-managed IT infrastructure towards third-party solutions, a dynamic driven by several factors: Building data centres is expensive, requiring a large CAPEX; Focussed data centre providers are more likely to have access to latest technology advances and services that are not available to a non-specialist end user, and the desire for flexibility to respond to rapidly changing environments can be more easily met by specialists whose business focus is solution delivery.

Utilisation

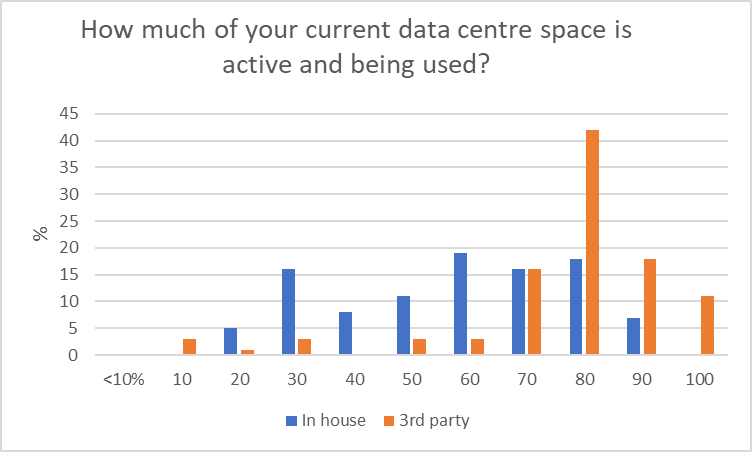

The desire for users to maximise the utilisation of their data centres whilst maintaining flexibility for growth has been a constant over the last 12 years of our survey work. For both service providers and corporate users of an externally managed solution this is especially true, driven by the need to balance costs associated with taking occupied and expansion space. The average utilisation rates of third- party managed space continue to exceed those for internally managed solutions. In our last survey in Q2, 71% of respondents reported that they utilised over 80% of their outsourced technical footprint against 27% who utilised the same percentage of in-house managed facilities. Our latest survey has seen a continuation of this, with the proportion having utilisation rates of 80% or more in their externally managed solutions rising to 73%, whilst in-house utilisation rates stood at 28%.

This requirement to maximise efficiencies in third-party data centres for the end user is even more prevalent. The proportion of 80% or more utilisation rises to 88% for third-party space contrasted to 55% reported by our in-house managed facilities.

In contrast, average utilisation rates for service providers tend to be marginally lower with around two-fifths of their own facilities reaching utilising rates of 80% or more. This may well reflect the need to balance the commissioning of space to meet expected demand and having near-finished space to allow quick deployment when needed. As with other users, service providers are driven by a need to maximise value for money regarding their third-party managed space, maintaining relatively high utilisation rates with 82% utilising at least 80% in these facilities.

Expansion

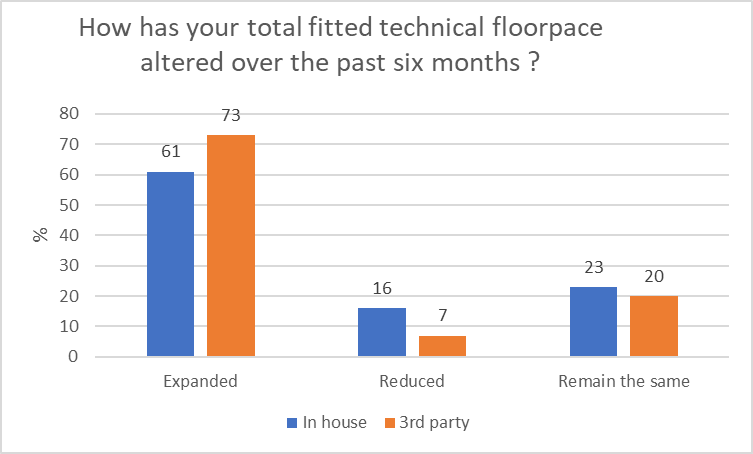

In the six months to the end of October 2021, just over 60% of respondents indicated that they had increased their in-house managed data centre capacity, a marginal decline from the 63% recorded in our Q2 survey. In addition, the proportion of respondents reporting a reduction in their in-house technical floor space has remained at 16% - a level which has been largely unchanged for the fourth successive survey. The proportion that saw “no change” - which has remained at around 20% for the past three years – saw a marginally uptick to 23%.

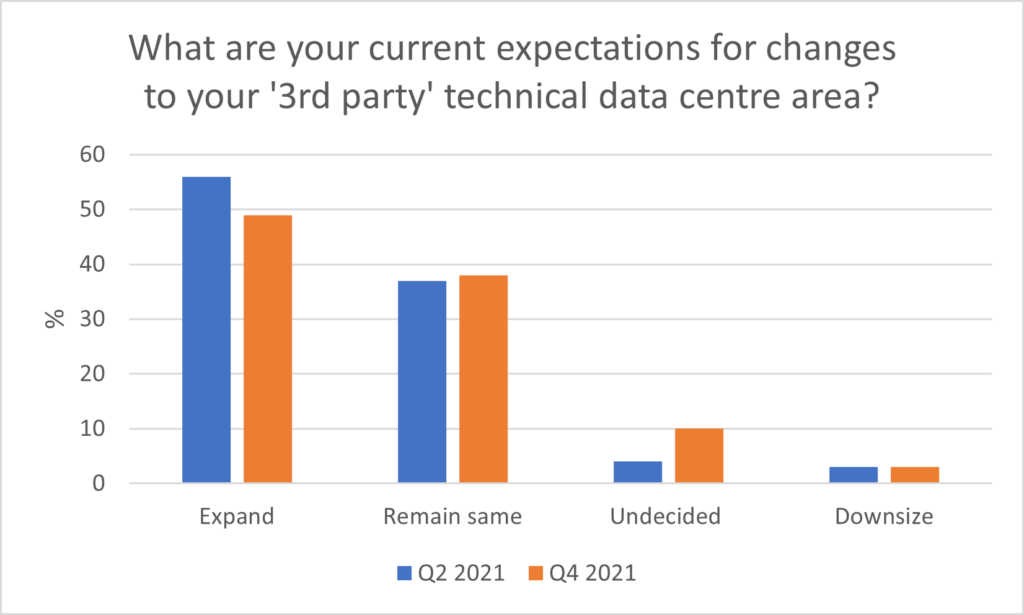

An examination of third-party expansion patterns over the past six months points to continued expectation of high levels of demand for data centre services, with 73% of our respondents indicating an increase in their externally managed solutions over that period. This represents a rise on the 67% recorded in Q2 2021 and compares favourably to the long-term average of 44%.

Corporate respondents continue to appear to be outsourcing a larger proportion of their data centre management to third parties, with four-fifths indicating that they have expanded their externally managed data centre portfolio in the past six months, a similar proportion to that recorded in Q2, and a notable increase on the two-fifths monitored a decade ago.

How was expansion achieved?

In terms of expansion within self-managed facilities over the past six months, the most popular chosen route was through self-build. 58% of respondents reported this approach, a marginal decline on the 63% in our last survey. This proportional decrease appears to have been driven by a rise in the purchasing or leasing through a development partner option, as those choosing this route rose from 20% to 26% in our latest survey.

Again, as was the case in the previous edition, around 17% of respondents reported that they have reduced their facilities through the decommissioning of a legacy facility, and of those that followed this route, the majority – some 63% - were corporate end users.

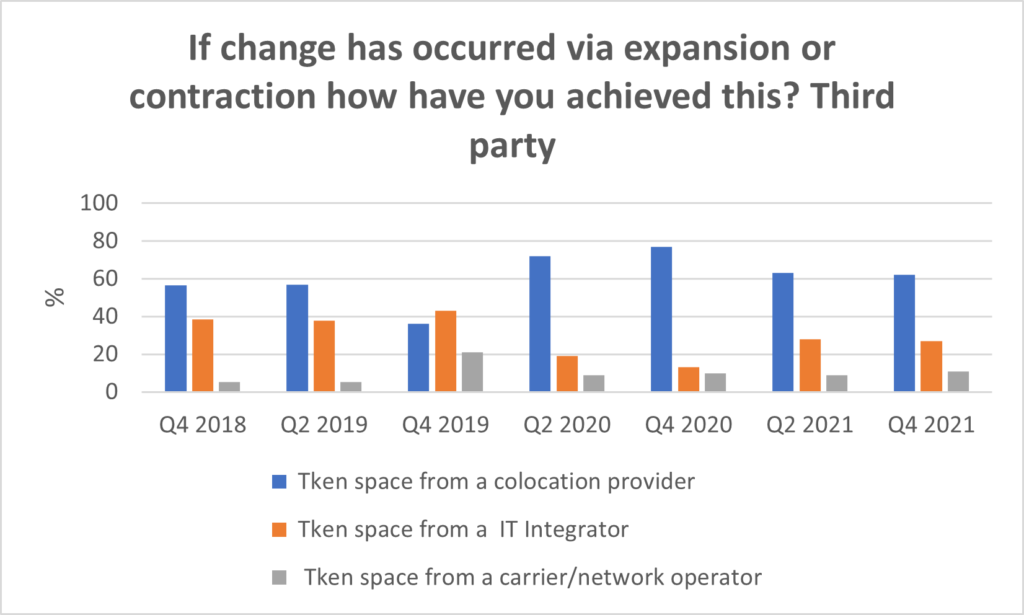

For those who have expanded in externally manged facilities, the use of a colocation operator remains the preferred route for many, with almost two-thirds choosing to do so; little change on that recorded in our preceding edition.

Our corporate users have been responsible for this use of colocation: some 77% of those who used this route came from our end-user respondents. Use of data centre services provided by Integrators was the second most favoured route with use of a carriers owned and operated facilities, the least favoured.

It should also be noted that some 12% selected more than one route to market. In these cases, this may be due to reasons of product availability at the right pricing or in the right location, or a combination of other specific requirement drivers. The contracting of space with an outsourced facility is driven by a complex matrix of both physical requirements and corporate trust.

No slowdown in expansion plans

The latest results suggest that 56% of respondents see their self-managed technical floor space expanding over the coming year; a marginal increase from six months ago, with our service-provider respondents being the most confident on this at 79%. Interestingly, respondents reporting an expansion increases in the second half of 2022, a good sign that forecasts for the longer term remain buoyant.

Drivers of change

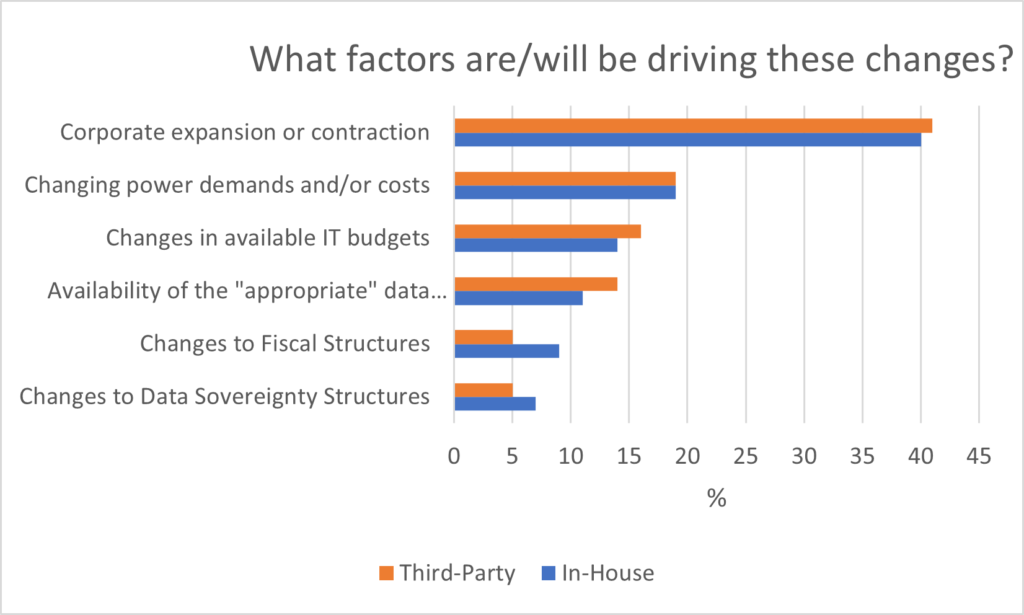

Corporate expansion or contraction has been established as the most highly ranked factor driving change in both internally controlled and third-party data centres since we undertook our first bi-annual survey back in 2009. Given that a company’s business growth or contraction and its supporting IT infrastructure are now inextricably linked across most business sectors, this is unsurprising.

In our Q4 2019 survey, we had seen a dilution of this as the premier driver of change, with the proportion of respondents falling from 45% to just over one third. Now, the last six surveys have revealed that this fall appears to be an outlier result and not a move away from this sentiment, with the latest results suggesting that two-fifths once again believe that corporate expansion or contraction is the most significant driving factor.

Demand for power and the costs associated with it have seen an uplift in the number of respondents citing it as an important driver of change to both internally and externally operated space – up from around 17% previously to 19%. Given recent news about the inflationary pressures on energy costs, it would be no surprise to see this rank even higher in our next survey.

For the third survey in succession there is evidence that budgetary issues are becoming more important; 15% of respondents cited them as a significant reason for change, which is an uplift from the 10% recorded in our last survey.

There appears to be mixed messages from respondents when it comes to the influence of data sovereignty and fiscal structure on data centre footprints. We had previously seen a rise in the number of respondents identifying this issue as highly important - from 15% to 18%. However, in our latest edition we see a reversion back to 13% indicating that respondents are once again rating other factors as more important. Have respondents adapted to the initial challenges around the changing political landscape in Europe – Brexit for example? It remains to be seen.

.

Developers, Investors & Funders

No easing in new stock plans

An important component to ensure a well-balanced European data centre market is not only the provision of new supply to satisfy future levels of demand, but to ensure that this is the right product in the right location. To understand more about the factors that drive those who fund and build that supply pipeline, we asked a series of questions targeted specifically at our developer and investor respondents.

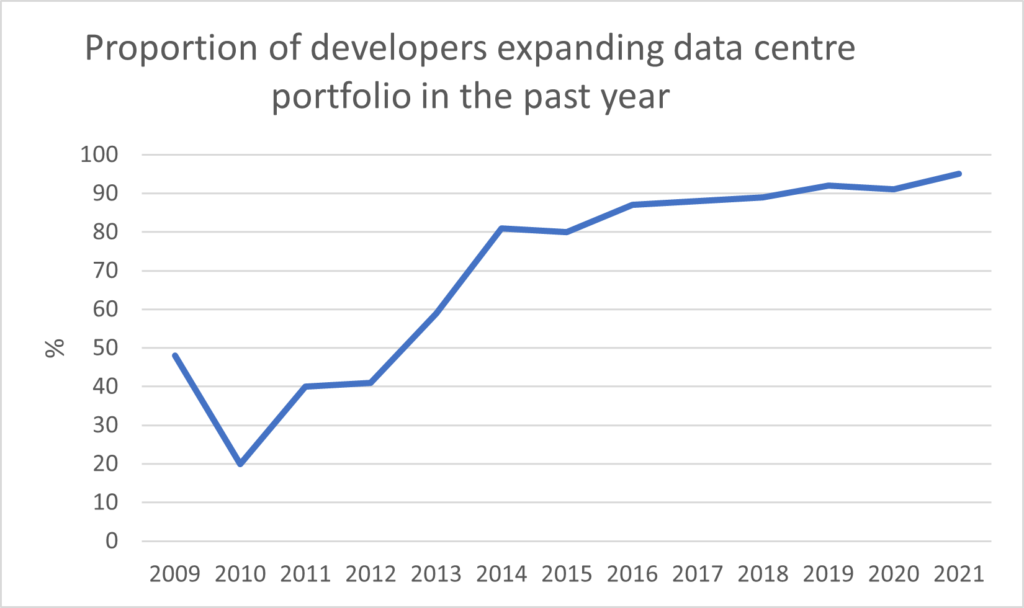

Our latest survey continues to provide evidence of the on-going confidence in the European market, with almost all developer and investor respondents reporting an expansion in their portfolio of technical real estate in the past six months. Indeed at 95%, it is now the highest proportion that we have recorded since the survey began.

.

As has been the trend over the last couple of years, portfolios have been expanded mostly through building activity, with over 80% of respondents reporting that they were involved in development activity over the period, with the remainder expanding through acquisition or merger activity. It is worth noting that these totals reflect the numbers of responses and do not reflect the size of those transactions.

The coming year

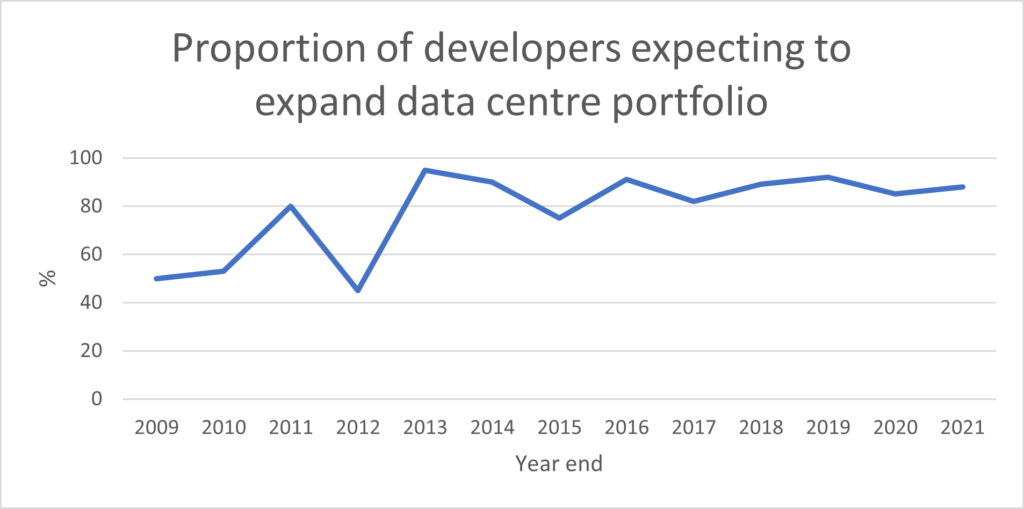

Around 88% of our developers and investors expect to increase the amount of European technical data centre area that they own or are prepared to fund in the next 12 months.

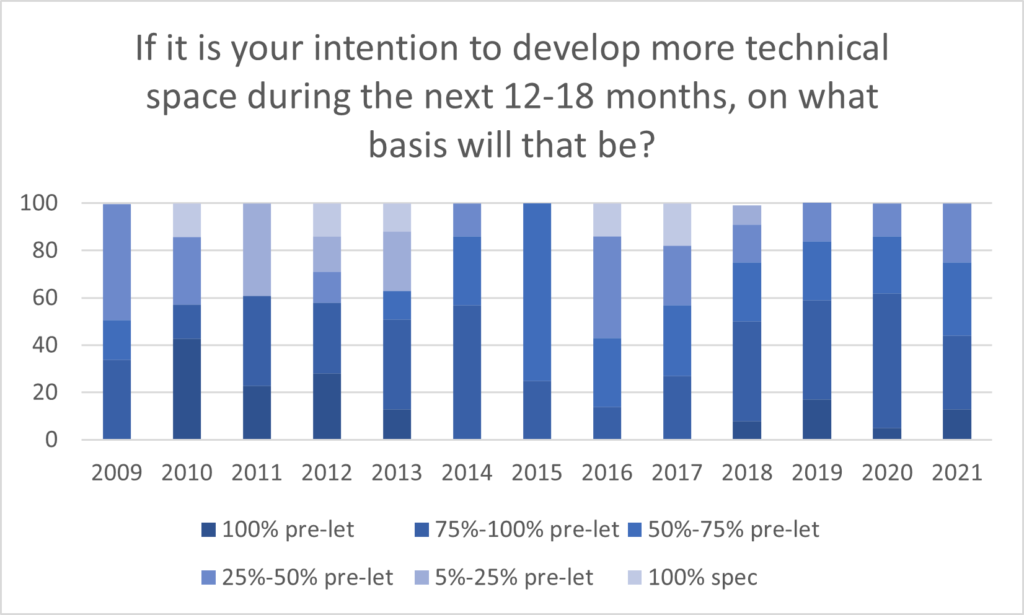

One measure that can be used to assess developer’s market sentiment is through the proportion of risk that they feel able to support by way of the amount of space they require to be pre-let before starting a development scheme. This helps provide an indication of the levels of sentiment that underpins their decision-making process.

Given this context, analysis of our latest data would suggest a slightly higher degree of caution is being exhibited by developers, as we have seen a rise in the proportion of respondents that have indicated they would only be prepared to move forward with their scheme if they have the security of a 100% pre-let; from 5% recorded earlier in the year to 13%, a marked jump.

In addition, no developer/investor respondent has reported that they would accept a pre-let of less than 25% of their scheme to start a development. Indeed, no developer has stated in our surveys that they would build on a 100% speculative since 2018.

Whilst the latest analysis suggests a continued seam of caution in the approach to delivering supply, it is by no means shared by all. For example, the proportion of respondents requiring 50% or more secured letting has actually fallen over the past six months from around 85% to three-quarters.

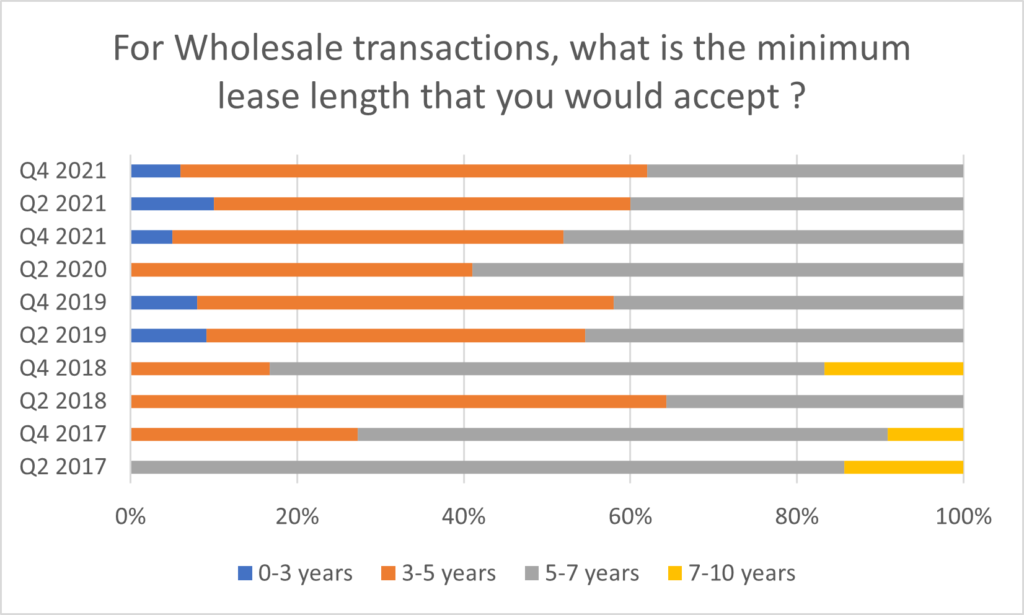

One other area of interest is the minimum lease length for a wholesale transaction that the developer would prefer to achieve. Our latest survey indicates that over half (56%) of respondents suggested a three-to-five-year period would be preferred, 18% would require over five years and just 6% would accept a period shorter than three years.

Data centre choice factors

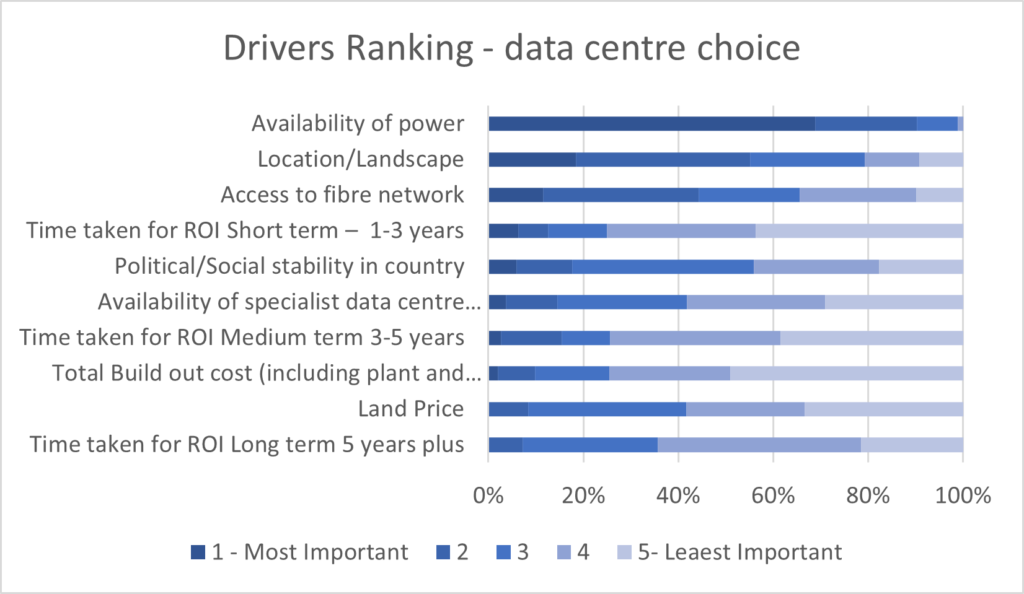

It has been well documented that the European power markets have entered a period of change, with prices touching new highs in a number of European countries; up to four times the average historical level. Electricity demand is expected to increase steadily in Europe, with some predicting a CAGR of about 2 percent until 2035, driven in part by the surge in electrification of areas such as transport and the production of green hydrogen through electrolysis.

Navigating these power markets will be a key challenge for data centres, driven by a demand from environmental savvy, but cost-conscious, corporates. Since we began this survey 12 years ago, power has consistently been ranked as the single most important factor in the ranking of the drivers of new data centres. The results of our latest analysis suggest that this remains the case, with over two-thirds of respondents choosing Availability of Power as their top influencing factor. Indeed, the proportion of those ranking it in either of the top two positions remains at a high of 90%.

Location is the second most highly rated factor, with over half of all respondents ranking it in the top two factor choices. We would expect this to continue to be ranked highly, particularly against the background of the UK’s withdrawal from Europe, the fallout of the COVID-19 pandemic, ongoing issues with supply chains and the effect that this may have on the location of company’s data centres relative to the markets that they serve.

Access to fibre has emerged as an increasingly important factor with around 10% citing it as their most important choice. Supply chain difficulties may well be impacting our respondent’s views on this issue. The largest concentration of the fibre optics supply chain can be found in Wuhan - epicentre of the COVID-19 outbreak. The Chinese city is home to companies such as Fiberhome, YOFC, and Accelink, amongst others, which together comprise a quarter of the global optical fibre production capacity.

We can also see that political or social stability has become increasingly more important in recent surveys, perhaps reflecting current perceptions and concerns regarding the wider geo-political and economic environments. Whilst the total build-out cost, availability of specialist data centre construction skills and land price are all important factors that are considered when looking at a new data centre build, they are consistently rated behind our top factors by our respondents. However, splitting out our developer respondents shows that these factors are ranked more highly by this group, just behind Availability of Power and Location, not surprising given that these would have significant day-to-day consequences for them.

Opinions

Design and build concerns

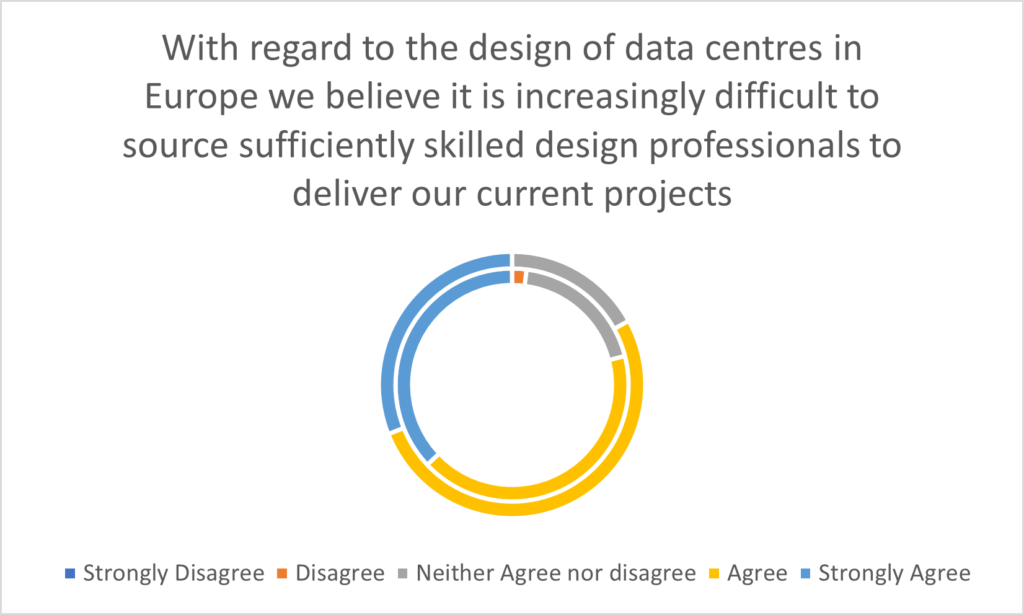

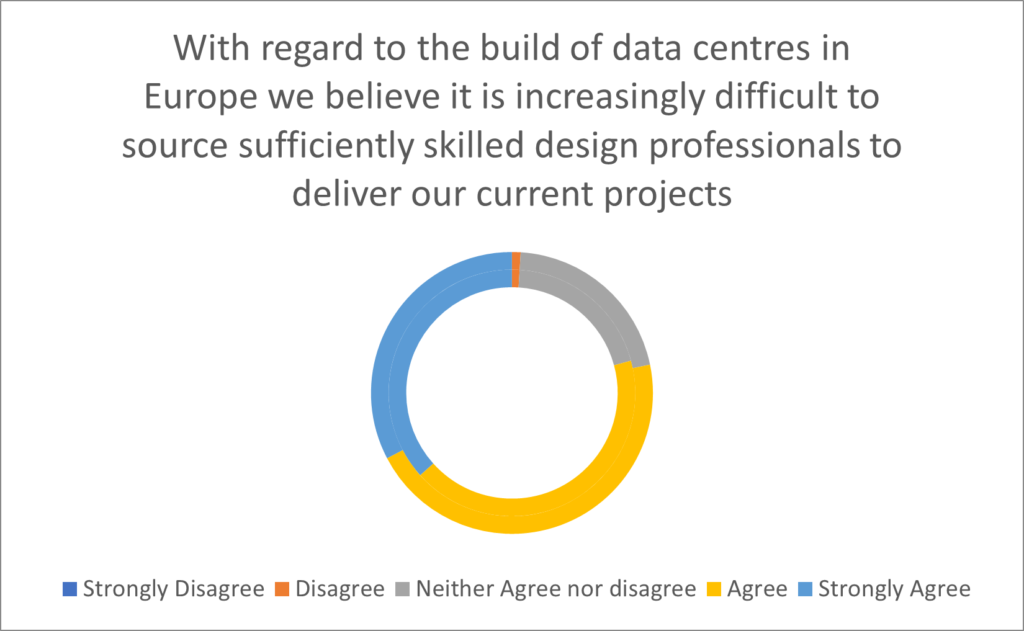

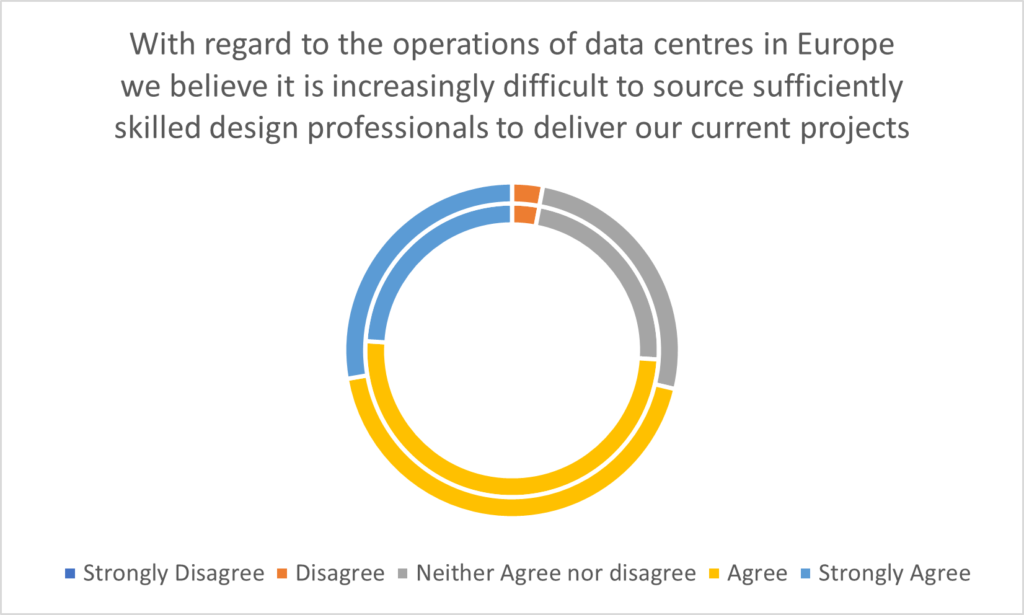

An ongoing area of concern within the industry as it has expanded is the lack of sufficiently qualified professionals available, particularly across the design, build and operations disciplines. Highlighted by the COVID-19 pandemic, where movement of labour was particularly restricted, access to the right professionals is vital to the ongoing health of supply and operations in the European data centre markets

The results for the latest survey suggest that these concerns continue for our respondents from all areas of the industry. Some 90% of all respondents suggested the market for these skillsets is currently characterised by that of falling availability and increasing demand. Those respondents who are at the face of this - real estate developers/investors or design, engineering, and construction (DEC) professionals - expressed this in the most emphatic of terms, with all respondents from this group sharing the view, a clear sign that they are feeling the imbalance.

For corporate respondents, the situation is less explicit with around half believing that demand for these skills is stable albeit also characterised by falling availability. This potentially reflects the fact that a significant proportion of these end users are increasingly “just consumers” of data centres and their services. Consequently, they are less directly impacted by issues that they do not have a daily interaction with.

The breakdown was as follows: 83% of respondents reported that there was a potential dearth of design staff across the European data centre industry, compared with 79% recorded in the Q2 survey. In addition, 79% shared a similar viewpoint in respect of build staff, in-line with that recorded in Q2.

On the operations side we noted a slight decline in the level of agreement - some 72% believe that it is increasingly difficult to source sufficiently skilled professionals in this realm compared with 74% last time around.

Again, these levels of concern increased amongst those who are directly involved in the building process, with all DEC and developer respondents stating they believed there was a shortage of both design and build personnel. In addition, some 95% of service providers shared this view regarding design and 81% on the build side.

Regarding shortages of sufficiently qualified staff on the operational side, the highest degree of corroboration comes from the corporate sector – over 90% expressed their agreement. In addition, three-quarters of service providers were also in agreement. This proportion dropped to 60% amongst our developer respondents.

Drilling further down, we have found that within design, nearly 40% of those surveyed cited experiencing a shortage of data centre architects within the last 12 months, whilst close to 50% stated that they had experienced shortages of suitably qualified construction managers, foremen and site engineers. Amongst developers, this proportion rises to nearly 80% for these roles.

Well over half of total responses stated that they have had direct experience of shortages of operations and network engineers/technicians over the last year, with a slightly lower proportion seeing a shortage of infrastructure specialists in the same period. Amongst our corporate respondents these proportions jumped to around three-quarters in almost all operational roles.

In addition, Mechanical & Electrical project managers were also highlighted as a major area of concern with around two-thirds of respondents acknowledging a shortage here. These levels of affirmation would indicate that concerns around skills shortages are still well founded and that it is an area of potential threat which needs to improve to ensure supply of new data centre stock is not impeded. Indeed, the survey provides evidence that these skill shortages have already had a real impact of the businesses of our respondents.

The two largest impacts of skill shortages cited by our respondents are increased workload for other staff and increasing operating and labour costs. In both instances around four-fifths cited each factor. Whilst in the case of the latter, the proportion has remained unchanged since last survey, a higher workload for other staff has fallen slightly over the period.

There is no doubt that greater workloads for existing staff have in turn led to problems in resourcing existing work, with around two-fifths of respondents stating that they had experienced difficulties in meeting deadlines or client objectives. The more extreme consequence of this has led to lost orders – around a fifth believe that they have directly lost orders as a consequence. In addition, a further quarter stated that shortages had led to delays to developing new products/innovations, but a smaller proportion (9%) indicated that they had ceased offering certain products or services because of this shortage.

Fit out labour

This issue of skills shortages is a long standing one, with evidence suggesting that the difficulties faced by data centre builders has been made worse by additional disruption in supply chains as well as labour shortages.

We have experienced difficulties sourcing labour regarding the fit out/operation of our data centre(s) in the following categories

In all instances there has been a considerable uplift in experienced disruption across all elements of data centre fit out with average degree of agreement rising from 2020 to 2021. Indeed, labour around both Power and M&E appear to be under severe pressure with around half of all respondents citing difficulties.

Notably, labour difficulties around security systems jumped from around 15% to 37%, and whilst not the highest proportion, a more-than-doubling of the number of respondents who felt this increase in constraint from 2020 to 2021 suggests a marked change in the market.

Power – The ongoing challenge

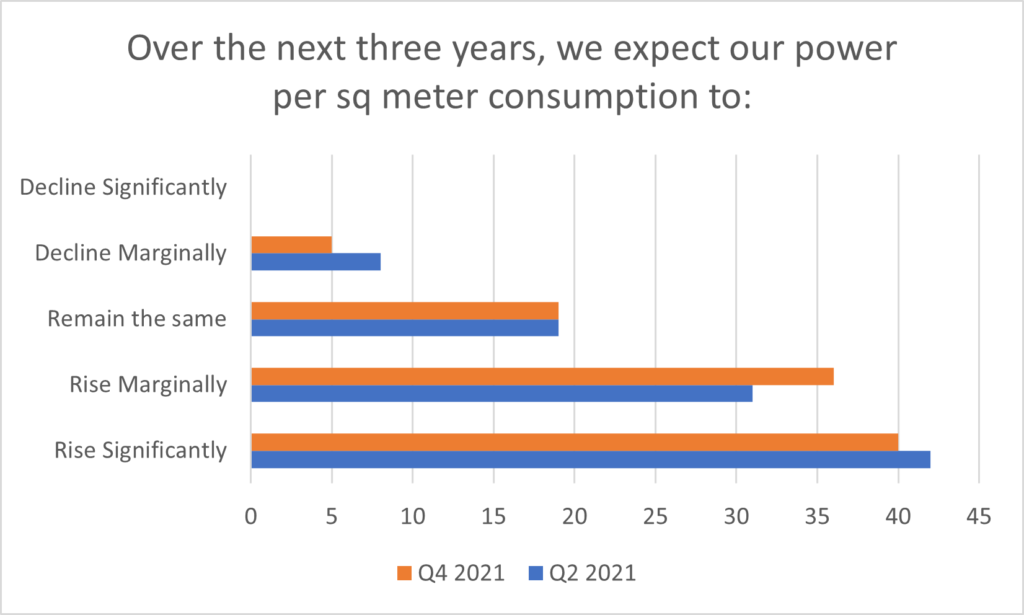

The surge in demand for data centre services that we have witnessed over the past decade in the wake of the ongoing digital transformation of society poses a major power challenge to the data centre industry. There is a real requirement for participant companies to evolve their power strategies to accommodate this demand. The challenge is to ensure a sufficiency of supply whilst meeting the needs posed by a political and social environment increasingly demanding that such power must be from a cost effective but sustainable source. The drive to Net-Zero.

The results of our latest survey underpin that demand for power will not diminish moving forward, even considering technological enhancements that drive efficiencies of equipment. Over three-quarters of respondents reported that they expect their power consumption levels to rise over the next three years, a proportion which has moved marginally up since the last survey.

Almost all our developer respondents expect to see an increase in power usage, whilst amongst our services providers, this proportion stands at 82%. Notably, amongst our end-user respondents this proportion drops to around 50%, suggesting that there may be a gap between what the providers believe they will need to deliver in the future, and what the consumers believe they will need.

Arguably, this apparent disconnect is the right way around, with supply parameters higher than those demanded, although the ever-increasing complexity of occupier profile means that demand standards will vary considerably, and suppliers need to remain flexible to ensure it can maximise its appeal.

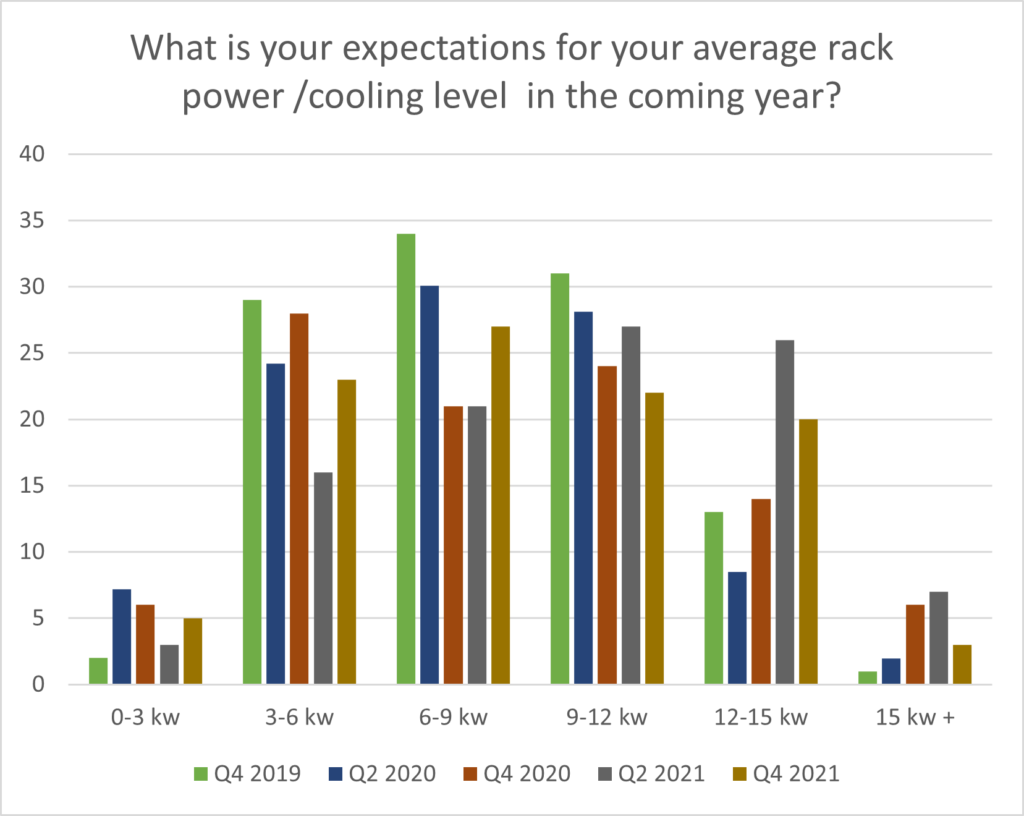

Average Rack Power/cooling levels to rise?

Over a quarter of respondents expect to see an average rack power/cooling level of 6kw-9kw over the coming 12 months, a rise on the 21% who reported the same six months ago. A further 20% expect to see an average rack power/cooling level of 12kw-15kw over this time, down from the 26% who reported the same range in our Q2 survey. Once again only a relatively small proportion of our respondents (3%) indicated that they would see a level higher than 15 kw per rack – notably less than half the 7% who reported the same in Q2.

Amongst our corporate respondents, around half are expecting to see an average rack power/cooling level of 3kw-6kw by the end of next year whilst a further 31% suggest their average levels will be in the 6kw-9kw range.

Power efficiency increasingly attractive driver

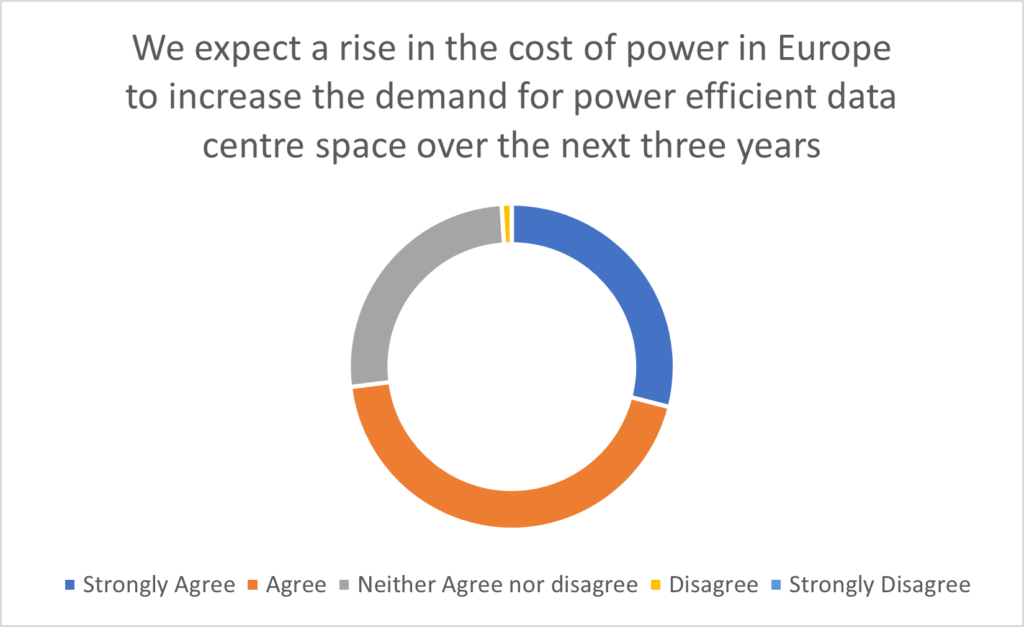

As power costs rise across Europe, the demand for data centres that are power efficient is also set to rise as almost three-quarters of our respondents believe that this will take place over the next three years. Perhaps the only surprise here is that this proportion is not higher given recent news around energy price inflation and the expected long-term impact on businesses.

Move to renewables

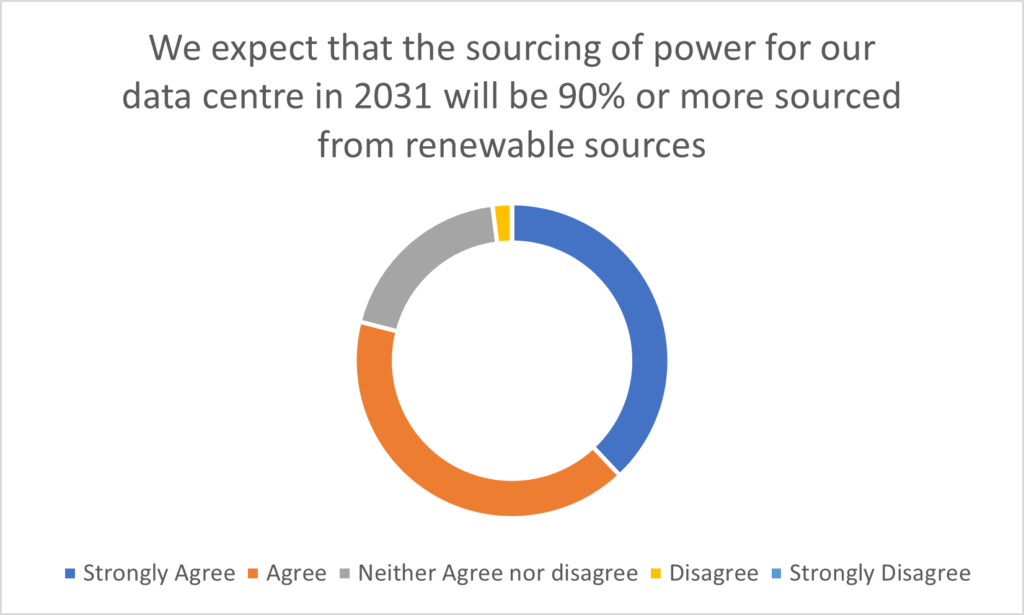

The commitment to a move to source sustainable energy is clear amongst our respondents. Over the course of the next decade some four-fifths of our respondents expect to see at least 90% of their data centre energy usage to be sourced from renewable forms, albeit this is a marginal decline from the 83% monitored in our previous survey. Just 2% disagreed, a fall from 5% in the Q2 report.

One feature of the energy market across Europe is the differing national and local sources of power which are delivered to the grid. This can reflect the natural resources available to a country as well as long-term power generation strategies adopted by governments over time.

In France for example, its political desire to operate as a nuclear power led to its first operational nuclear power plant opening in 1962. Now nuclear power is responsible for some 70% of total electricity production in that country. In the UK, nuclear is utilised to source around 21% of the country’s electricity whilst gas/coal variably provide just over half. In Spain where 61% is generated from non-renewable sources (gas/coal and nuclear) whilst 18% is from wind, 14% hydropower and 5% from solar.

The ongoing and likely future increase in power consumption indicate that the industry needs to continue to innovate to keep up with demand for cost-efficient power delivery within the context of a framework of Corporate Social Responsibility. Given this context, for the second successive survey we questioned our respondents on their current and future power sourcing strategies.

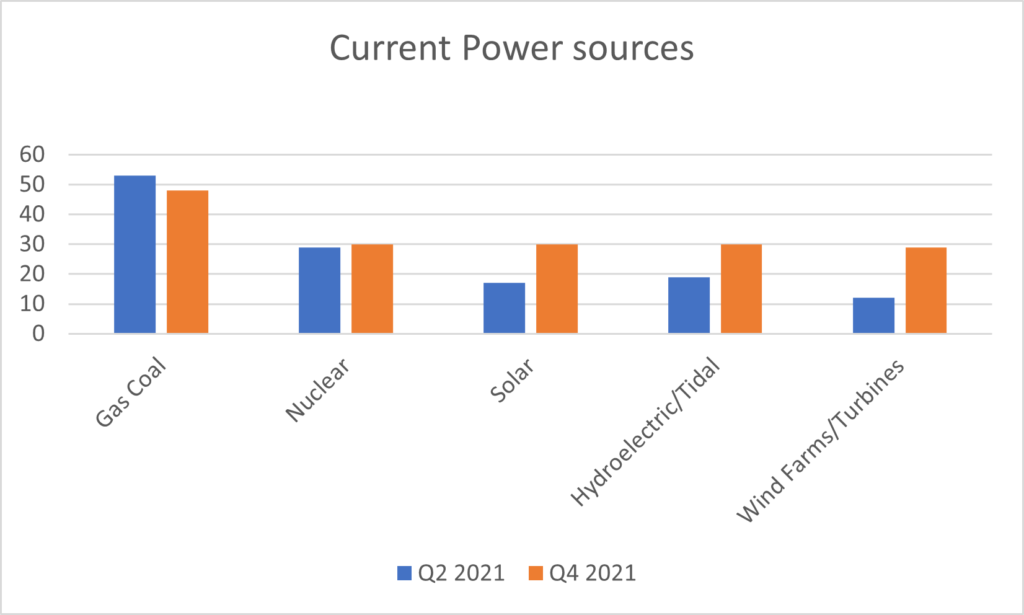

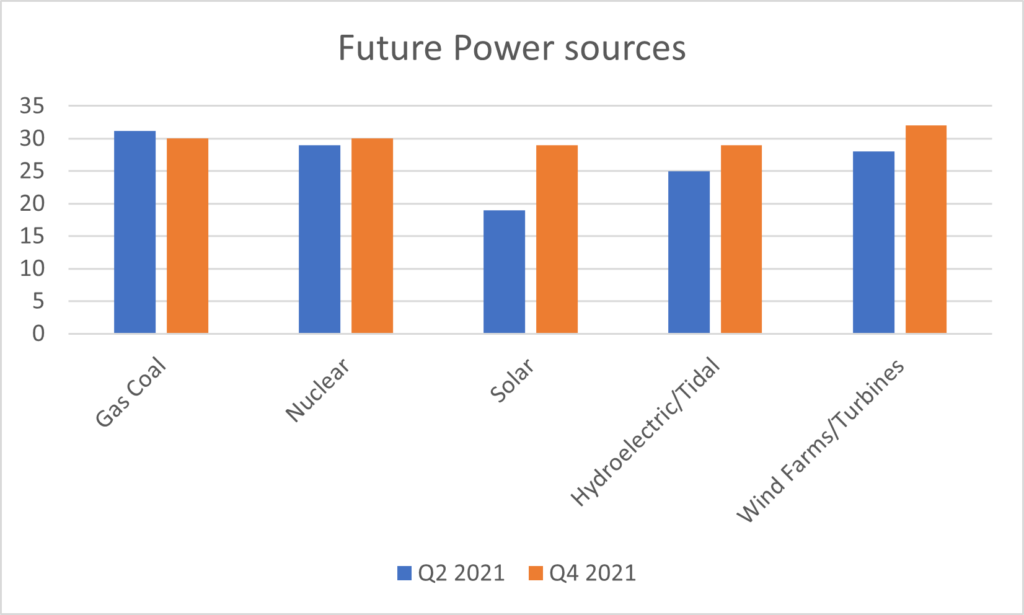

Given the disparate nature of sources of power across European territories and the wider geographical spread of some of our respondents with multiple facilities across their portfolio, it is perhaps not surprising that as with the Q2 survey, we have noted that only around 10% of our responders secure their energy from a single source. Encouragingly of those who source energy solely from finite resources such as gas and coal, totals less than 5% of our respondents, a marginal decline on the 7% we recorded in Q2

In contrast around 21% of our respondents’ data centre portfolio floorspace is sourced only from a mix of renewable sources including solar, hydroelectric/tidal, and wind farms/turbines; up from 18% recorded last survey. It should be noted that just under half of our respondents utilise some degree of gas or coal power in their facilities, down from 53% six months ago whilst nuclear power is used as a source of power by around 30% in at least part of their portfolio.

Looking to the future, survey participants were asked to assess their expected average share of sources of power across their data centre real estate in the next five years. The results of which suggested a firm commitment by a significant proportion of respondents to move towards renewable energy as a key cornerstone of their future power usage.

One important measure is noted in the expected future use of gas or coal power in our respondents’ facilities. Currently just under 50% of respondents state they utilise energy generated from fossil-based fuels, a proportion which declines to around 30% over the next five years. In addition, nuclear power is expected to remain as a source of power by 30% of respondents on at least part of their portfolio.

Whilst only around 7% - a proportion unchanged for the last survey - suggest that their facilities will be sourced from a single type of renewable power, almost all respondents expect to see a rise in the proportion of power from renewable sources which will service their data centre facilities.

Supply chain challenges

There is no doubt that a major challenge facing the global economy in the wake of COVID-19 pandemic is dealing with supply chain disruption. Many decades of global growth have resulted in fluid global trading platforms, supported by a highly developed transportation system and underpinning the freedom of movement of both labour and goods. This well-oiled supply chain has been hit with a storm of disruptions as a result of the global pandemic.

Congestion and blockages in the production system, labour constraints, manufacturing restrictions, transportation interruptions, and dwindling access to raw material stocks, have all had their effect. Of course, when sentiment surrounding supply chains turns down, it leads to more desperate demand planning, which feeds back into the ever-escalating disruption equation.

Arguably, the data centre industry’s strong performance in the face of the pandemic will have placed further pressure on its supply chains at a time when it is least needed. For a real-estate asset class that has innovation and speed-to-market at its core, increased lead-times and uncertainty in the implementation of data centre projects will be difficult to accept. Indeed, supply-chain pressures are felt by owners and users alike as the global chip shortage disrupts internal data centre ecosystems that rely on server, storage and networking components.

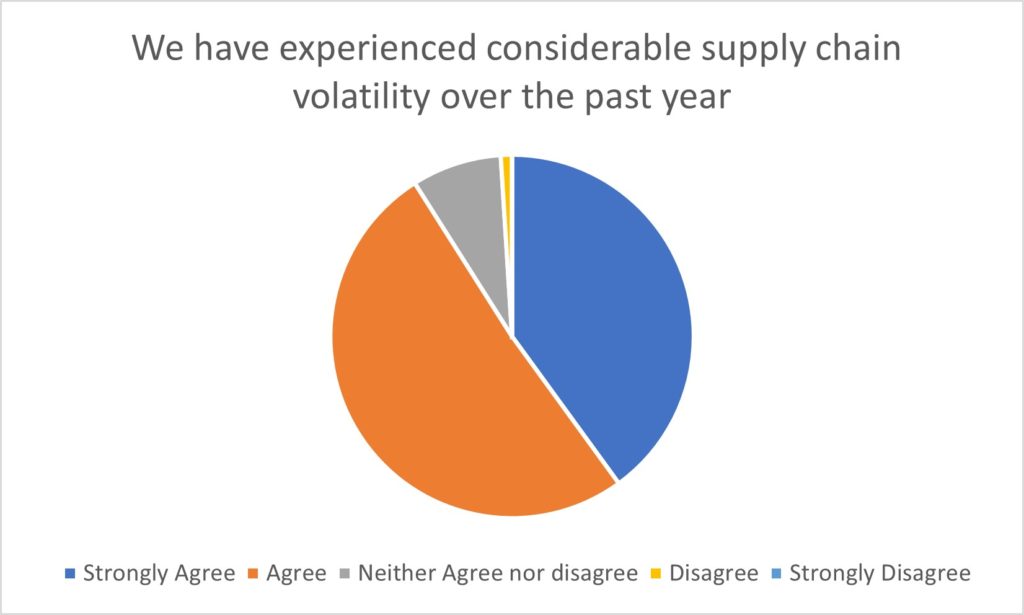

Our latest survey shows that there is considerable agreement amongst our respondent base that the sector has been heavily impacted by supply chain disruption. 91% of our respondents have experienced issues over the past 12 months. Disruptions were felt the hardest amongst our build professionals, with 69% of developer/investor respondents and 62% of design engineering and construction (DEC) respondents reporting strong agreement that 2021 had experienced supply chain volatility.

Construction

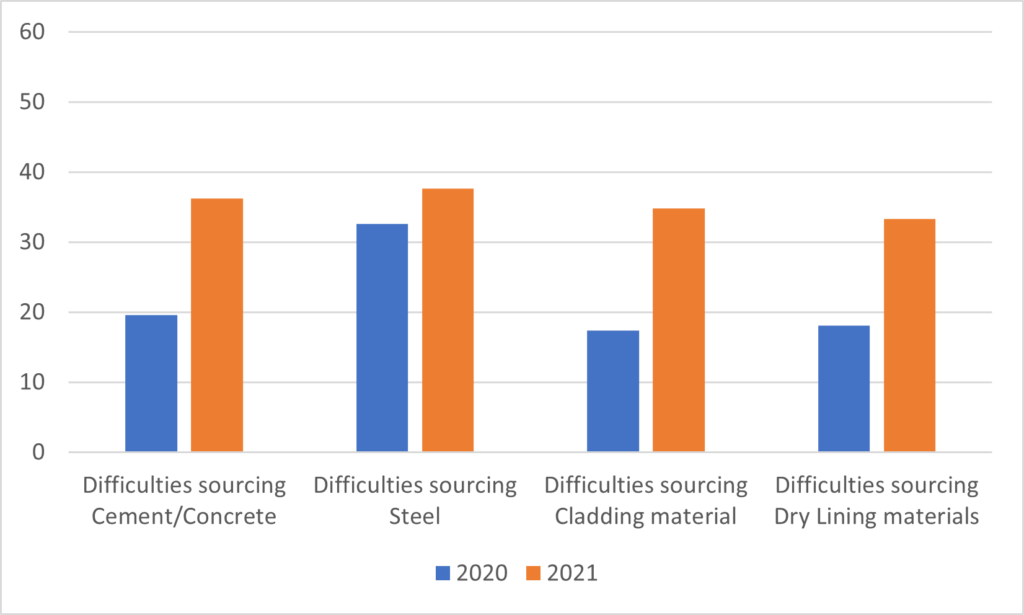

In the construction sector our respondents have reported that 2021 has provided a more severe challenge in sourcing construction raw materials contrasted to 2020. Concrete/cement, steel, cladding materials, and dry lining materials have all proven to be more difficult to acquire, as surplus stocks have been used up and price inflation bites.

For our developer respondents, around a third in 2020 experienced sourcing difficulties for concrete/cement, cladding materials, and dry lining materials – a proportion that rose to 62% in 2021. Notably, it appears that difficulties in obtaining steel were already hitting the sector in 2020, with 63% citing problems, rising to 68% this year.

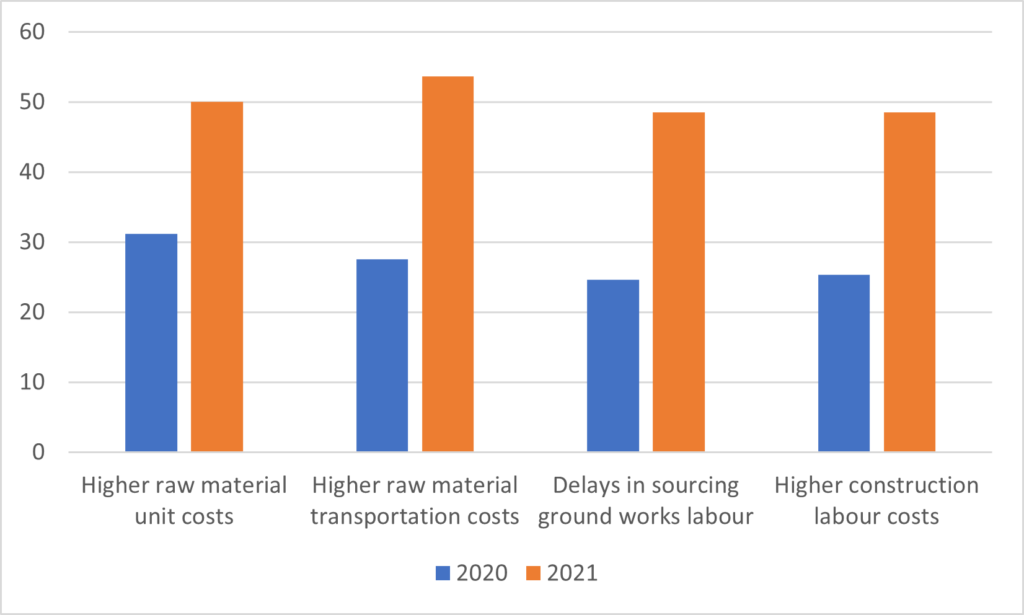

Regarding the base construction of our data centre(s) in Europe, we have experienced the following:

To some degree, the easing of lockdown measures helped to exacerbate the demand spike for many goods and services as manufacturers, consumers and builders reignited projects that had been on-hold in a route to re-establish a degree of normality.

Hand-in-hand with physical shortages has seen rise in associated costs – raw material unit and transportation costs as well as construction labour costs. In this case twice as many of our respondents cite having experienced these in 2021 compared to 2020 – up on the average from around a quarter to a half. Notably, DEC professionals indicated an average uplift from around 40% to 75%, whilst the proportion of developers in agreement rose from 40% to 68%.

Regarding the base construction of our data centre(s) in Europe, we have experienced the following:

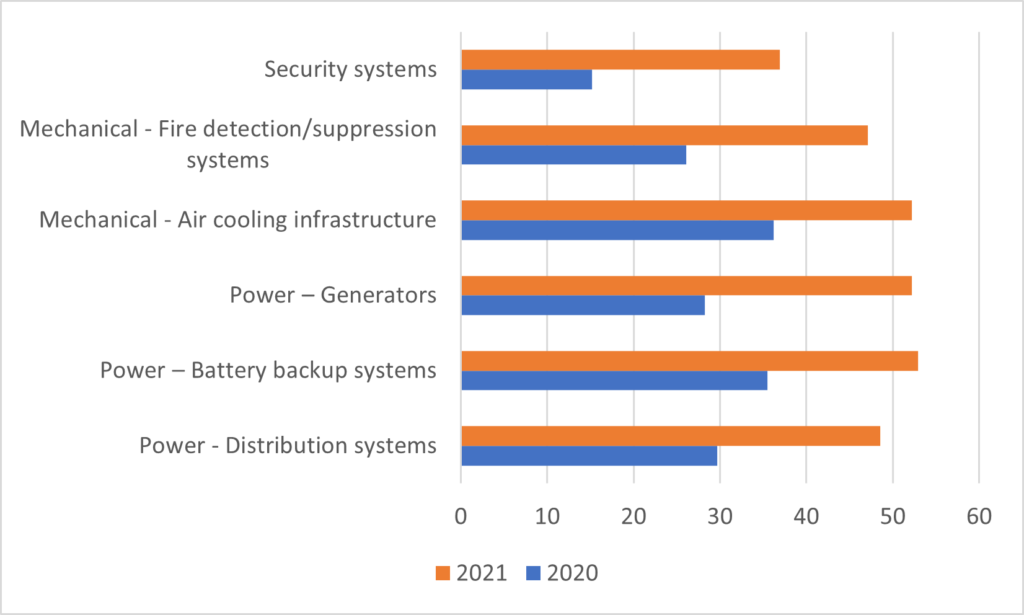

Fit Out

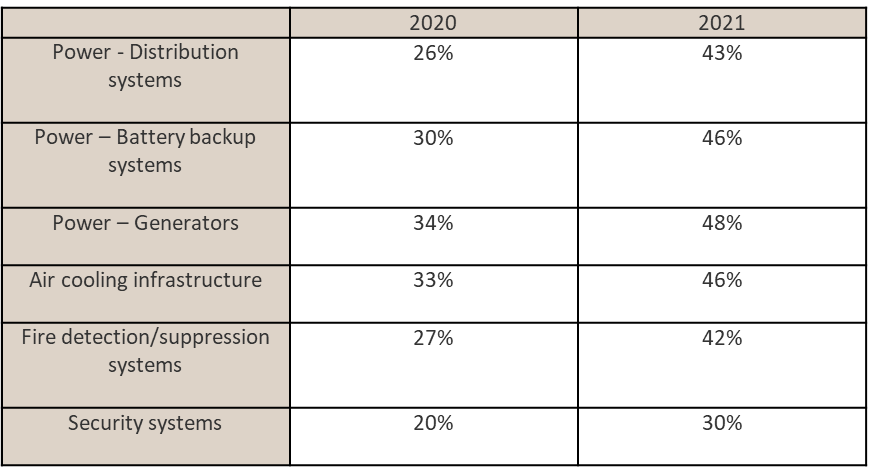

A significant proportion of our respondents reported difficulties in sourcing equipment components for the fit-out of their facilities during 2020 and 2021. Again, we see a marked uplift in problems this year compared to last, across all areas of the M&E functions, most notably around generator, battery and distribution infrastructure and air-cooling equipment. Indeed, amongst our developer and DEC respondents, power infrastructure issues in the supply chain were reported by 58% and 55% of respondents respectively.

For our service providers, disruption also appears to be felt markedly more this year compared to last, with the proportion of those citing difficulties above the collective averages. For example, 31% of colocation operators noted problems in sourcing air-cooling infrastructure, fire detection/suppression systems and security systems in 2020, rising to 56% reporting the same this year.

Regarding the fit-out/operation of our data centre(s), we have experienced difficulties sourcing data centre equipment components for

Conversely, our corporate end-users – some of whom will have their own self-managed space – report less disruption in the supply chain (either directly or in-directly from their third-party providers), although still witnessing a significant uplift from 2020 (9%) to 2021 (27%).

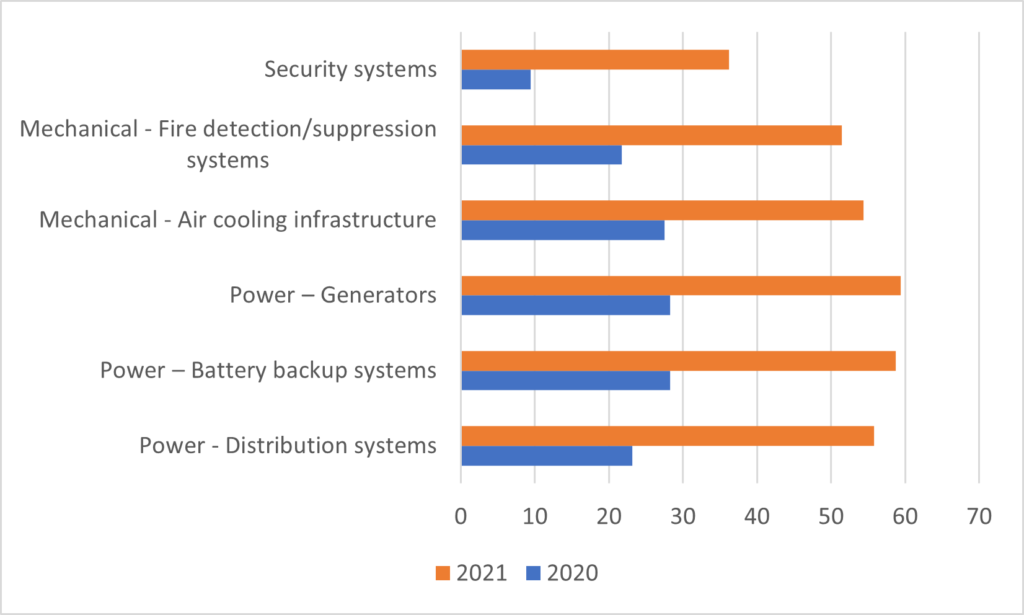

Regarding the fit-out/operation of our data centre(s), we have experienced significant cost inflation for the following...

As with shortages in construction materials, difficulties sourcing fit-out equipment components has led to price inflation across the board. In most cases, more than double the number of respondents has cited experiencing these rises in 2021 compared to 2020. Indeed, in the case of security systems components – the number has increased nearly four-fold from around 9% to 36% this year.

Perhaps more significantly, just over 70% of our colocation providers and 77% of developers reported cost inflation of power related infrastructure during 2021, an uplift from 31% and 35% respectively in 2020. This issue was not so significant amongst our telco and carrier respondents, but at 64% in 2021 still a significant proportion facing infrastructure cost rises.

There is little expectation that the current supply chain disruption will disappear in the short term as significant disruption drivers remain; power shortages in China affecting output, the rising price of raw material such as copper, fall-out from BREXIT to name a few, and all are exacerbated by an increase in demand across the world. However, there are some encouraging signs, with key metrics such as cargo shipping costs falling, congestion at ports easing and reported delivery times across the wider economy for manufacturers worldwide reducing.

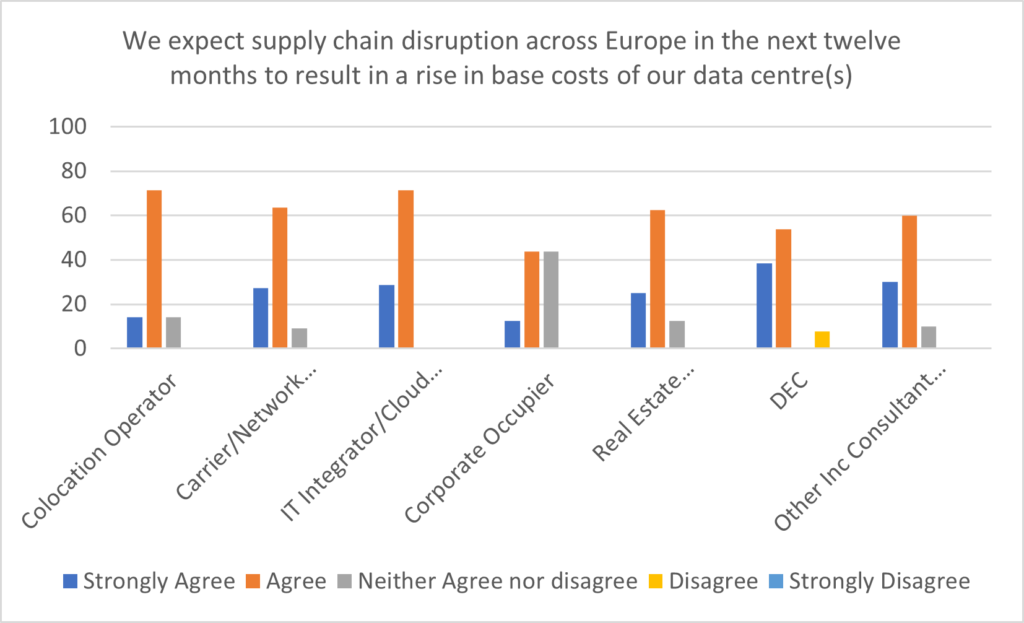

Despite this, our survey responses from September this year suggest pressure will continue to affect the industry, with some 84% of our respondents expecting to see continued inflation in data centre base costs over the coming year with just 1% not expecting an increase. Amongst our service providers – the colocation operators- carriers and IT integrators - the proportion of those agreeing rises to 89%.

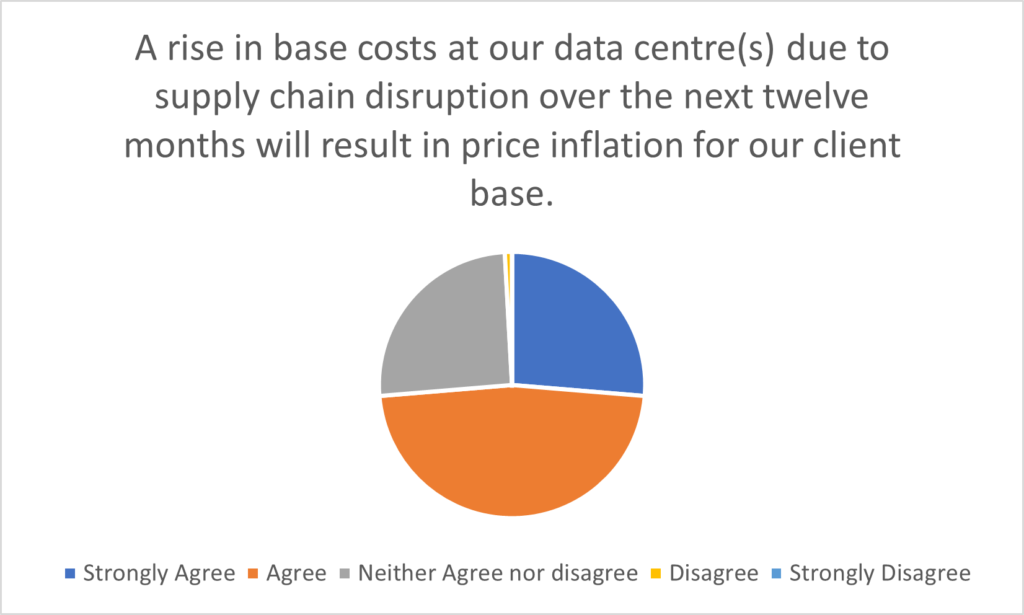

Of course, if the majority of providers see inflation in the base costs of the data centre, it will be expected that these rises will be fed through to the end user. Consequently, around 74% of all respondents expect that to be the case, whilst the remainder adopted a neutral position at present. Indeed, amongst our service providers – colocation operators/carriers and integrators some 81% expected to see such a rise with the balance, neutral. It may be that these particular latter respondents have adopted a wait and see attitude and have not yet decided whether they will pass on the rises to their client base.

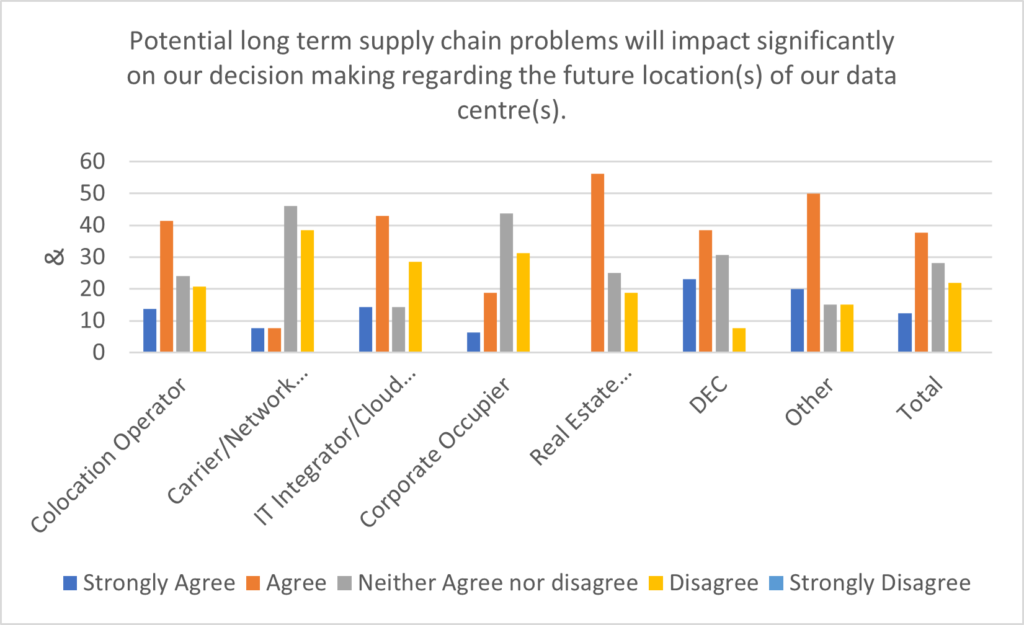

When asked about the likelihood that long term supply chain problems could impact in a significant way on future data centre location decisions, 50% stated that they believed that this would be the case. Whilst amongst our developer respondents this portion is slightly higher (56%) suggesting that supply-chain items may factor more highly in the development decision in the future, our corporate occupier and service provider respondents appear less influenced by these factors.

We will continue to monitor the supply chain influence moving forward, as for the first time in the European data centre industry history, a Black Swan event such as the pandemic has influenced not only the availability of product but will also have a lasting effect on pricing to end users and maybe even locational influences. Coupled with the on-going global disruption in energy production, distribution and move towards sustainability and carbon-neutrality, the industry is perhaps entering a noticeable period of change.